Investing.com’s stocks of the week

With the Federal Reserve reassuring investors of the course that would be taken in the coming months, the fate of the US monetary system appears to be fixed. Given that the Fed has purposefully played this out compared to past occasions from 2013 to 2016, we evaluated the impact of emerging market currencies and their path ahead in the following months.

Since the beginning of the year, the Brazilian real and South African rand have outperformed other emerging market currencies (EMs) such as the Turkish lira, Korean won, Mexican peso, Indonesian rupiah, and Argentine peso.

The US economy's imminent taper and interest rate increase signify a withdrawal of money from developing economies as investors seek income in developed countries. However, we believe the impact on emerging-market currencies would be modest because of the deliberate manner in which the rate rise has been prepared.

Rates were raised 18 times between 2003 and 2006 to battle inflation and an overheated economy in the United States, reaching 5.25 percent. However, the increase in interest rates in the United States increased net portfolio inflows in six of the eight emerging economies studied.

Compared to the 2013 taper tantrum, which drastically decreased emerging inflows except for China, which saw record inflows as investor confidence improved, we cannot rule out the possibility of history repeating. Still, we do favor more robust flows into developing markets.

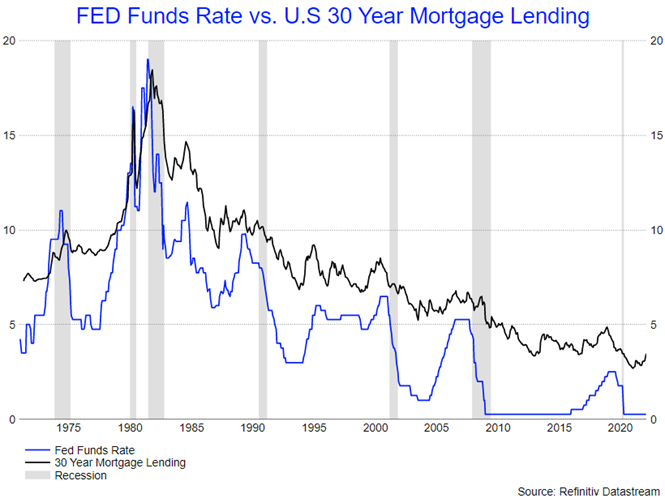

The question regarding how far the Fed can go? We predict that a 1.75 percent peak in present conditions will generally hinder growth prospects. Over the previous 45 years, the convergence of the Fed Funds Rate towards the 30-year mortgage rate has lagged a US recession, leading us to argue 1.75 percent as a significant policy threshold.

The South African Economy

On Feb. 10, President Cyril Ramaposa will present SONA 2022. As the economy faces a grave unemployment crisis, general discussions over Covid-19 will continue. Given that SARS collection was up 12.3 percent in September 2021 from the February 2021 projection, our growing worries for the first half of the year include Eskom price rises in April 2022, rising fuel costs, and a weaker rand as a result of global macroeconomic issues.

There is little question that commodity prices have fallen significantly, but supply-side limitations continue to create inflationary pressures. Investors will be keeping a close eye on potential development projects ahead of Minister Enoch Godongwana's budget announcement on Feb. 23.

We expect the rand to return to its comfort zone range of R15.55 to R15.72 as we approach the budget address, with knee-jerk price movement on the day. The SARB has guaranteed rate hikes gradually throughout this year. However, the direction of fiscal policy over the coming weeks will be heavily scrutinized.