- Stronger-than-expected US CPI data revives rate hike bets

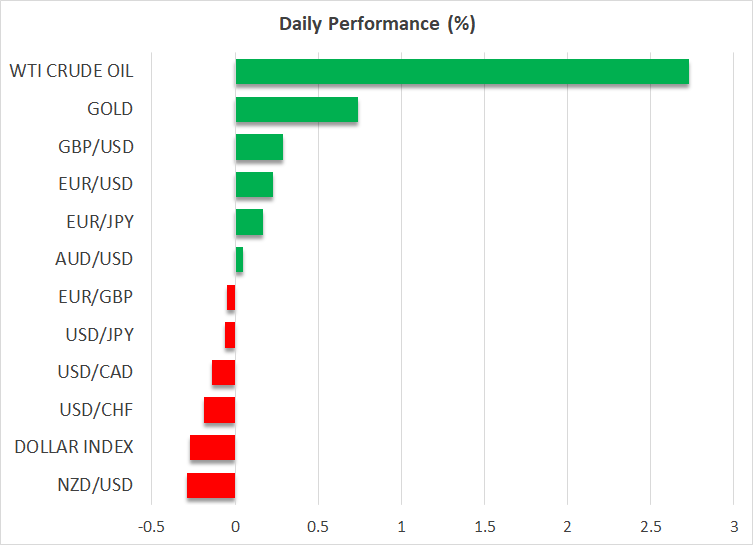

- Dollar re-energised, heads for weekly gains as yields jumps

- Stocks come under pressure, but selloff limited ahead of Q3 earnings

Dovish Fed bets dented by CPI surprise

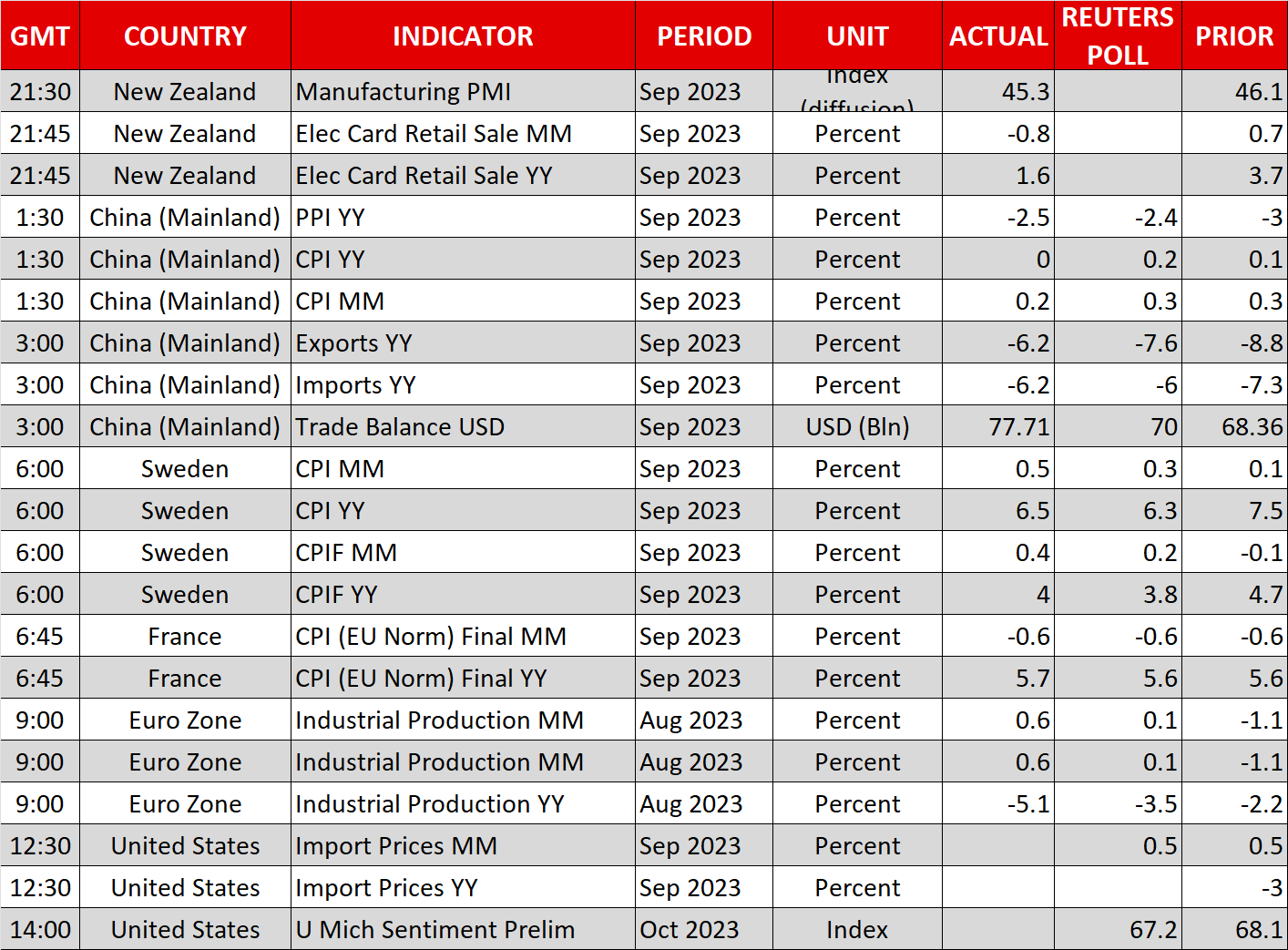

Markets whipsawed on Thursday after the US consumer price index rose more than expected in September, dashing hopes that the Fed is done hiking rates. The CPI measure of inflation edged up 0.4% month-on-month, beating forecasts of a 0.3% increase, while the annual figure was unchanged at 3.7% instead of easing to 3.6%.

After a string of not-so-hawkish remarks by Fed officials over the past week put a stop to the relentless rally in Treasury yields, the latest CPI report was a stark reminder to investors that the risks to inflation remain to the upside. Gasoline prices continued to exert upward pressure on headline inflation in September, though by a lesser extent than in August. But the biggest contribution to the monthly increase in CPI came from higher rental prices – something that could potentially make policymakers think twice before calling time on further tightening.

Market expectations for one more rate hike in the coming months rose to around 40% in the aftermath of the inflation data before easing slightly. The focus in recent weeks has shifted to the December and January meetings as the Fed is seen wanting to take more time to evaluate things given the mixed readings of late on the US economy. Thus, the next meeting on October 31-November 1 is no longer in the picture as far as a rate rise is concerned.

Yields off highs but dollar poised for positive week

Still, with rate hike odds having fallen to below 30% in the run up to yesterday’s numbers, the moderate repricing in futures markets was enough to spur significant moves in bond and FX markets. The yield on 10-year Treasury notes jumped more than 15 basis points to a high of 4.7282% on Thursday, fuelling gains of around 1% for the US dollar. Weak demand for 30-year Treasuries in yesterday’s auction exacerbated the bond selloff.

Yields are trading lower today and the dollar is softer too, but the damage has already been done to the recovery that was underway for battered currencies such as the euro and pound.

Fed speak is expected to be quieter today and the only major release on the agenda is the University of Michigan’s consumer sentiment survey, so the dollar has a strong chance of finishing the week with some decent gains.

