- Waller says Fed is in no rush to cut rates

- March cut probability slips and dollar gains

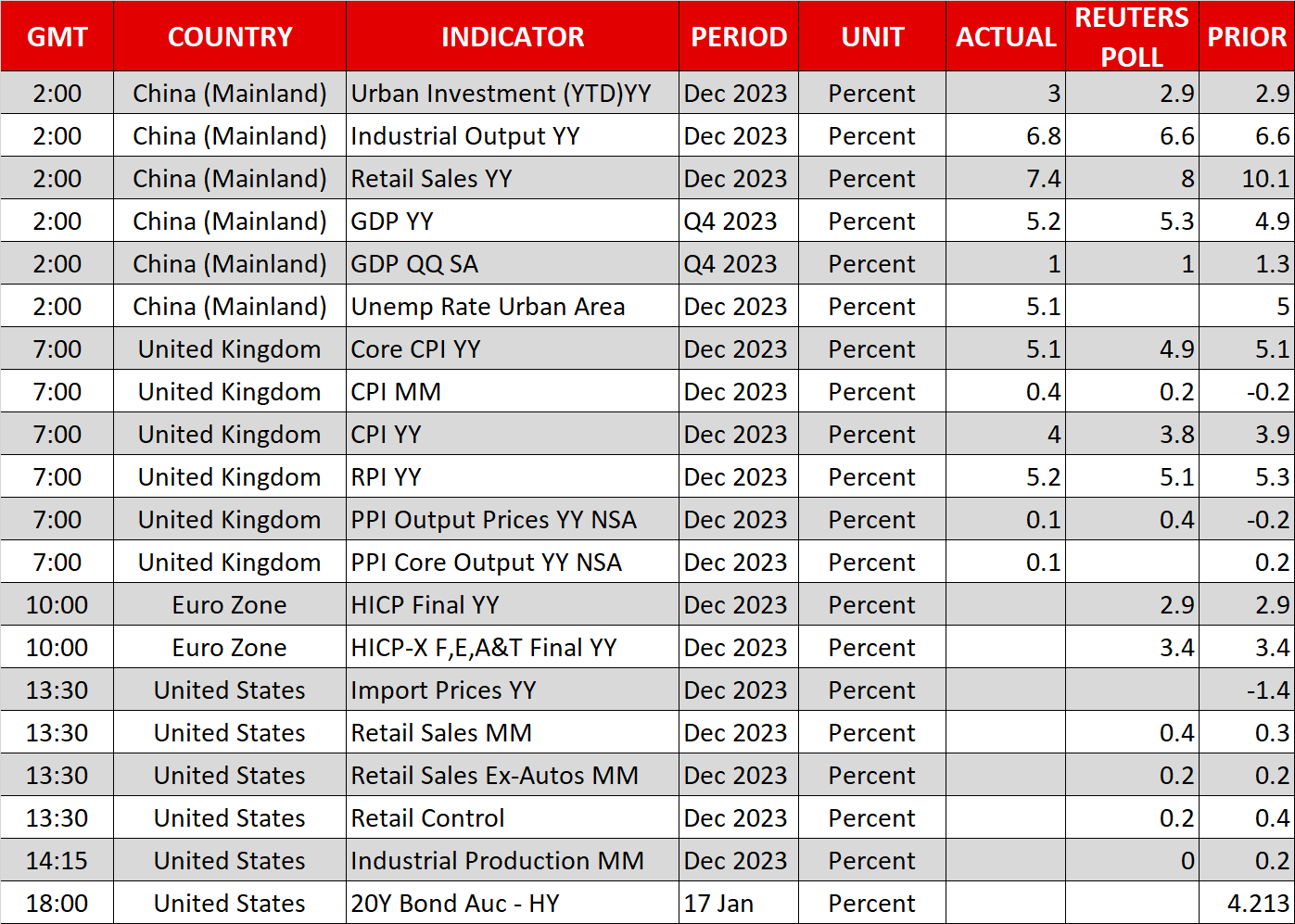

- Pound rebounds after hotter-than-expected UK CPI data

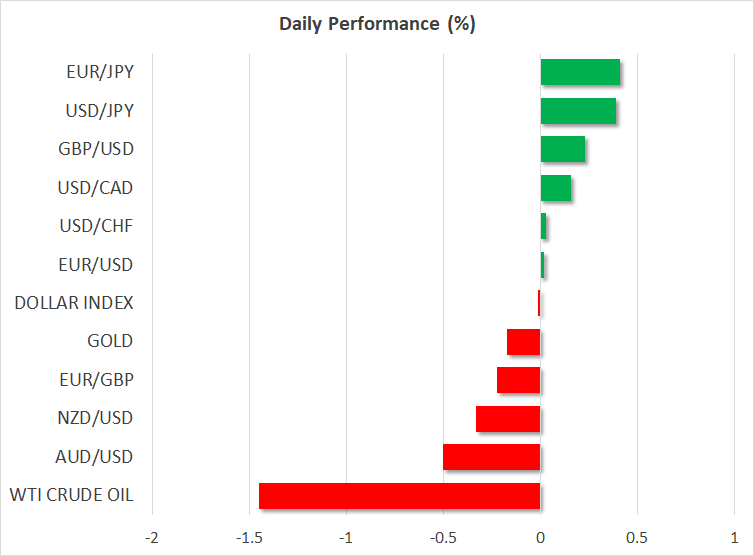

- Yen and euro extend losses, Wall Street also slips

Traders scale back Fed rate cut bets, US retail sales on tap

The US dollar rose sharply against all its major counterparts on Tuesday, extending its gains today, as Fed Governor Waller said that while inflation is within “striking distance” of their 2% objective, they should not rush into cutting interest rates until it is clear that low inflation is sustained.

Waller was the first Fed policymaker to officially talk about the possibility of rate reductions and thus, the fact that he is pushing against imminent rate reductions prompted investors to eventually pay attention. If he doesn’t want to cut in March, maybe no one else does. That’s why the probability for a March rate cut dropped to around 65% from slightly more than 70%, while the total number of basis points worth of rate cuts by December was reduced from around 160 to 150.

Still, this suggests that there is ample room for further adjustment and what could pour more cold water on investors’ aggressive rate cut bets may be today’s US retail sales for December. Following the hotter-than-expected CPI numbers for the month, improving consumer demand may translate, not only into healthier economic growth, but into concerns about stickier inflation in the months to come. This could thereby prompt investors to further lift their implied rate path, which could in turn help the dollar extend its recovery.

Later in the day, dollar traders will get the Beige Book, which provides details on the current economic conditions in each of the US’s 12 Federal districts, and they may closely listen to what New York Fed President John Williams has to say.

Sterling licks its wounds as CPI data beats estimates

