- Dollar stays pressured even as yields rise

- ISM PMIs and NFPs on this week’s agenda

- Wall Street feels the heat of rising yields and recession fears

- Oil finishes 2022 with gains

Investors push yields higher, but not the dollar

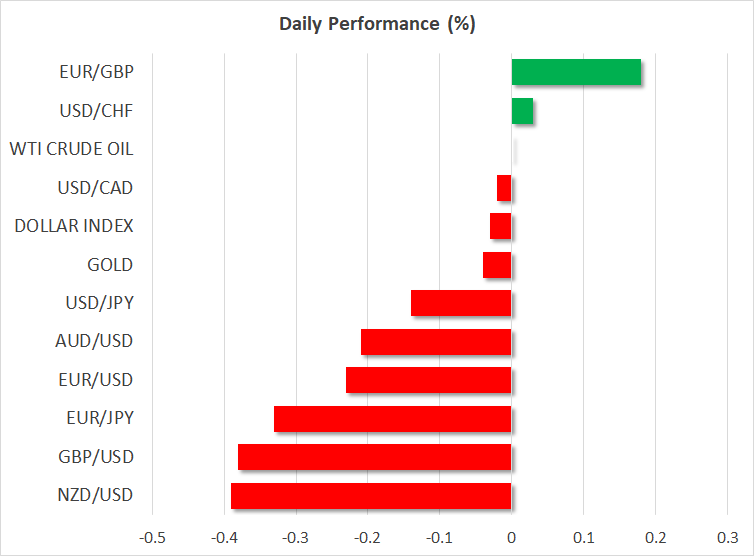

The US dollar ended the last trading day of 2022 on the back foot against most of the other major currencies, despite US Treasury yields rising further. It rebounded somewhat today.

The 10-year yield has been in a recovery mode since mid-December, closing the trading year with its biggest annual increase in decades, but the greenback has failed to follow that last rebound, although it finished the year with a roughly 8% gain, its biggest since 2015.

The US currency came under selling pressure during the last quarter of 2022, as easing inflation in the US raised speculation of a Fed pivot sooner rather than later, although policymakers have been adamant that when interest rates reach their terminal level, they are likely to stay there for some time.

Market participants have been raising their implied terminal rate recently, taking it to around 5% on Friday, but they are still pricing in more than 50bps worth of rate cuts by the end of the year. They probably believe that the still-tight labor market could warrant slightly bigger hikes in the short run, but also that, with other data deteriorating, officials may need to start scaling down borrowing costs later this year to avoid a deeper recession.

This week, both the ISM manufacturing and non-manufacturing indices for December are expected to have declined, with the former slipping further below the boom-or-bust zone of 50. This would confirm recession concerns and rate-cut bets, while signs of weakness in the labor market from Friday’s employment report could prompt investors to take back down the level of where they expect interest rates to peak.

Such developments could keep the dollar pressured, pushing it closer to the key zone of 1.0800 per euro. That zone may be the last line of defense for euro/dollar bears as it acted as both support and resistance in previous years. Its break could intensify trend reversal talks.

Higher yields and recession fears weigh on Wall Street

The rising yields put added pressure on equities, with the tech-heavy Nasdaq getting closer to its November lows last week. Wall Street will stay closed today for the New Year Holiday, but expectations of higher interest rates during the first half of the year, together with increasing recession fears, appear to be a negative cocktail for the short run.

Yes, news about the reopening of the Chinese economy was initially cheered by investors, but with COVID infections soaring in many districts, the optimism faded fast. Investors are now worried that, let alone the risk of reversing relaxations, the Chinese economy may take much longer to recover, while they are also evaluating the risk of new variants spreading to the rest of the world.

Even if the world’s second largest economy were to recover faster, the restoration of demand for energy could add support to oil prices, which may very well lead to a rebound in inflation around the globe and raise fears of even tighter monetary policy by central banks.

Ergo, the risks surrounding the stock market remain tilted to the downside for now, even as the US dollar weakens. It seems that the inverse correlation has broken down, at least for now. Due to recession fears, the currency could attract some safe-haven flows periodically, but as long as rate-cut bets are firmly on the table, investors may prefer to seek shelter in other safe havens, like the yen and gold.

Oil ends year in gains, outlook remains blurry

Oil prices finished 2022 in the green, despite trending lower during the second half of the year due to weaker demand from China and concerns of a global economic contraction.

The black liquid entered a recovery mode in December on hopes of easing restrictions in China, but also due to Russia banning the supply of oil to nations that abide by the cap agreed by the G7 nations.

However, the discussion of a major uptrend still appears premature. The surging COVID infections in China could result in economic complications and thereby delay the return of demand to normal levels, while a deteriorating global economy could result in shrinking fuel consumption.

An uptrend is off the cards from a technical standpoint as well. Even after the latest recovery, WTI remains below the downtrend line drawn from the high of June 14, while it has yet to confirm a higher high on the daily chart. Therefore, the outlook may be best described as neutral for now.