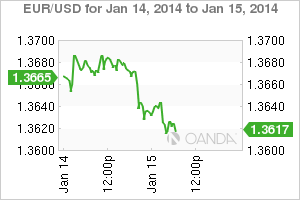

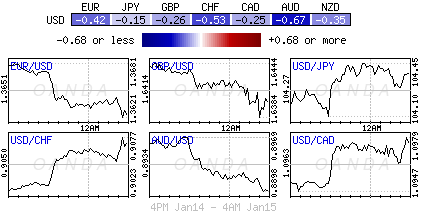

A certain relief to dollar bulls is that after a two day hiatus the "buck is back" and in favor across the board for now at least. Yesterday's stronger than expected US retail sales data should have been capable of lifting economic sentiment that was tainted somewhat after last Fridays non-farm payroll report and given the USD an immediate lift. However, so far in this new calendar year nothing is coming easy to those dollar "weak" long positions. The immediate dollar follow through did not transpire; instead the techies moving averages had the dollar bulls sweating as they limited the 18-member single currency's dips, allowing risks to remain to the topside for anyone long the dollar. Since last Friday's dismal North American employment reports, the market has been trying to get long the EUR on dips. Failing to do so had lead to speculators becoming even more aggressive and bidding up the EUR. EUR/USD" border="0" width="600" height="600">

EUR/USD" border="0" width="600" height="600">

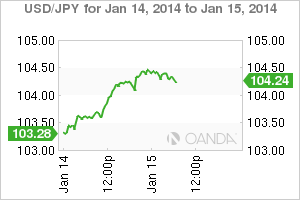

There should have been a good opportunity yesterday, immediately after a stronger December US retail sales print (core +0.7%) to purchase EUR's. The chance did not transpire, even with retail sales pushing ahead last month despite the huge drop-off in auto-sales (down -1.8% - dragging down broader figures). The total retail sales for 2013 were up +4.2% from the prior year, a slowdown from the 2012's pace of +5.4%. The Fed's go-to, the US consumer, has again remained resilient and this despite higher taxes and a brief loss of confidence in Washington during the government shutdown. A rampant equity market and rising house prices have buoyed households. With overall debt burdens down, has led to an increase in disposable incomes, and certainly paves way for stronger expectations for this year. Any increase in core spending would suggest that consumption activity could provide a meaningful boost to economic activity for Q1.  USD/JPY" border="0" width="600" height="600">

USD/JPY" border="0" width="600" height="600">

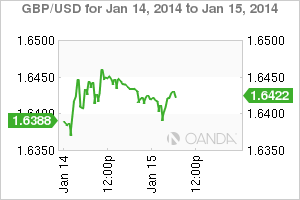

Instead, it has taken the World Bank to modify their global growth projection to bring the USD back into the fold, temporarily at least. The World Bank has raised its 2014 GDP projections to +3.2% from a +3.0% prior forecast on the strength of economic recovery in developed economies; the Euro-zone and Japan have been upgraded +0.2pts to +1.1% and +1.4% respectively, while the US GDP forecast is maintained at +2.8%. Concurrently, World Bank officials have cut China's GDP target to +7.7% from +8.0% and Brazil's by -1.6pts to +2.4%. The overall developing nations 2014 GDP forecast has been reduced to +5.3% from a +5.6% prior. Numbers like these give the perception that the global economy is probably strong enough to withstand scaling back stimulus measures. So far, the mighty dollar has managed to strengthen against all of its 16 major peers as global equity bourses trade in the black, with investors happy to take on more risk. GBP/USD" border="0" width="600" height="600">

GBP/USD" border="0" width="600" height="600">

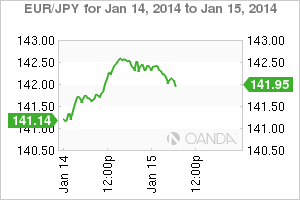

On the surface, many investors have been drawn into the minutia of a contained trading range. Uncertainties cast by the lackluster payroll report last week and the ECB's Nowotny's optimistic take on the Euro-zone yesterday, so soon after Draghi's dovish words, could be considered a powerful ingredient to counter-trade the 18-member single currency, especially with a further drop in volatility (now hovering at a seven-year low). Such low vols would suggest that the immediate currency moves should remain relatively contained. The dollar bulls were well positioned ahead of last Friday's NFP for that downside break in the EUR. A move that never transpired as lower US yields and more bullish EUR technicals created that necessary stopgap, allowing the weaker dollar longs to be caught offside.  EUR/JPY" border="0" width="600" height="600">

EUR/JPY" border="0" width="600" height="600">

The EUR’s use as a “funding” currency is not forgotten, benign inflation, interest rate differentials, a dovish ECB; a hawkish Fed cannot be lost on the EUR's value. There are still strong fundamental reasons to be short the currency, as rallies are probably not sustainable. Overall, the negatives outweigh the positives. Give it time, the growing monetary policy divergence is expected to become more of a USD supporter over the coming months. Too many investors get caught up in the noise and eventually get lost in that noise. Data watching will continue to take a prominent role.

Macro selling has led the EUR slide overnight, whilst the algo's stops have added to that negative momentum. The techies require a EUR close below 1.3540 to shift the market back into a new bearish trend. The Euro-zones trade surplus numbers (+€16b) this morning should have been more positive for the single currency, however, when the boost to growth is reflected in a decline in imports rather than a pickup in exports generally does not stop a currency bleed quiet as fast. Yesterday’s US retail sales figures showed that consumer spending is picking up, certainly a counter trend to a weak jobs report. Perhaps now investors will feel more comfortable viewing last week's NFP print as an outlier and remain bullish on the USD?

Original post

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Forex Consolidation Or Is the Buck Back?

Published 01/15/2014, 07:42 AM

Updated 03/05/2019, 07:15 AM

Forex Consolidation Or Is the Buck Back?

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2025 - Fusion Media Limited. All Rights Reserved.