- US dollar softer ahead of Powell as US inflation and consumption cool

- Euro regains some posture, stocks look to stretch November gains

- Oil unimpressed by OPEC+ decision for deeper cuts, futures dip

Markets cheer receding inflation

Rate cut speculation went into overdrive on Thursday after inflation in both the United States and the Eurozone fell to levels last seen in 2021, pushing forward the expected timing of when the Fed and ECB will start to ease policy. The drop in Eurozone inflation was the most impressive, with the headline reading falling to within just 0.4 percentage points from the ECB’s 2% target.

Core PCE inflation on the other hand was in line with expectations. But the decline to 3.5% in the Fed’s favourite inflation metric was nevertheless a strong validation of the narrative that interest rates will be cut sooner rather than later.

Investors were also relieved by the slowdown in personal consumption in the first month of the fourth quarter. With the US economy still in very good shape, the upside risks to inflation are far higher in America than in the euro area, which is likely in a recession now. So, the cooldown in spending is seen as lowering those risks.

Dollar eases after data, euro licks its wounds

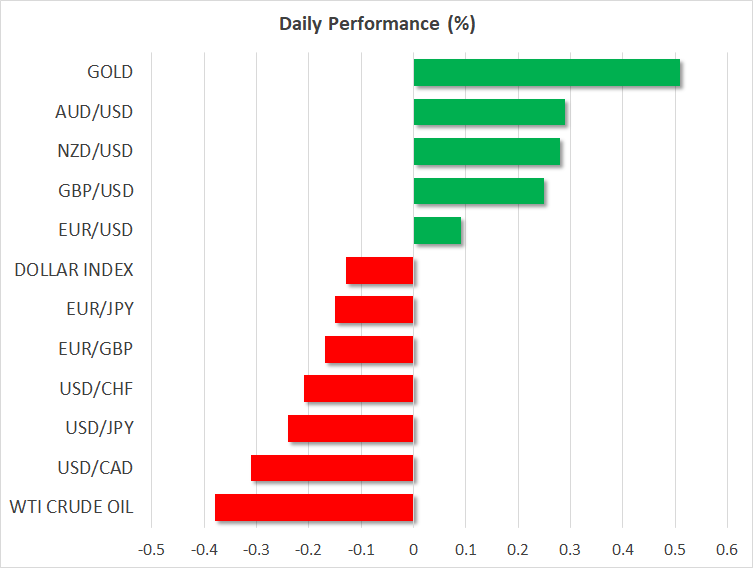

The US dollar didn’t initially react much to the data as the euro’s plunge earlier in the day had triggered a broader rebound in the greenback. But an overdue technical correction likely played a role too and the dollar is on the backfoot again on Friday, having lost 3% of its value against a basket of currencies in November.

The euro, meanwhile, is looking a lot steadier today but remains two handles below where it was on Wednesday when it briefly poked above $1.10.

Its two-month long uptrend against the dollar has come into question following the post-CPI repricing in ECB rate cut expectations as investors see the first ECB cut arriving in April, whereas a Fed rate cut isn’t fully priced in before May.

Still, the looming Fed pivot could yet overpower ECB expectations, not to mention the boost to risk appetite that goes hand in hand with a dovish Fed.

But in the immediate term, the Fed doesn’t seem ready to completely rule out any additional tightening. From the slew of Fed officials that have commented on policy this week, only Waller has so far talked about rate cuts.

If Powell, who is scheduled to make two appearances later in the day, does not join Waller in flagging a possible rate cut within months, the dollar might resume its rebound. Investors will also be keeping an eye on the ISM manufacturing PMI for November.

Stocks kick off December on a positive footing, mostly

In equities, European markets opened sharply higher on the first trading day of December following solid gains on Wall Street yesterday. Rate cut expectations, which have gathered a lot of steam this week, are lifting risk assets, although worries about the earnings outlook are weighing on tech stocks and the Nasdaq bucked the trend to close lower.

The Dow Jones was the surprise winner, hitting its highest level this year after being boosted by a jump in Salesforce (NYSE:CRM) shares on the back of an earnings beat.