The pound suffered against the dollar yesterday after data showed that UK wages slowed in the three months to November. That said, the currency entered a recovery mode today as the CPI figures for December came in hotter-than-expected, confirming the upside risks suggested by the services PMI for the month.

With headline inflation being double the BoE’s 2% objective and the core rate holding at 5.1%, the probability for a May rate cut dropped from 90% to 55% as the actual figures contrasted the forecasts by some institutions, including Deutsche Bank, that UK inflation will fall below 2% by April.

Expectations that the BoE will begin its own rate-reduction process after the Fed does may help pound/dollar recover some of the recently lost ground, but the pound will be put to another test this week as UK retail sales for December are coming out on Friday.

Yen falls the most, ECB officials send conflicting messages

The yen was among the main losers yesterday as reduced Fed rate cut bets and increasing expectations that the BoJ is in no rush to take interest rates out of negative territory are resulting in widening yield differentials between the US and Japan.

The euro traded on the back foot as Portuguese central bank chief Centeno and his French counterpart appeared open to the idea of rate reductions, with the latter policymaker noting that they may need to start cutting this year. Those remarks come after German central bank chief Nagel and ECB board member Schnabel said that it is too early to enter such a discussion. ECB President Lagarde also sounded skeptical today about the aggressive market pricing, but that did not stop her from paving the way for a possible cut in the summer, adding to the mixed signals. She is scheduled to speak later in the afternoon as well.

On Wall Street, all three of its main indices closed in the red, with the Dow Jones losing the most. The repricing of market expectations regarding the Fed’s future course of action appears to be the main drag for equities and improving retail sales later today may result in further losses. China’s lower than expected GDP earlier today may also be denting sentiment, evident by the retreat in stock futures.