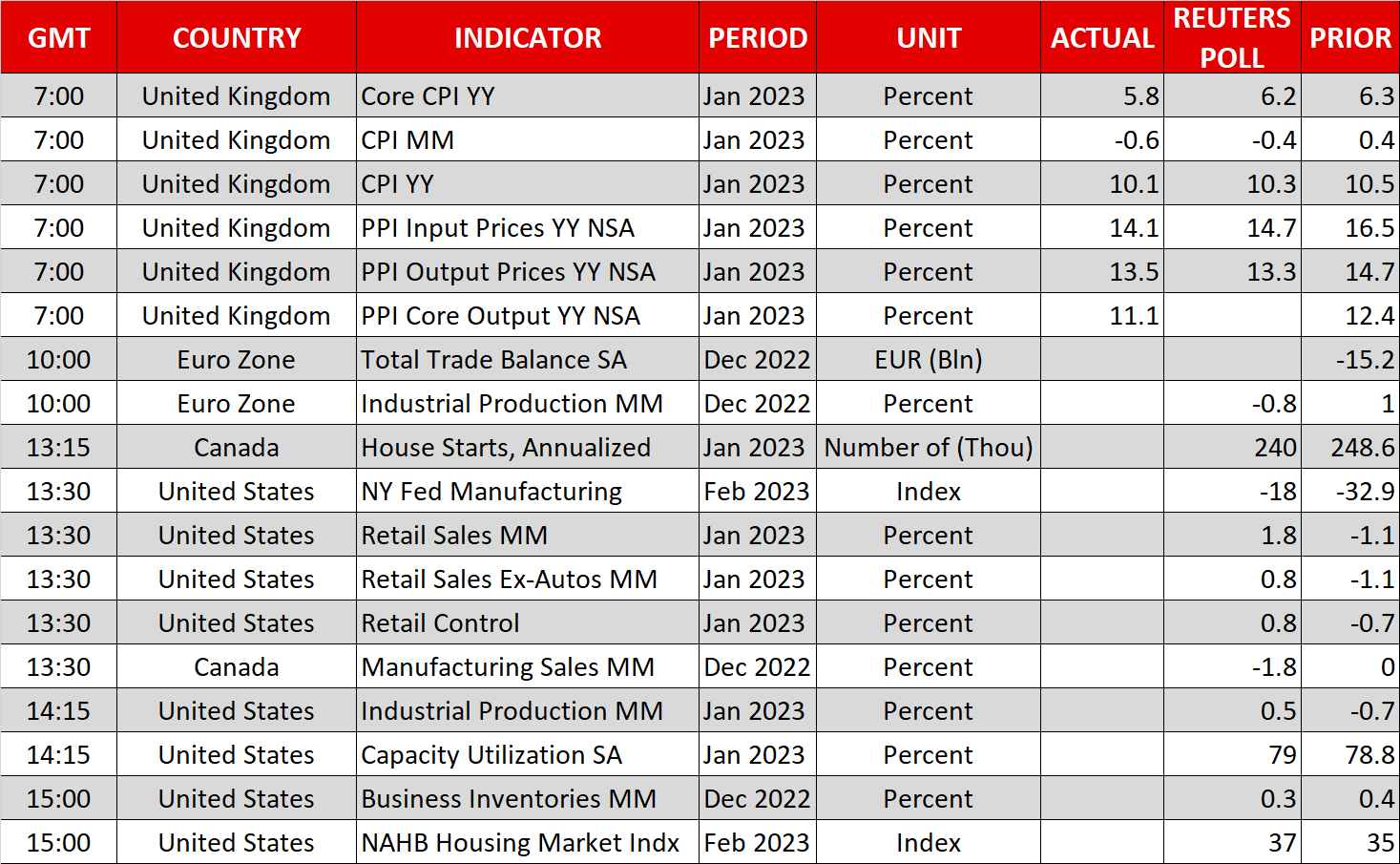

- Rental and food prices fuel US CPI

- Dollar gains as investors add to Fed hike bets

- Eurozone employment hits new record

- ECB President Lagarde steps onto the rostrum

Investors raise implied Fed rate path on accelerating monthly CPI

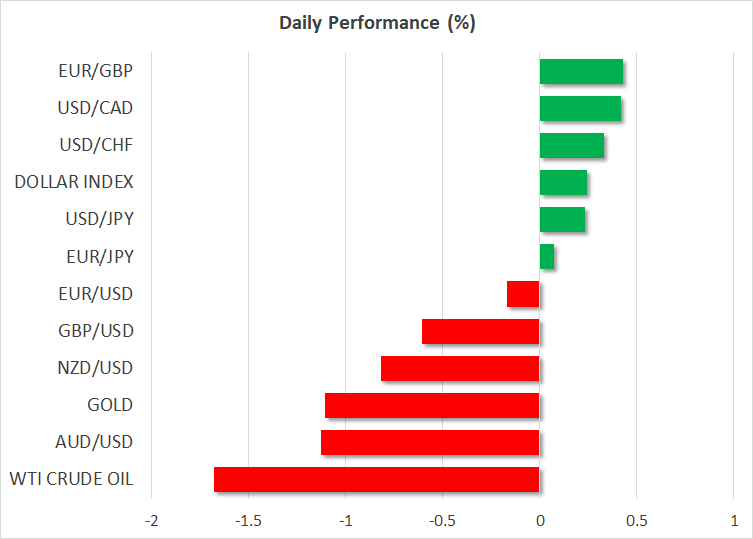

The dollar traded mixed against the other major currencies on Tuesday, but today it is outperforming all of them as yesterday’s US CPI data allowed investors to maintain the view that interest rates in the US may need to rise higher than anticipated.

The report revealed that both the headline and core year-over-year CPI rates further slowed in January, but by less than anticipated, while on a monthly basis, consumer prices accelerated to 0.5% from 0.1%, mostly due to higher rental and food costs. This suggests that inflation is stickier than previously thought, and following the astounding NFP gains and the rebound in the ISM non-manufacturing PMI, it adds further credence to the view of more rate hikes by the Fed.

Specifically, investors raised their terminal rate projections to 5.26%, while they expect interest rates to end the year at 5.06%. Yes, this is still 20bps worth of rate reductions, but should the Fed just match its own projection of 5.15%, no cuts may eventually be needed.

The initial reaction in the US dollar was a slide, perhaps on the lower y/y rates, but as soon as investors digested the full report, the currency recovered with the 10-year Treasury yields rising to levels last seen on January 3.

The latest shift in market expectations regarding the Fed’s course of action could allow the dollar to gain for a while longer, especially if US retail sales and industrial production for January come out strong today. However, it is still premature to call for a full-scale bullish reversal. The next Fed meeting is scheduled for March 21-22 and up until then, investors will have to absorb another round of employment and inflation data.

Record Eurozone employment supports more hikes by the ECB

What could also make a dollar comeback difficult may be a potentially strong euro. After all, euro/dollar is by far the largest component of the dollar index. Although the spotlight was on the US CPI data yesterday, just a few hours earlier, another report showed that Eurozone employment surged more than expected in the last three months of 2022 to a new record high, pointing to even more acceleration in underlying price pressures in the months to come and thereby more hikes by the ECB.