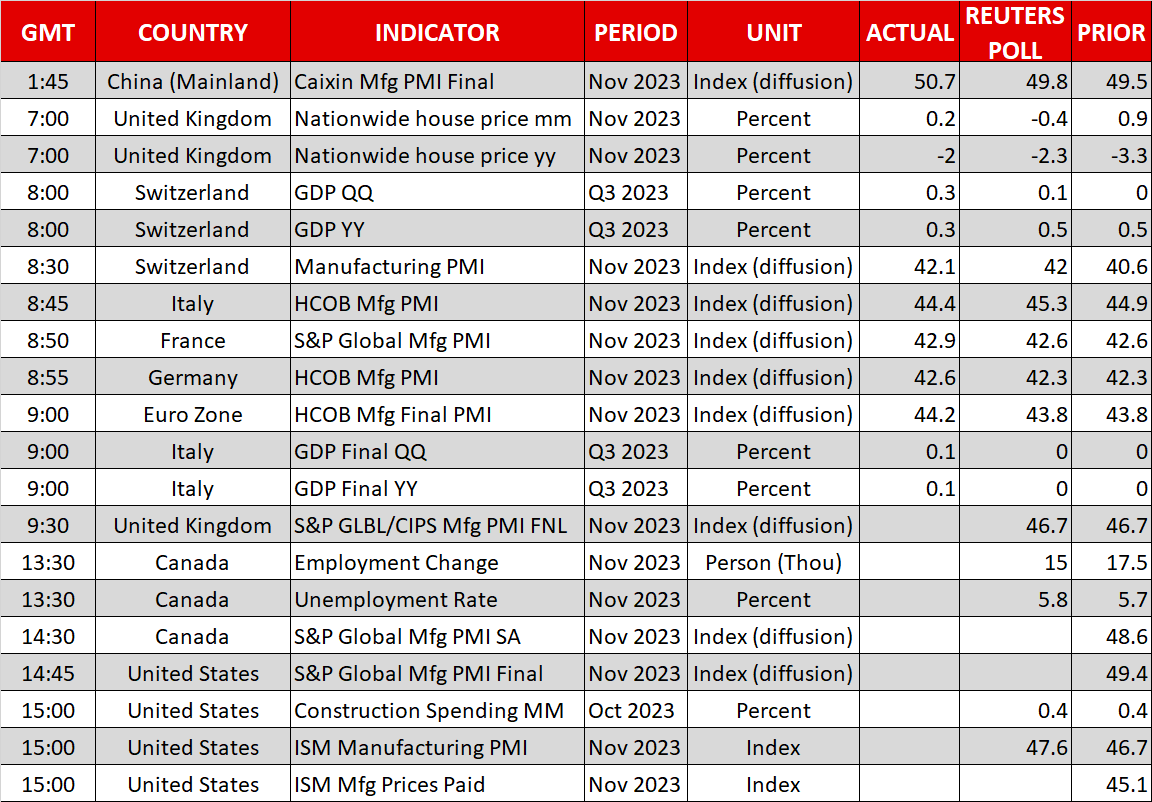

Asian markets were somewhat more downcast today, however, as disappointing manufacturing PMIs in the region dented sentiment, while a bigger-than-expected increase in the Caixin manufacturing PMI failed to ease worries about China’s economy.

Nevertheless, many stock markets around the world had their strongest month of the year in November.

Little changed for oil outlook after OPEC+ cuts

The same cannot be said for crude oil as oil futures declined for the second month in a row. After much speculation, OPEC and non-OPEC countries announced fresh production cuts on Thursday. The OPEC+ alliance surprised many by agreeing to additional cuts of 900,000 barrels a day for the first quarter of 2024, on top of the existing cuts of 1.3 million bpd that have been extended.

But the additional reductions will be implemented on a “voluntary” basis, casting doubt about whether or not members will stick to them as Angola has already rejected a lower quota.

Brent crude futures opened with a gap lower today, coming close to slipping below $80 a barrel, while WTI futures were steady around $75.80 a barrel.