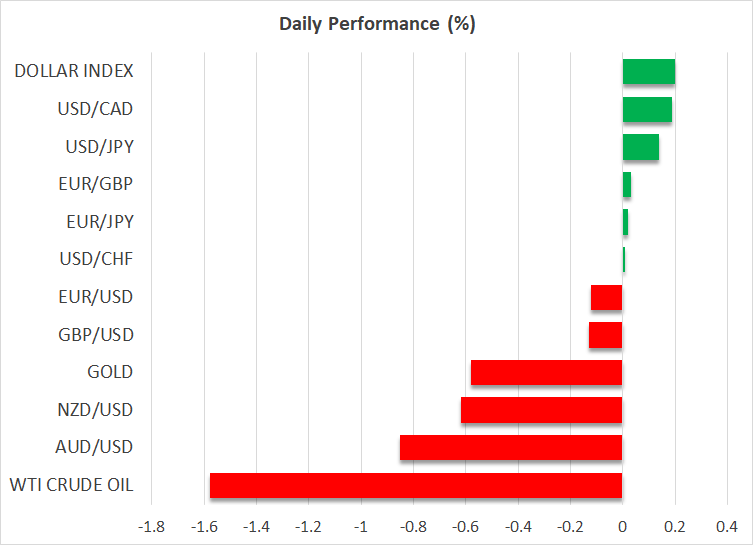

- Dollar regains some lost ground as US yields bounce back

- Gold and oil edge lower - geopolitical risks getting priced out?

- Aussie sinks despite RBA rate increase, Fed speakers ahead

Dollar back in the ring

Global markets continue to grapple with a variety of risk factors, from geopolitical tensions to a softer economic data pulse, although the most pressing question for traders is whether yields on government bonds have peaked for this cycle.

Yields are essentially the price of money, so sharp movements in the bond market have similar effects to a central bank raising or cutting interest rates. Several elements came together last week to engineer a heavy decline in US yields, as data releases disappointed and the Treasury announced a shift in its debt issuance towards shorter-dated bond maturities.

But this week, the tables have turned and yields are marching higher once again, helping to breathe life back into the US dollar while dampening demand for non-yielding assets like gold.

In terms of economic performance, the US dollar still has the upper hand over other currencies. Even accounting for signs of an impending slowdown in growth and slightly looser labor market conditions, the US economy remains stronger than other regions such as Europe, where downside risks have started to materialize.

Gold and oil prices slide

Over the past month, gold and oil prices have acted as barometers for geopolitical tensions in financial markets, as the risk of escalation in the Middle East simultaneously fueled safe-haven demand and raised concerns about disruptions in local energy production.

Judging by the recent declines in gold and oil prices, it seems that investors are becoming less concerned about geopolitics, as it becomes increasingly clear that Iran doesn’t want to get dragged into this conflict.

Gold has been trading with relative weakness since last week, when it could not advance even as US yields cratered and the dollar was sold off, which on paper is a bullish recipe for bullion. Hence, it appears these positive effects were eclipsed by something even stronger, most likely speculators unloading gold positions as the geopolitical risks did not intensify.

