- Fed hikes by 25bps, but turns data dependent

- Dollar extends slide as investors price in a June pause

- ECB to hike by 25bps as well, focus could fall on Lagarde

- Wall Street and oil prices slide, gold nearly hits its record

Dollar falls as Fed seen pivoting during summer

The US dollar continued to weaken across the board yesterday, with the slide extending into the Asian session today as the Fed watered down its forward guidance, prompting investors to price in a pause at the next gathering.

The Committee delivered the broadly anticipated 25bps hike, but in the statement accompanying the decision, officials removed the part saying that some additional policy firming may be appropriate and instead said that in determining whether more hikes may be needed, they will consider the cumulative tightening of monetary policy, the lags with which policy affects the economy and inflation, and incoming economic and financial developments.

In other words, they turned data-dependent, with Fed Chair Powell confirming that at the press conference he held after the decision. However, he also said that the process of getting inflation back to 2% has a long way to go and that they remain prepared to do more if warranted. At the Q&A session, he added they didn’t decide on a pause at this gathering, something that they could do in June.

The softening of the forward guidance pushed the US dollar lower initially, but the currency found some footing during Powell’s press conference, perhaps as he refused to close the door to a June hike. Having said that though, it was all south for the greenback thereafter as market participants were convinced that a pause is the most likely outcome for June. Now, they are also pricing in 80bps worth of rate reductions by the end of the year, something that could keep the dollar on the back foot for a while longer, at least until the June decision.

Will Lagarde sing the same hawkish song?

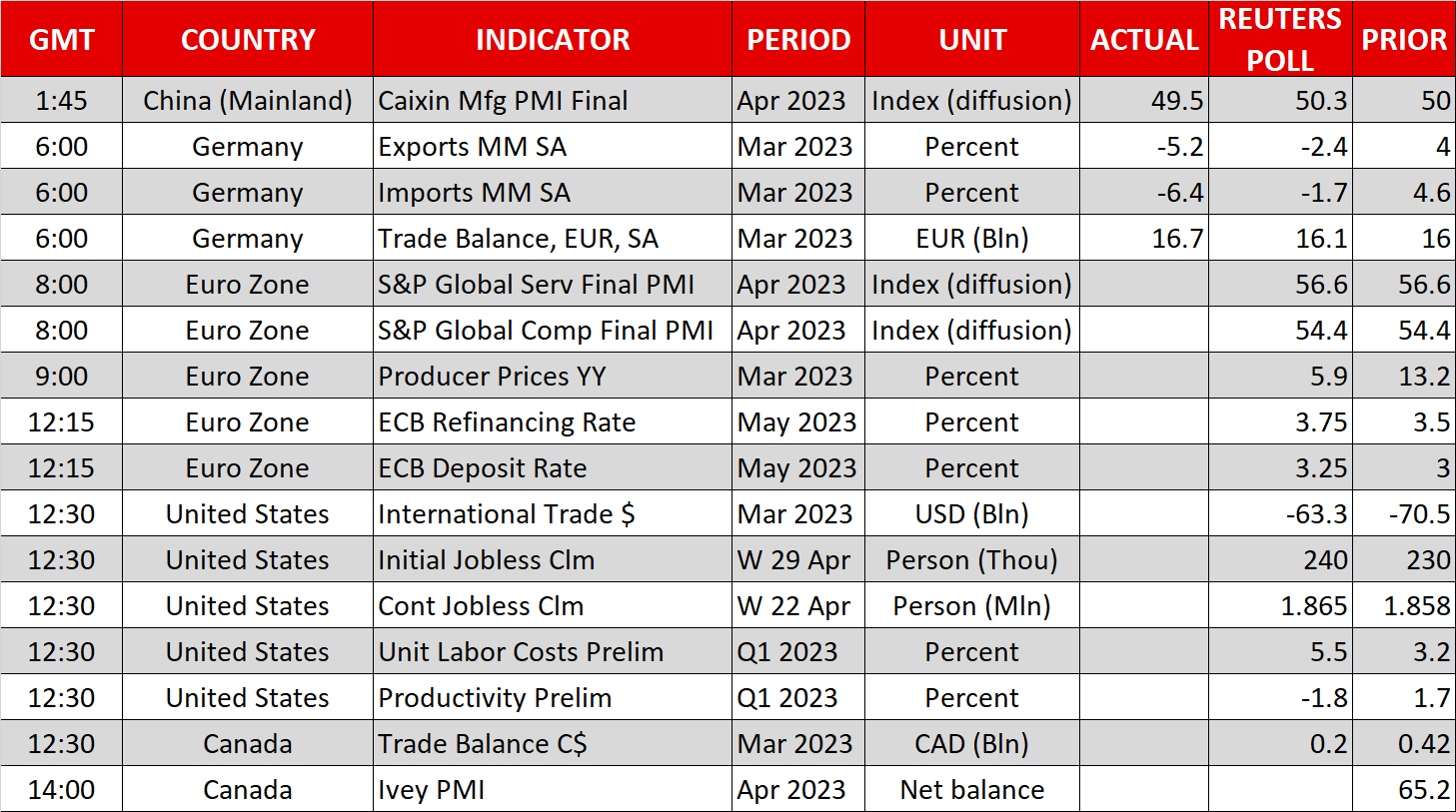

Today, the central bank torch will be passed to the ECB, which is also expected to hike by 25bps. According to money markets, investors assign a nearly 80% probability to that scenario, with the remaining 20% pointing to a 50bps increment. Taking that into account, a quarter-point hike may come as a disappointment to those expecting a bigger increase, and thus, the initial reaction in the euro may be to the downside.

However, President Lagarde has been repeatedly emphasizing that underlying price pressures remain elevated and that she and her colleagues need to do more, prompting the market to price in a total of nearly 75bps worth of additional rate hikes henceforth. Thus, should she sing the same hawkish song, any decision-related slide in the euro might stay limited and short lived.

With Fed funds futures pointing to rate cuts in the US later this year, the divergence in monetary policy between the ECB and the Fed could continue to benefit euro/dollar. For the uptrend to start being seriously questioned, investors may need to see signs that the ECB might underdeliver or be convinced that the Fed will not cut rates later this year, even if it doesn’t proceed with any more hikes.

Wall Street slides on recession worries, gold flirts with record

Strangely, Wall Street finished yesterday’s session in the red, despite the market fully pricing in a pause at the June FOMC meeting. Perhaps investors remained more concerned about the performance of the US economy rather than being happy with the prospect of better present values. This is also evident by the fact that oil prices tumbled by another 5% yesterday.

The blend of economic concerns, sliding Treasury yields, and a weak dollar, allowed gold to shine again. The precious metal nearly touched its record high of 2,072.50, hit back in August 2020, before pulling back during the Asian trading session today. With investors remaining fearful about a recession in the US and expecting a series of rate cuts later this year, the precious metal may be poised to turn north again soon and eventually enter uncharted territories.