- Fed Chair Powell stresses the need for higher rates

- Dollar rallies across the board, as Fed hike bets surge

- BoC is widely anticipated to stand pat today

- Wall Street feels the heat of Powell’s hawkish remarks

Powell opens the door to higher and faster rate hikes

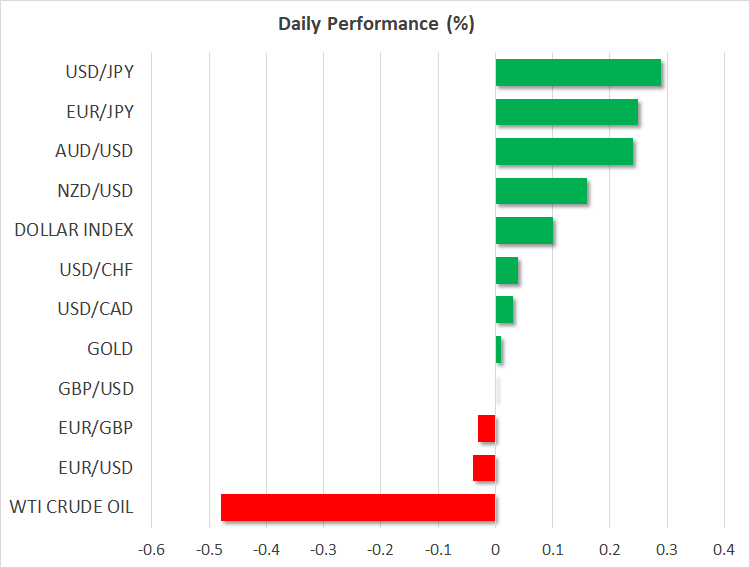

The US dollar outperformed every other major currency on Tuesday and continued to gain against most of them today as well.

The person responsible for the dollar’s rally was Fed Chair Jerome Powell, who at his testimony before the Senate Banking Committee of the US Congress said that the Fed may need to raise rates more than expected and will stand ready to move in larger steps if incoming data warrant tougher action to bring inflation to heel.

Other policymakers have already been vocal about the need for more aggressive action due to recent economic data being stronger than expected. However, Powell’s change of heart from highlighting the disinflationary process to underscoring the chance for larger steps prompted investors to profoundly increase their Fed hike bets. The probability for a 50bps hike at the upcoming gathering has climbed to 70% from 30%, while the level where they expect interest rates to peak was pushed up to 5.65%.

Today, Powell presents the same testimony before the House Financial Services Committee and a reiteration of yesterday’s remarks could keep the dollar supported. Having said that though, the massive increase in Fed hike expectations also heightens the downside risk. Ahead of the next gathering, investors will have to digest the employment report and the CPI numbers for February, due out on Friday and next Tuesday, respectively. Negative surprises in these data sets could well hurt the greenback.

Loonie could suffer against the dollar if BoC appears dovish

Although the dollar gained against all its major peers yesterday, it is hard to envision strong and lasting gains against some of them, one being the euro. Yesterday, an ECB survey showed that inflation expectations among Euro area consumers dropped in January, but expectations for wage growth are still rising, which could well refuel inflation in the coming months. Market participants are still expecting the ECB to deliver another 165 basis points worth of rate increments by the end of the year.

Therefore, the outlook for euro/dollar remains somewhat blurry, despite yesterday’s slide. Maybe the dollar will perform much better against the risk-linked currencies as increasing hike expectations have been weighing on risk sentiment lately. With the slowdown in Canada’s inflation for January and the disappointing GDP data for Q4 cementing expectations that the BoC may refrain from hiking today, the loonie may be the better choice.

Investors are pricing in one more 25bps hike by the BoC until the end of the year and thus, the loonie could come under instant pressure today if officials stand pat and signal that they will likely stay side-lined for the rest of the year unless economic data points otherwise.

Wall Street tumbles, Treasury yield inversion widens

Equities around the globe tumbled after Powell’s hawkish remarks, with Wall Street’s main indices falling more than 1% each on fears that higher interest rates will dent profitability and corporate valuations, as well as the US economy as a whole. The latter is also evident by the fact that the spread between the 2-year and 10-year Treasury yields has fallen to the lowest since 1981.

Surging short-term yields and a strong dollar proved a toxic cocktail for gold, which erased almost all the recovery it staged since February 28. The precious metal is still holding above the 200-day exponential moving average, but a clear dip beneath it could invite more bears into the action.