The U.S. Dollar weakened against most of the majors and slumped to a one-year low against safe havens like the Swiss Franc. The markets grew concerned as Gross Domestic Product was revised to a yearly 2.4 percent after the Commerce Department posted the preliminary forecast of 3.2 percent for the last three months of 2013. Federal Reserve Chairwoman Janet Yellen indicated that the economy has softened, but that it was not completely clear which factors caused the slowdown. Mrs. Yellen added that policy makers are waiting to ascertain whether the winter season is the main culprit for the economy’s slump. Risk appetite declined in the markets as tensions between Russia and the Ukraine worsened, and as the U.S. warned Russia against taking military actions. Appetite was also impacted by the likelihood that the Chinese Central Bank intervened in the market causing the Yuan’s major drop in anticipation of government reforms slated to be implemented in the near future. Gold Futures dipped on Friday although they still sustained the biggest hike since July. The weaker than predicted economic releases out of the U.S. cast doubts over the likelihood of another cut in monthly bond assets. Contracts for April delivery concluded the week at $1,321.6 0 a troy ounce on the Comex Division of the New York Mercantile Exchange and are predicted to settle at $1,307.10. Other reports revealed that production in Australia, the world’s second biggest gold producer, reached the highest level in ten years as miners boosted the output of high grade ores. Economists anticipate that bullion may plunge to $1,011.00 an ounce by December should the Federal Reserve continue to taper stimulus.

The Euro climbed to the highest price in ten months as recent metrics on Inflation raised speculation that policy makers may not make any changes to policy at this time. The shared currency experienced its biggest advance since April as higher Inflation numbers set investors at ease. However, economists remain worried that deflation could be the next major problem to weigh on the regional economy given low domestic demand. The E.U.’s Gross Domestic Product came in higher than predicted signaling that the recovery is gaining momentum in practically every economy of the region. Exports continued to help the E.U.’s progress while consumption is said to remain off. The British Pound extended gains against the greenback as recent announcements revealed that a higher amount of investing in the business sector has led the U.K. to post a bigger economic expansion. However, the Bank of England’s officials have intimated that the surge in the currency’s value could become a problem for the economy.

In Japan, Inflation appears to be reaching the Bank of Japan’s target goal. According to releases, the Consumer Price Index posted at 1.3 percent on a year-over-year basis in January, and analysts forecast that an upcoming hike in sales tax may help boost the inflation level to the bank’s 2 percent target by the middle of 2014. The Bank of Japan has indicated that it will adhere to the current monetary easing plan, but there’s a possibility that policy makers may increase easing if the tax increases slow the economy down.

Lastly, in the South Pacific, New Zealand’s Dollar jumped to a six-week high against its U.S. peer on metrics confirming that trade levels with China rose; and it remained to the upside on the likelihood the Federal Reserve may not move ahead with further bond purchasing cuts. The Kiwi rallied on Friday following news indicating that the Business Confidence Index climbed to close to two-decade highs in February, and as other announcements revealed that the country’s Trade Surplus contracted less than predicted. Australia’s Dollar slipped to one-month lows against the greenback as the markets remain wary about the progress of China’s economy. The drop of the Yuan along with economic news showing that Chinese Manufacturing PMI fell to eight-month lows prompted a decline in risk appetite.

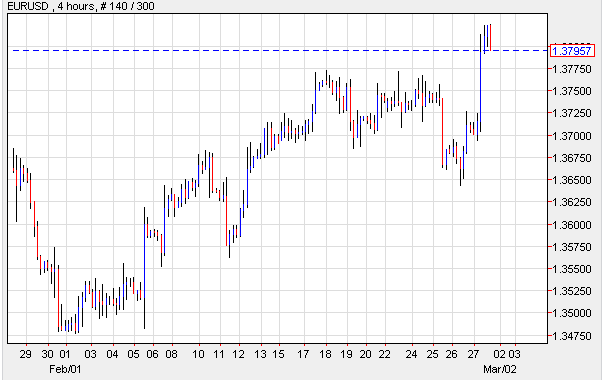

EUR/USD- Deflation May Not Make Headlines

The EUR/USD surged to more than a two-month high after the U.S Commerce Department indicated that the fourth quarter’s Gross Domestic Product only posted at 2.4 percent rather than the previously shown 3.2 percent. The pair was fueled by news that the yearly percentage of Consumer Inflation came in at 0.8 for February, a tad higher than the anticipated 0.7 percent. While the number was below the European Central Bank’s target 2 percent, it appeared to ease policy makers who thought they would have to tighten policy in the face of possible deflation. All eyes will be on the bank this Thursday, when it meets to discuss the future of the E.U.’s monetary policy. The Euro region will also be publishing key economic fundamentals out of Spain and Italy.