Combined with a surprisingly resilient economy, which may have avoided a recession according to the latest projections by the EU Commission, still-accelerating underlying inflation is allowing ECB officials to sound hawkish and keep delivering 50bps worth of rate increments. Following last week’s hawkish remarks by German policymakers Joachim Nagel and Isabel Schnabel, who signaled that more bold action is needed, ECB member Gabriel Makhlouf said yesterday that the Bank could raise rates above 3.5% and will probably not cut them this year.

Today is the turn of ECB President Lagarde to step onto the rostrum. At the press conference following the last policy meeting, she explicitly said that they intend to raise rates by another 50bps at the upcoming gathering and then evaluate the path of interest rates on a meeting-by-meeting basis based on the data. Should she corroborate the view that interest rates could be raised above 3.5%, investors could add more basis points to their hike expectations and thereby lift the euro. That said, for euro/dollar to resume its prevailing uptrend, a clear break back above 1.0800 may be needed.

Wall Street closes mixed after CPI numbers

Although expectations of a higher Fed rate path were clearly reflected in Treasury yields, the same cannot be said for Wall Street. Yes, the Dow Jones slid and the S&P 500 finished the session virtually unchanged, but strangely the more rate sensitive Nasdaq gained 0.57%. Perhaps the fact that the data is pointing to a better economic shape is allowing investors to add to their risk exposure even if higher rates hereafter mean lower present values for high-growth firms.

From a technical standpoint though, both the S&P 500 and the Nasdaq are struggling to break above their key resistance areas of 4,155 and 12,900 respectively, which means there is a group of investors who may be worried that interest rates could hurt firms’ profitability and valuations. With interest rates now expected to finish the year above 5%, it is hard to envision equity indices heading towards their record highs. On the other hand, with China reopening its economy, the Eurozone averting a recession, and latest US data coming in much better than expected, market participants seem reluctant to scale down their risk exposure. So, for now, the outlook for equity indices seems neutral.