China worries add to negative mood

One of the worst performers on Thursday was the Australian dollar, which tumbled by about 1.5% as risk-on sentiment took a blow from revived Fed overtightening fears. The aussie as well as its kiwi counterpart remain under pressure today following subdued data out of China.

Both producer and consumer prices in China increased by less than forecast in September, suggesting that the recent stimulus measures have done little to boost domestic demand. There was slightly better news from trade figures for the same period as the drop in exports wasn’t as large as had been anticipated.

Oil back on the front foot, gold resumes ascent

Oil futures shrugged off the sluggish data to rally more than 2% after Washington imposed sanctions on two shipping companies for breaching the $60 price cap on Russian oil. It is the first time that the US has sanctioned the owners of tankers carrying Russian oil, signalling a fresh move by the West to tighten the enforcement of the G7 price cap.

Today’s gains in oil prices more than offset the post-CPI drop as well as the selloff from the surge in weekly crude stockpiles in the US.

Gold, meanwhile, resumed its climb, with yesterday’s decline on the back of the rebound in bond yields proving to be just a blip. The precious metal approached $1,885/oz, lifting its weekly gains to 2.9% - its best performance since March. Ongoing tensions in the Middle East are likely keeping the safe-haven gold elevated as Israel is intensifying its assault on Gaza following last weekend’s attacks by Hamas.

Stocks eye bank earnings after yields setback

In equities, a negative close on Wall Street yesterday weighed on Asian and European markets on Friday. At this point, the recent correction in yields is looking increasingly just that – a correction – and it’s too soon to be able to say with any certainty that yields have peaked. Even if the Fed doesn’t raise rates again, the risk of inflation taking longer than expected to fall all the way down to 2% can’t be ignored. And when there are three 25-bps rate cuts priced in for 2024, a lot can still go wrong for equity markets.

For the time being, however, all eyes are on the Q3 earnings season, which is set to kick off today with the big banks. JP Morgan Chase (NYSE:JPM), Citigroup (NYSE:C) and Wells Fargo are all due to report their results later on Wall Street before the closing bell.