HCP Inc. (NYSE:HCP) is slated to report second-quarter 2017 results on Aug 1, before the opening bell.

Last quarter, this Irvine, CA-based healthcare REIT delivered a positive surprise of 6.25% in terms of funds from operations (“FFO”) per share. Results reflected growth in three-month same-property portfolio cash net operating income (“NOI”).

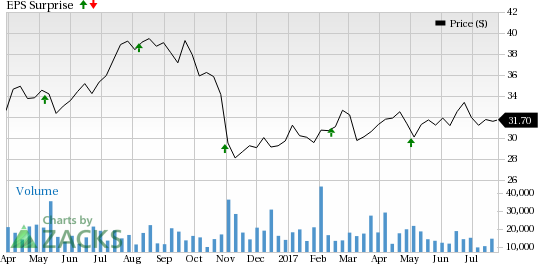

The company has a decent surprise history. In fact, over the trailing four quarters, the company exceeded estimates in each occasion, generating an average positive surprise of 4.22%. This is depicted in the graph below.

HCP’s shares have gained 6.7% year to date, outperforming the industry’s growth of 3.4%.

Let’s see how things are shaping up prior to this announcement.

Factors to Consider

HCP has a diversified, well-balanced portfolio in the healthcare sector. The company is likely to benefit in the to-be-reported quarter from rising healthcare spending and a growing aging population. Further, strategic investments, tie-ups and acquisitions are anticipated to drive decent cash flows. Also, the sale of 64 Brookdale Communities to affiliates of Blackstone (NYSE:BX) Real Estate Partners VIII L.P in the first half of 2017 helped it reduce the Brookdale concentration and the company remains on track with its deleveraging plan.

However, growth might be hindered by cut-throat competition in the company’s markets. In addition, there is increased supply in senior housing category that is expected to lead to softness in this market fundamental. In addition, it cannot bypass the dilutive impact on earnings in the near term from huge asset dispositions.

Overall, HCP’s performance during the quarter was inadequate to win analysts’ confidence. As a result, the Zacks Consensus Estimate remained unchanged at 47 cents over the last 60 days.

Earnings Whispers

Our proven model does not conclusively show that HCP will likely beat estimates this quarter. This is because a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or at least 3 (Hold) for this to happen. But that is not the case here, as you will see below.

Zacks ESP: The Earnings ESP for HCP is 0.00%. This is because the Most Accurate estimate of 47 cents matches the Zacks Consensus Estimate. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: HCP’s Zacks Rank #3 increases the predictive power of ESP. However, we also need to have a positive ESP to be confident of an earnings beat.

Stocks That Warrant a Look

Here are a few stocks in the REIT space that you may want to consider, as our model shows that these have the right combination of elements to report a positive surprise this time around:

CyrusOne Inc. (NASDAQ:CONE) , likely to release earnings on Aug 2, has an Earnings ESP of +2.70% and a Zacks Rank #2.

Piedmont Office Realty Trust, Inc. (NYSE:PDM) , expected to release earnings on Aug 2, has an Earnings ESP of +2.27% and a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

AvalonBay Communities, Inc. (NYSE:AVB) , likely to release second-quarter numbers on Aug 2, has an Earnings ESP of +0.94% and a Zacks Rank #3.

Note: All EPS numbers presented in this write up represent funds from operations (“FFO”) per share. FFO, a widely used metric to gauge the performance of REITs, is obtained after adding depreciation and amortization and other non-cash expenses to net income.

The Hottest Tech Mega-Trend of All

Last year, it generated $8 billion in global revenues. By 2020, it's predicted to blast through the roof to $47 billion. Famed investor Mark Cuban says it will produce "the world's first trillionaries," but that should still leave plenty of money for regular investors who make the right trades early.

See Zacks' 3 Best Stocks to Play This Trend >>

AvalonBay Communities, Inc. (AVB): Free Stock Analysis Report

HCP, Inc. (HCP): Free Stock Analysis Report

Piedmont Office Realty Trust, Inc. (PDM): Free Stock Analysis Report

CyrusOne Inc (CONE): Free Stock Analysis Report

Original post