Fireeye Inc (NASDAQ:FEYE) released first quarter 2015 earnings on April 30, beating estimates for both revenue and earnings per share. The cyber security firm went public in 2013 and expects to be become profitable in the next three to five years.

The cyber security sector has drawn more attention from analysts and investors following recent high-profile cyber attacks, such as the Sony email leak in November. FireEye was hired to assist Anthem Health Insurance when the company was hacked in February, which impacted up to 70 million people. In the quarter, FireEye announced partnerships with HP and Check Point to rectify threat response platforms.

FireEye posted first quarter revenue of $125.4 million, beating the analyst consensus of $120.6 million and marking a 69% year-over-year increase. Combined product revenue and product subscription revenue made up half of total revenue. First quarter billings increased 53% year-over-year though the average contract length for new subscriptions was consistent with the first quarter of 2014. FireEye posted non-GAAP loss per share of ($0.48), ahead of the analyst estimate of ($0.51).

Looking forward, FireEye provided updated guidance on second quarter earnings and full-year 2015 outlook. In the next quarter, FireEye expects to post total revenue between $140 million and $144 million with a loss per share between ($0.47) and ($0.50). For full-year 2015, FireEye expects to post total revenue between $615 million and $635 million with a loss per share between ($1.75) and ($1.85). This outlook beat estimates of $619.8 million in revenue and ($1.86) loss per share.

Analysts released a slew of mixed ratings following the earnings report.

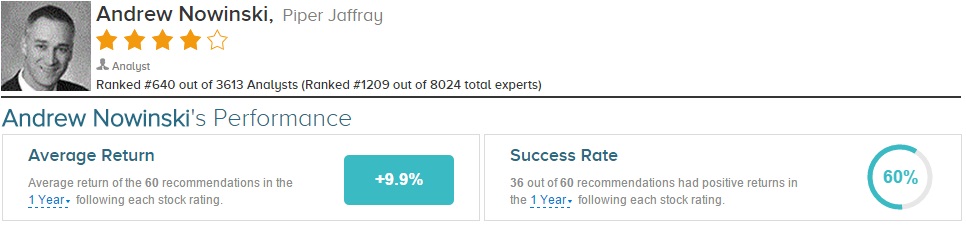

Andrew Nowinski of Piper Jaffray reiterated an Overweight rating on FireEye and raised his price target from $45 to $50.Nowinski commented, “FireEye is one of the most innovative companies within the security market and with an expanding portfolio of products, now has many more routes-to-market. This should enable the company to continue gaining market share and to deliver 40%+ revenue growth for the foreseeable future.” Nowinski also noted that Mandiant, a computer forensics company acquired by FireEye last year, had a “90%+ attach rate of products and subscriptions” in the quarter and is running at full capacity in North America.

Andrew Nowinski has rated FireEye 4 times since August 2014, earning a 75% success rate recommending the stock with a +19.4% average return per FEYE recommendation. Overall, Nowinksi has a 60% success rate recommending stocks with a +9.9% average return per rating.

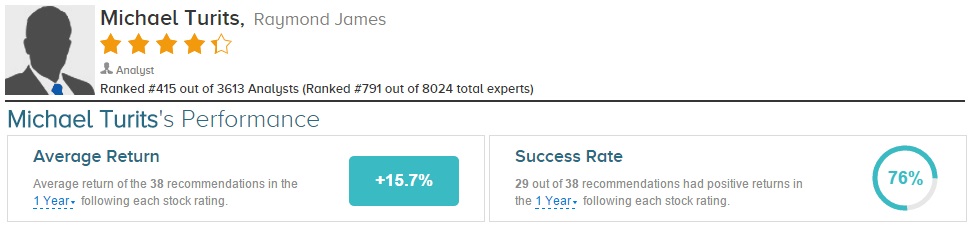

Separately after earnings, Michael Turits of Raymond James reiterated a Market Perform rating on FireEye. Turits noted that FireEye has “built the dominant franchise in APT defense and continues to take advantage of a strong security spend environment” and he expects “continued strong near-term growth.” However, the analyst also noted several risks such as uncertain TAM, increasing competition, and steep CFFO and EBIT losses. Turits believes the company is fairly valued and raised his 2015 revenue estimate from $617 million to $627 million.

This is Michael Turits’ first time recommending FireEye. Overall, Turits has a 76% success rate recommending stocks with a +15.7% average return per rating.

On average, the top analyst consensus for FireEye on TipRanks is Hold.