- Dollar slumps again amid more signs of US slowdown, core PCE next

- Euro see-saws after mixed CPI numbers

- Stocks extend rally on fading Fed hike expectations, China stimulus

Dollar pummelled as soft US data streak continues

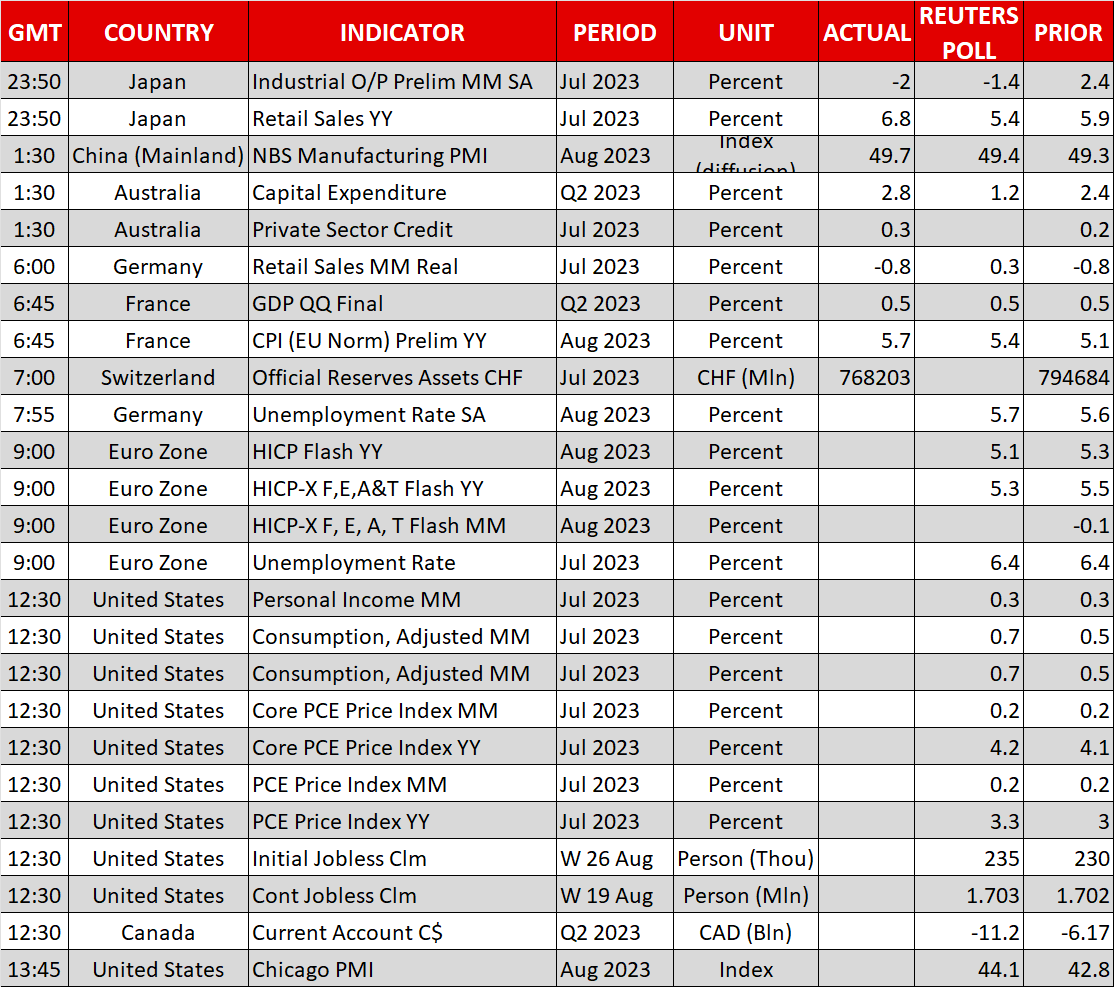

Expectations of further tightening by the Fed diminished further on Wednesday after more data pointed to a slowing economy in the United States. Hot on the heels of Tuesday’s unexpected drops in job openings and a key gauge of consumer confidence, the ADP employment report also disappointed yesterday, while GDP growth for the second quarter was revised slightly lower.

Private employment increased by a less than forecast 177k in August according to ADP, fuelling speculation that Friday’s nonfarm payrolls print will also fall short of estimates. The focus on Thursday, however, will be on the core PCE price index, which the Fed tracks for its inflation objective.

Whilst the data that’s come out so far this week has cast doubt on just how resilient the US economy really is, today’s reports could have the opposite effect. The core PCE price index is expected to have edged up to 4.2% y/y in July from 4.1%, which would indicate that the journey to reaching 2% inflation is going to be a slow one, bolstering the higher for longer case.

Personal income and spending numbers are also due and could show consumption jumped by 0.7% m/m in July, signalling that Americans are upping their spending rather than cutting back.

Bad news is good news for stocks

After the market probability for one final rate hike from the Fed shot up to 65% after Powell’s Jackson Hole speech, those odds have now been mostly reversed. Investors now see a slightly less than 50% chance that the Fed will raise rates in November, while rate cut bets for 2024 have been ramped up.

This abrupt swing in market pricing has put a halt to the rally in both Treasury yields and the US dollar. Only last week the greenback scaled 12-week highs against a basket of currencies but was brushing two-week lows yesterday.

Wall Street on the other hand reacted positively to the not-so-strong data as investors grew more confident that the Fed will pause in September and start cutting rates as early as May next year. Of course, much will depend on which way today’s and tomorrow’s releases go, but the upbeat mood is holding for now, with European equities and US futures heading higher.

Encouraging signs from China

Asian equities were mixed however, as lingering concerns about China’s economy pulled Chinese and Hong Kong shares lower despite Beijing stepping up its support for the troubled property sector. The drip-feed stimulus has been gathering pace lately, with mortgage requirements being eased in two of the country’s largest cities, while it is expected that state-owned banks will soon announce a reduction in mortgage rates.

However, those headlines were overshadowed by a warning from China’s largest property developer – Country Garden – that it faces the risk of defaulting after reporting a loss of $6.7 billion.

PMI data for August brought more gloom as the manufacturing sector continued to shrink and there was a further deceleration in services activity. On the bright side, the slump in manufacturing appears to be easing and a rebound may be around the corner.

But until there is more evidence of that, China-sensitive assets such as the Australian dollar are likely to remain under pressure. Still, there was some support for the aussie today from better-than-expected Q2 capital expenditure figures out of Australia.

Euro turns choppy after conflicting CPI data

The euro slid on Thursday, reversing some of this week’s impressive gains, as investors deduced that the somewhat hotter-than-expected preliminary CPI readings for August will be a temporary setback in the fight against inflation.

Headline inflation was unchanged at 5.3% y/y across the euro area in August versus expectations that it would fall to 5.1%. The stronger-than-forecast figure follows similarly worrying flash estimates out of Germany on Wednesday, which boosted the market odds that the European Central Bank will hike rates again in September, pushing the euro higher.

However, traders seem to be reassured by the surprise drop in one of the underlying measures, as CPI that excludes food and energy fell sharply from 6.6% to 6.2%, and are taking that as a sign that Eurozone inflation will resume its downward path in the coming months.

The euro was last trading 0.5% lower, slipping back below $1.09.