EURUSD traded at new four-month lows this morning, even as an official statement tries to take back Dijsselbloem’s ill-advised comments on Cyprus from Monday. But we all know from Juncker of course, that for politicians, “when things become serious you have to lie”.

EURUSD is hitting fresh lows this morning as nothing has emerged to counter the Euro-pessimism generated by the Cyprus banking solution. The latest headlines suggest that capital controls for Cyprus could be in effect for “years”. Still, the euro was bouncing around trying to decide whether it was comfortable at new lows after an E-17 statement declared that the Cyprus bailout solution is not a template for Euro rescues. (The market doesn’t invest much in politicians statements, considering the track-record of Euro officials and the infamous Juncker statement that when things get serious, “you have to lie”.) Other news moving the market this morning was the S&P bond ratings agency putting long term Deutsche Bank debt on negative watch.

GBP

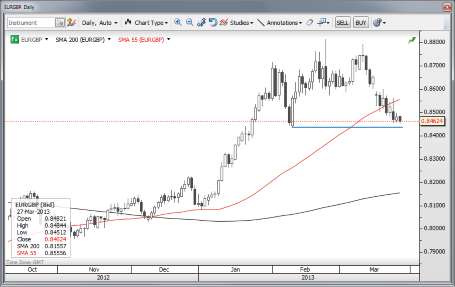

The pound has avoided weakness here as it is still a safe haven from the Euro when the pressure is really on the single currency and the after the market perhaps go too short on sterling trades recently. As well, the language on the BoE’s new remit and inflation yesterday from Osborne suggest that UK leadership will tread carefully around this issue. It doesn’t mean that the UK government or central bank will want a stronger pound, merely that disorderly moves – the recent one bordered on disorderly – are not welcome. For EURGBP, 0.8440 is an interesting area of support that bears watching. Meanwhile, GBPUSD may look towards 1.5000 as the dollar remains preferable.

Chart: EURGBP

The 0.8440 area is a big focus area for obvious reasons. EUR/GBP" title="EUR/GBP" width="455" height="287">

EUR/GBP" title="EUR/GBP" width="455" height="287">

USD

The US dollar was fairly weak yesterday on across the board weak US data – interesting to note that the US currency is responding in “normal” fashion to the strength or the weakness of the data. I don’t think there is much more downside for the greenback on this kind of reaction pattern, as the US currency also remains a safe haven and eventually, if the US growth story proves disappointing, asset markets will have to wake up and smell the coffee and this will tend to favour safe havens.

JPY

Another round of comments from Japanese semi-official quarters (a head of the government’s Economic and Fiscal Policy Council) about the USDJPY and that it should be trading at 100 and could weaken further show that while the official statements focus on inflation, the real focus is on weakening the yen in the hopes that this will revive the Japanese economy. Korean government officials have made noise about asking the G20 to review its policy on currencies as he specifically mentioned the risks from the weak Japanese yen on Korean exports. A former BoJ deputy governor Iwata said that it won’t be possible to achieve the 2% inflation target in 2 years, and maybe not even in 5.

Looking ahead

Again recall that tomorrow is effectively the end of the month/quarter for most of Europe and North America with markets closed for the Easter holiday. And Japan will also likely get most of its trading done in sympathy of where the liquidity is to be found ahead of the end of its financial year on Friday. So we have fixing flows today and through Friday and then repositioning/new trades being put on next week as we run into the Bank of Japan meeting on Thursday and the ECB meeting later the same day.

Economic Data Highlights

- New Zealand Mar. ANZ Business Confidence out at 34.6 vs. 39.4 in Feb.

- Switzerland Feb. UBS Consumption Indicator out at 1.26 vs. 1.15 in Jan.

- Germany Apr. GfK Consumer Confidence out unchanged at 5.9 as expected

- Sweden Mar. Consumer Confidence out at 2.8 vs. 1.0 expected and -1.0 in Feb.

- Sweden Mar. Manufacturing Confidence out at -10 vs. -8 expected and -11 in Feb.

- Sweden Feb. Trade Balance out at +7.1B vs. +2.6B expected and +6.2B in Jan.

- Sweden Feb. Retail Sales out at +1.0% MoM and +3.5% yoY vs. +0.2%/+2.1% expected, respectively and vs. +1.8% YoY in Jan.

- UK Q4 Current Account (0930)

- Italy Jan. Retail Sales (1000)

- Euro Zone Economic/Industrial/Consumer Confidence (1000)

- Canada Feb. Consumer Price Index (1230)

- US Feb. Pending Home Sales (1400)

- US Weekly DoE Crude Oil and Product Inventories (1430)

- US Fed’s Rosengren to Speak (1530)

- US Fed’s Pianalto to Speak (1615)

- US Fed’s Potter to Speak (1630)

- US Fed’s Kocherlakota to Speak (1700)

- New Zealand Feb. Building Permits (2145)

- Japan Feb. Retail Trade (2350)