Last week we saw the most significant JPY rally attempt yet, though USDJPY has already taken back about half of the lost ground. EURUSD has been slower to recover after last week’s ECB meeting.

The week should be starting quietly with Asia out on the Chinese New Year and a Japanese holiday as well, but JPY crosses have been on the move and AUDUSD sell-off renewed overnight as well. It’s going to be an interesting week as we head towards the BoJ meeting on Thursday and the G20 meeting on Thursday/Friday. Even within Europe, there is little apparent agreement on what kind of response is necessary to the strong Euro (which may yet resolve itself if tail risks come back or if the ECB is forced to employ the OMT as a peripheral country asks for a bailout). France’s Hollande has already protested recently about the Euro’s strength and Japan’s policy, while German officials have brushed off the Euro strength as not a problem – maybe not for Germany, but certainly for the rest of Europe!

Meanwhile in Japan, the latest rhetorical support for a weaker JPY came from potential BoJ candidate Kuroda, currently of the Asian Development Bank, who said that the inflation target is appropriate for Japan and that the yen weakening is a natural adjustment after excessive strength. It is interesting that he said that monetary policy alone would be sufficient to achieve the goal, as Abe has also stressed the importance of fiscal stimulus.

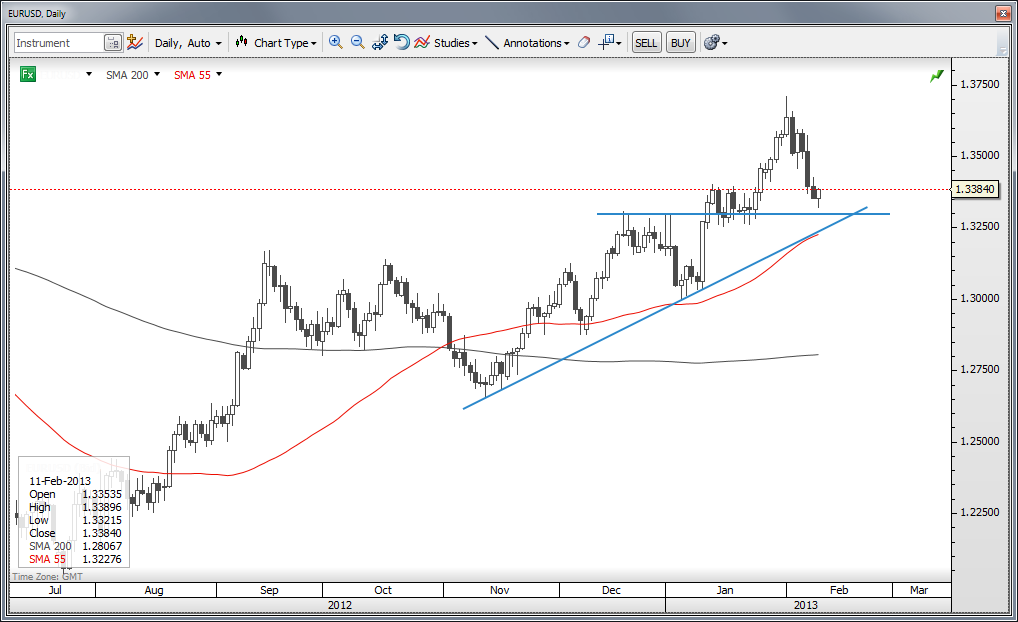

Chart: EURUSD

The Euro closed last week with its weakest performance since it put in a low last summer, even as the ECB meeting saw Draghi not fully engaging in the competitive devaluation theme. The lows this morning near 1.3330 saw the vast majority of the 445-pip rally from 1.3265 to 1.3710 unwound, which serves as a powerful bearish counterattack. This was not yet a fatal blow, but the force of the retreat has me looking for signs that the rally since last July is over. We had a false indicator of the same back at the very beginning of the year, but then the massive rally on 10 January turned things back around. We still have channel-like support in place, so the bears still need to see the 1.3300/1.3270 area taken out to more fully break the back of the rally. To the upside, the local resistance is from the daily pivot at Asian highs (1.3395 area) up to about 1.3450. EUR/USD" title="EUR/USD" width="1018" height="622">

EUR/USD" title="EUR/USD" width="1018" height="622">

Looking ahead

In the US, look out for Fed vice-chair and ultra-dove Janet Yellen, who is out speaking later on the US recovery and the Fed’s response. The looming Fed appointment this summer will be quite a spectacle, especially if the hard core of the Republican party decides to make things interesting. Some consider Yellen the heir apparent to the Fed Chairman’s seat, but it is hard to imagine the political opposition won’t seize the moment to make a fuss. It will be interesting to hear her rhetoric after surprising rhetoric from one of her traditionally very dovish colleagues, Mr. Evans of the Chicago Fed, last week.

The US data highlights this week include Wednesday’s Retail Sales report. At some point, if not for the January data, then certainly in the coming few months, one would expect an ugly hit to spending because of the high cost of petrol in the US (for this time of year more than in absolute terms, remember that most US data seasonally adjusted), but more so due to the end of the payroll tax cut and the higher tax rate on the highest incomes that provide a disproportionate amount of spending. Later in the week, we have the Empire manufacturing on Thursday and the first look at February University of Michigan Confidence on Friday.

The BoJ is up on Thursday. With the G20 getting under way the same day and after the last meeting’s dramatic policy statement change, it’s doubtful we see much of substance as the speculation shifts to who will replace Shirakawa in March.

This week could be a pivotal one for the increasingly lively politics of exchange rates as the G20 meeting is up beginning this Thursday in Moscow. It will prove a very interesting occasion to test whether Japan’s move has dented diplomatic politeness and international relations. We’ll all have to do a great deal of reading between the lines to measure the mood. I’m particularly curious about how China will eventually respond to Japan’s devaluation attempt. It was, after all, China’s massive 1994 devaluation that helped to touch off the Chinese economic miracle, and the CNY/JPY rate is at its highest since late 2008.

Economic Data Highlights

- UK Jan. Lloyds Employment Confidence out at -45 vs. -42 in Dec.

- Australia Dec. Home Loans fell -1.5% MoM vs. 0.0% expected

- Norway Jan. CPI out at -0.2% MoM and +1.3% yoY vs. -0.4%/+1.1% expected, respectively and vs. +1.4% YoY in Dec.

- Norway Jan. CPI Underlying out at -0.5% MoM and +1.2% YoY vs. -0.4%/+1.0% expected, respectively and vs. +1.1% YoY in Dec.

- US Fed’s Yellen to Speak (1800)

- New Zealand Jan. REINZ Housing Price Index (2030)

- New Zealand Jan. Card Spending (2145)

- UK Jan. RICS House Price Balance (0001)

- Australia Jan. NAB Business Conditions/Confidence (0030)

- Japan Jan. Consumer Confidence (0500)

- Japan Jan. Machine Tool Orders (0600)