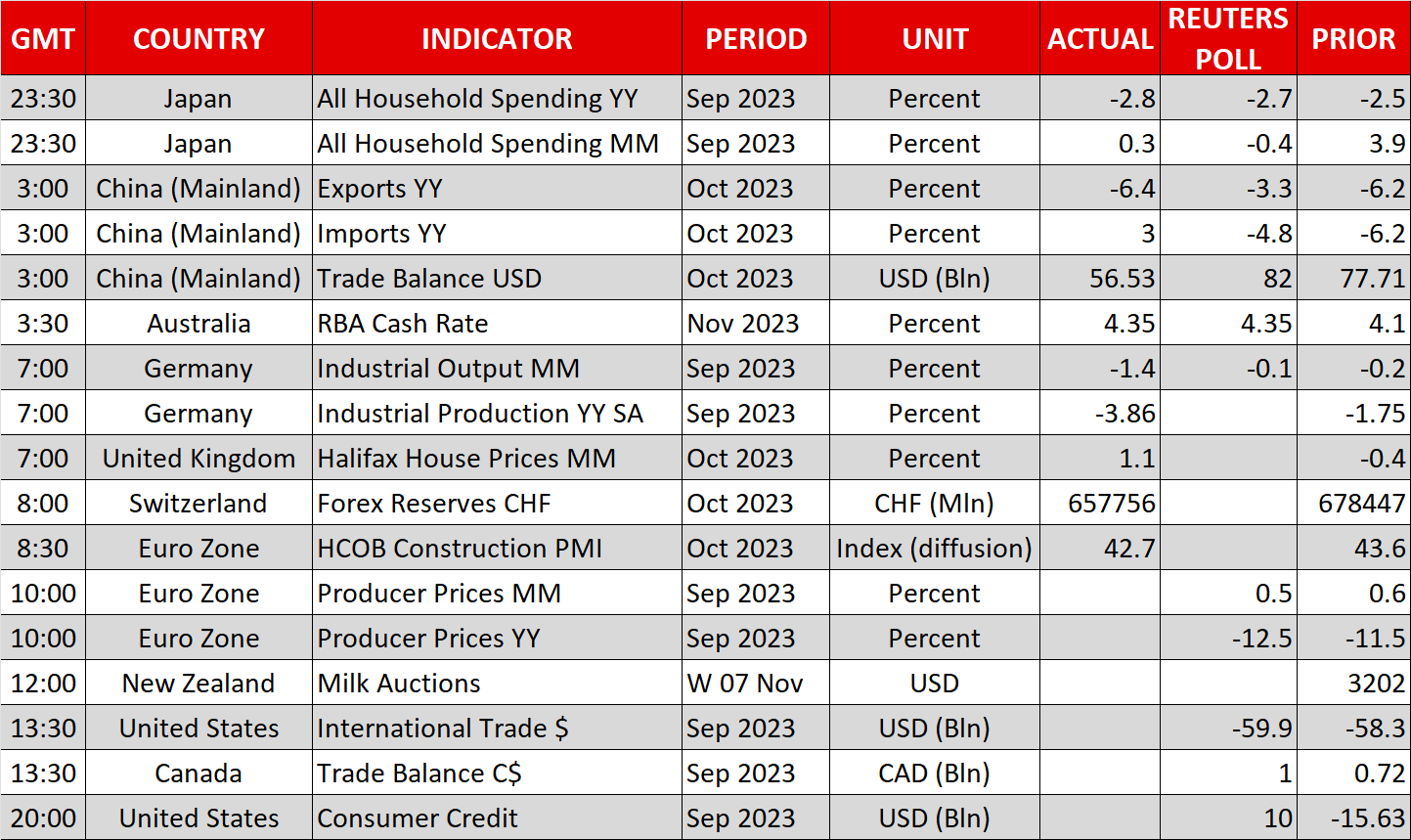

It is equally striking that oil prices have fallen to their lowest levels since late August, even after Saudi Arabia and Russia reaffirmed their commitment to their voluntary supply cuts until the end of the year. As such, the geopolitical risk premium embedded into oil seems to be getting priced out, and the disappointing export data out of China earlier today added fuel to the selloff by painting a picture of weakening global demand.

RBA disappoints, Fed speakers next

As expected, the Reserve Bank of Australia raised interest rates today, citing more persistent inflationary pressures. However, the central bank also toned down its forward guidance, introducing an element of uncertainty about whether any further rate increases are needed.

The end result was a sharp drop in the Australian dollar, as money markets were fairly confident the RBA would deliver another rate increase next year, prior to this event. Instead, the RBA adopted a more neutral stance and emphasized data dependence. With the rate outlook taking a back seat, the aussie will turn its focus back to global risk sentiment and China developments.

As for today, the data calendar is low-key but there’s a parade of Fed speakers on the agenda to spice things up, with Barr (14:00 GMT), Schmid (14:50 GMT), Waller (15:00 GMT), and Williams (17:00 GMT) all scheduled to speak.