- US job openings fall to the lowest since May 2021

- Wall Street slips as data revives recession fears

- Gold rallies above $2,000 as Fed pivot bets intensify

- New Zealand dollar rallies after RBNZ hikes by 50bps

Dollar extends losses as speculation about Fed rate cuts increases

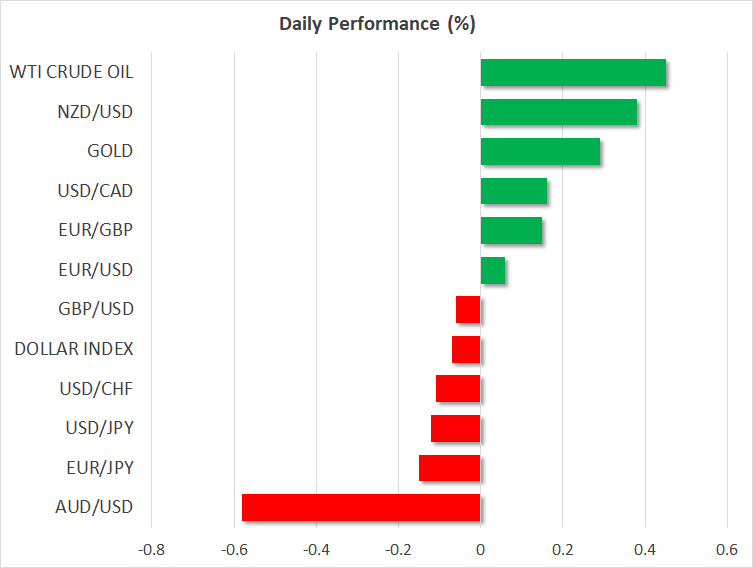

The dollar extended its losses against most of its major peers on Tuesday, with traders becoming split on whether the Fed will deliver another 25bps hike at its May meeting or not.

Following OPEC’s decision to cut oil production and the consequent surge in prices, market participants timidly started tilting the scale towards another quarter-point increase, but a cocktail of disappointing US data spread fresh doubts on what could be the wisest choice at the upcoming Fed gathering.

On Monday, the ISM manufacturing PMI disappointed on all fronts, while yesterday, the US Labor Department reported that job openings dropped below 10mn in February for the first time since May 2021. Evidence of a cooling economy just after the banking system was shaken up, revived fears that the Fed’s already-delivered hikes could result in a deep downturn. Those fears currently translate into evenly split chances for another hike or no action in May, as well as a series of cuts, with rates anticipated to end the year at 4.2%.

Nonetheless, ahead of the next FOMC meeting, investors will have to examine several more key data releases, with the ISM non-manufacturing PMI for March coming out today. Expectations are for a small decline, but with the index staying safely above the boom-or-bust zone of 50. That said, given that the service sector accounts for nearly 80% of US GDP, a negative surprise could very well spell more trouble for the US dollar.

Wall street slides, gold surges past $2,000

All three of Wall Street’s main indices slid yesterday, losing more than 0.5% each. Considering that equities tend to rise when Fed pivot bets intensify, this seems strange. Perhaps recession fears outweighed hopes of lower interest rates and pricier valuations, or it could be renewed concerns about the stability of the banking sector after the CEO of JPMorgan (NYSE:JPM) warned shareholders that the crisis is ongoing and that the impact will be felt for years.

The broader picture suggests that stocks remain resilient, despite yesterday’s pullback. The Nasdaq remains above the key zone of 12900, while the S&P 500 is very close to the important area of 4150. With investors lately ignoring anything that pushes against their view and paying more attention to reaffirmations, that zone could be easily breached on the next data point suggesting that the Fed may need to pivot this year. If this doesn’t happen by Friday, investors may get another opportunity next week if the CPI data shows that inflation slowed further.

The group of traders that took the most advantage of the dollar’s slide were gold traders, with the precious metal surging and clearing the psychological zone of $2,000 as soon as the job openings data was out. With the market stubbornly sticking to its view that rates in the US will be cut later this year, the path of least resistance for gold may be to the upside. The next areas to watch out for may be the peak of March 8, 2022, at $2,070 or the record high of around $2,075, hit on August 7, 2020.

RBNZ unexpectedly lifts rates by half point, kiwi jumps

Today, the dollar seems to be trying to stabilize against most of its peers, gaining more ground against the wounded aussie, but losing notably against the kiwi, which skyrocketed after the RBNZ confounded expectations of a quarter-point hike, and instead raised rates by 50bps. On top of that, although they noted that monetary policy is now contractionary, policymakers agreed that they must continue hiking rates to tame inflation.

All this widens even further the divergence in policy between the RBNZ and the RBA, which preferred to remain sidelined just a day earlier. With any risk-sentiment drivers being offset in the aussie/kiwi currency pair, the divergence in policy approaches of the RBNZ and the RBA suggests that the kiwi may continue outperforming its Australian counterpart for a while longer.