U.S. markets were sharply lower for the second day in the row. Both the Nasdaq Composite and S&P 500 have seen their biggest losses in almost five weeks. The Republicans and Democrats have reached a deal on a provisional budget. This has raised fears the Federal Reserve Bank will taper back its QE this month.

Late Tuesday, Senate leaders reached a deal that will reduce spending and shave off $23 billion off the deficit over two years. The bipartisan deal still must pass a vote in the U.S. Congress, but is expected to clear this hurdle next Friday. The Senate will then vote on it shortly after and send it to President Obama to sign into law. This will avert another budget shutdown like we had last October and raises the fear, once again the Fed will begin to reduce its QE program during its December meeting instead of the first quarter of 2014.

STOCKS

Overnight, the DJIA lost 129.60 points to close just above 15,800 at 15,843.53. The S&P 500 lost 20.40 points, a 1.13 percent loss, to close at 1,782.22. The tech heavy Nasdaq Composite was also hit hard. This market lost 1.40 percent or 56.68 points to close the day at 4,003.81. We are within stone’s throw of 4,000 and this time 4,000 is support.

Taking a quick look at the CBOE Volatility Index, which gauges investor fear, was up sharply and over 15. This indicates that investors are very worried about the taper and when the Fed will pull the trigger. The QE has been propping up the equities markets for such a long time, that we could see a nice pullback when the taper begins or it will be priced in before it happens.

At this time, Asian markets are red all over. The Nikkei is currently off 1.62 percent to 15,263 and at a new one week low. We are seeing a great deal of profit taking in big cap stocks. On a brighter note the yen has weakened further as the USD/JPY moved higher after hitting 102.35, we are currently at 102.56.

The Australian benchmark fell to an intraday four and half month low before recovering a bit. While still down, losses are not as steep as earlier. We did receive a stronger than expected November jobs report where 21K jobs were created. The estimate was for 10K.

Looking at two emerging markets, the Jakarta Composite fell 1 percent as did shares in the Philippines. These losses come ahead of each of those countries respective central bank meetings. No changes are expected in policy.

CURRENCIES

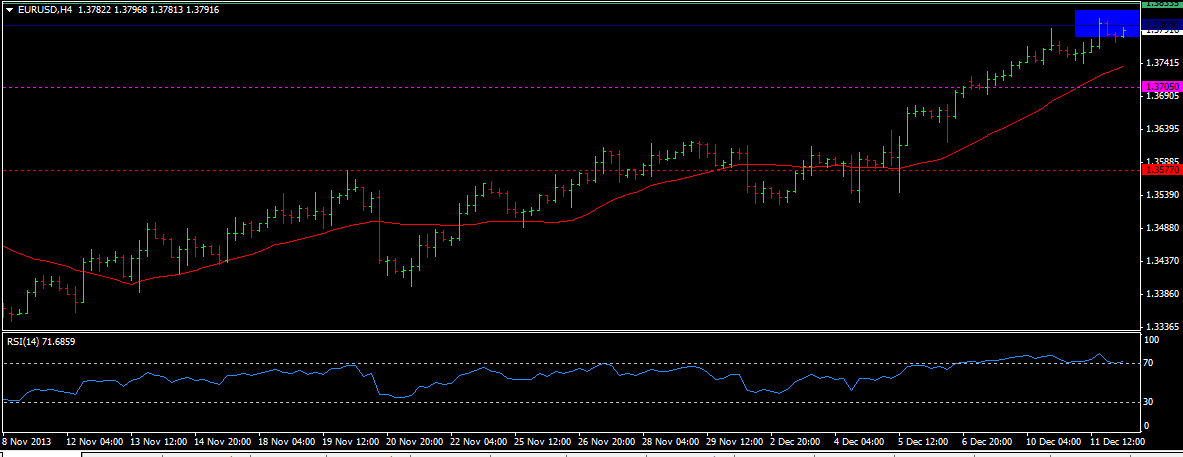

The EUR/USD (1.3791) is moving higher and currently testing 1.38. If this level holds, we can dip to 1.3650 then 1.36. If it breaks, we will see a rally even higher. USD/JPY (102.619) moved lower but has bounced back a bit. If 102.50 holds, we could bounce higher. However, a weaker Dollar, could see support breaking soon which would be bad for the yen.

The GBP/USD (1.636) has moved lower after failing at 1.644. We have moved below a minor support at 1.6350 but remain bullish above 1.6280. USD/INR (61.24) is remaining bearish while below 61.81. We could see some range trading today but we have a strong risk to dip further targeting 60.80 in the coming sessions.

COMMODITIES

Metals are mixed today.

Gold (1254.60) is moving lower and could now test support at 1250 again. We are in a medium range of 1240 to 1270 which has been going on for some time now. We need to break above 1270 to go bullish. Silver (20.285) has fallen but while above 20.25/20.00 we remain bullish. We have support at 19.98/20 which is holding very nicely.

Copper (3.3315) is moving higher. We are targeting 3.35 right now as we stay bullish in this market.

TODAY’S OUTLOOK

The US budget deal will affect global markets as we might see a taper in the QE this month. As for data, the US will release jobless claims, retail sales. We also get business inventories and import and export price data.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Equity Markets Continue To Fall

Published 12/12/2013, 02:49 AM

Updated 05/14/2017, 06:45 AM

Equity Markets Continue To Fall

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2025 - Fusion Media Limited. All Rights Reserved.