Tuesday March 8: Five-things the markets are talking about

Global challenges remain in place for emerging markets and continue to weigh upon market risk appetite.

Regional equities are on the back foot, along with U.S. stock index futures this morning, while crude and other commodity prices fall as reports overnight revealed that Japan’s economy and Chinese exports are shrinking. Safe-haven assets, including yen, gold and U.S. Treasuries remain better bid.

1. China trade disappoints

China’s trade balance has hit a ten-month low in yuan terms: February Trade balance – ¥209.5b vs. ¥341b; Exports y/y: -20.6% vs. -11.3%e (the biggest decline since May 2009); Imports y/y: -8.0% vs. -11.7%e.

In dollar terms, both missed consensus. Exports fell for the eight-consecutive month by -17.8% vs. -14.5%e and imports for the 16-month in a row by -16.7% vs. -12.0%e.

Shipments to the U.S, EU, and Japan were all down about -20% y/y.

With such disappointing data like this, its no wonder that China’s Premier Li decided to skip 2016 projections for the trade component of the economy on the weekend (China’s Peoples Congress). The export data in particular would suggest that the markets recent hopes for a global rebound perhaps needs to be somewhat tempered again.

The People’s Bank of China (PBoC) continues to keep forex traders guessing. Authorities again overnight set the yuan mid-point at ¥6.5041 vs. ¥6.5113 prior (the strongest setting since Jan 4th and the fourth-consecutive stronger setting).

2. Japan’s Q4 GDP confirmed back in contraction

Japans economy has confirmed contraction for the second-time in three-quarters.

The GDP declines in the final prints were revised to be smaller with mixed component trends. Capex (capital expenditure) was stronger than expected at +1.5% vs. +1.2%e and vs. +1.4% preliminary, while consumption was slightly weaker at -0.9% vs. -0.8%e vs. -0.8% preliminary.

The trade numbers were unrevised with a -0.9% drop in exports and -1.4% decline in imports q/q. Comments by Economic Minister Ishihara after the release, maintained that there is no change to the view of Japan fundamentals. They remain solid, noting weakness in consumption but also pointing to recovery in corporate profits and incomes.

With Japan’s data points showing no real signs of improvement might persuade PM Abe’s cabinet to consider pushing back the timing of second round of sales tax increase. Currently, they are slated for April 2017.

3. Bank of England (BoE) Chief Testifies to MP’s on EU membership

BoE Governor Carney testified to the U.K’s Treasury Select Committee that he would not provide comprehensive analysis of the economic ‘pros and cons’ of EU membership. Membership brings risks as well as benefits to the U.K.

He reiterated that it was in the U.K’s interest that European monetary union was placed under sounder footing. Remaining in the EU posed risks related to development of eurozone, most recently during the eurozone’s debt crisis.

He added that the BoE has not carried out a comprehensive assessment of the economic impact on the U.K of leaving the EU. However, the Governor indicated that the U.K’s new deal should help it achieve its twin objectives of maintaining low and stable inflation and preserve financial stability.

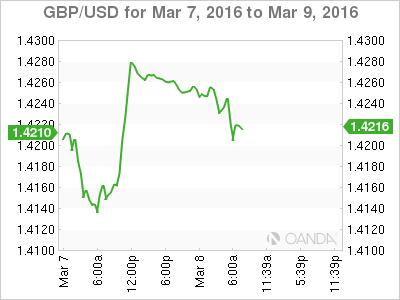

Note: Sterling (£1.4220) rallied hard Monday after the BoE said it would provide extra liquidity in the days surrounding the June 23 referendum.

4. EUR Bears feeling the pinch

Currently, USD ‘bulls’ are left wondering what happened. One of this years go to favorite trades is not going as planned – the EUR (€1.1007) is up on the year outright.

The Fed is back in play after a good month’s U.S data. It seems that traders have got the ‘policy divergence’ theme correct, but the FX outcome wrong. The USD is well off its recent highs despite a new wide’ in U.S rate differentials vs. Europe and Japan. What will be most interesting to the market is how EUR/USD will trade after the expected ECB cut this Thursday.

The ECB meet is expected to result in new stimulus measures that could include another interest rate cut and/or new spending on bond buying. Despite the threat, the EUR/USD continues to drift higher as participants hedge against any potential ECB disappointment. The market is wary of a December Draghi repeat – under deliver.

With crude oil prices +40% higher off its January lows could temper some of the ‘dovish’ voices at the governing council is certainly a threatening factor for the bear.

5. Aussie dollar raises a warning flag

With the AUD (A$0.7481) strengthening to an eight-month high is prompting some concerns with RBA officials. Deputy Governor Lowe stepped in overnight to talk the currency down (A$0.7423).

He noted that “monetary easing abroad is a complication for us, as it tends to put downward pressure on currencies were the easing is taking place and thus upward pressure on the AUD.”

With Lowe and company expecting further easing abroad, will the Reserve Bank of Australia (RBA) need to be proactive in manipulating their currency’s value? Year-to-date, the Aussie has rallied +7% outright.

Other RBA voting members have indicated that they would prefer the AUD to be trading near A$0.6500. A strong dollar will only continue to dent the Aussie’s economy. It’s difficult to see a vocal Central Bank posing idle threats when a stronger AUD poses both economic and inflation expectation threats.