EUR/USD" title="EUR/USD" align="bottom" border="0" height="242" width="474">

EUR/USD" title="EUR/USD" align="bottom" border="0" height="242" width="474">

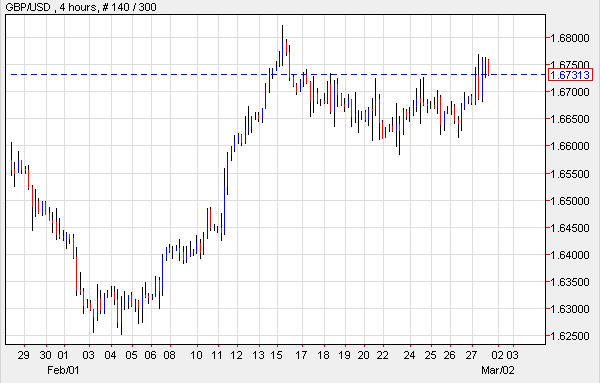

GBP/USD- Investments Up

The GBP/USD advanced following economic reports out of the U.S. denoting a drop in growth for the fourth quarter of 2013, and as releases out of the U.K. revealed that a hike in business investments led the way for the British economy to sustain a surge in growth. Analysts have suggested that the U.K.’s economy has expanded due to the fact that the European economy has not expanded as much. However, Ian McCafferty, one of the Bank of England’s policy makers, suggested that the hike in the Sterling could become a problem for exporters, though it’s not a problem at present. British Gross Domestic Product rose 0.7 percent in the months of October to December 2013 and from the previous year, the economy showed the most growth in close to six years.

GBP/USD" title="GBP/USD" align="bottom" border="0" height="242" width="474">

GBP/USD" title="GBP/USD" align="bottom" border="0" height="242" width="474">

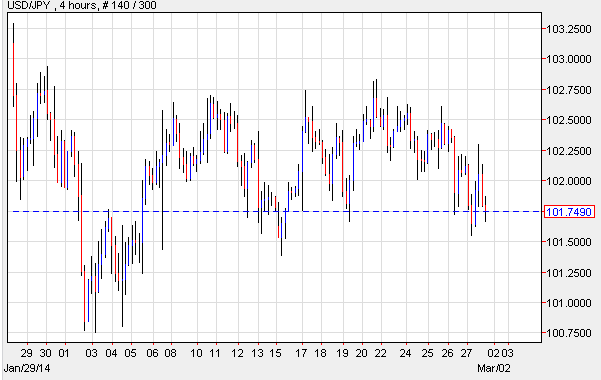

USD/JPY- Japanese Gather Information

The USD/JPY weakened on mixed macroeconomic fundamentals out of the U.S. In Japan, the government is preparing to collect data on how the financial institutions set their currency exchange rates in order to conduct commercial transactions. According to sources, this was prompted by a recent probe into currency exchange manipulation. The Financial Services Agency will present the data to the central bank who in turn will provide the information to the Financial Stability Board who regulates currency fixing. On the domestic front, Inflation seems to be inching closer to the central bank’s target rate, and policy makers have pledged to leave monetary easing unchanged unless the increase in sales tax of April causes the economy to lose momentum. Demand for safe harbors benefitted the Yen, causing a further decline in the USD/JPY. The increase in risk aversion came about on reports indicating that the situation between Russia and the Ukraine worsened, especially after news that Russian military stormed airports in the Crimea region.

USD/JPY" title="USD/JPY" align="bottom" border="0" height="242" width="474">

USD/JPY" title="USD/JPY" align="bottom" border="0" height="242" width="474">

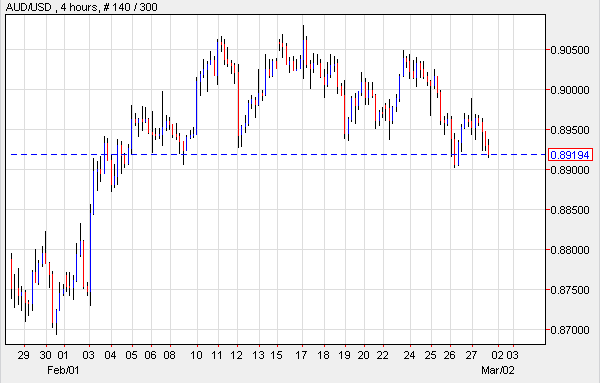

AUD/USD- Aussie Posts Busy Month

The AUD/USD traded actively in the month of February, but slumped to one-month lows on Friday. The pair’s fall occurred as investors worry about the future of China’s economy and the possible intervention which may have been the reason for the Yuan’s plunge. Data issued last week showed that China’s Manufacturing PMI declined and the Trade Balance contracted. But according to analysts, it’s really the drop of the Yuan what has shaped the risk environment in the markets and the shifts in appetite. The Yuan was sustained dramatic drops against the greenback. Meanwhile, Australia’s miners have raised gold production. And the central bank has stated that inflationary pressures have risen. In the days ahead, the South Pacific nation will issue reports on Company Profits, while China releases metrics on activities in the Services sectors.

AUD/USD" title="AUD/USD" align="bottom" border="0" height="242" width="474">

AUD/USD" title="AUD/USD" align="bottom" border="0" height="242" width="474">

Today’s Outlook

Today’s economic calendar shows that Switzerland will report on the SVME PMI. The Euro region will issue Manufacturing PMI. The U.K. will also publish Manufacturing PMI along with Mortgage Approvals, M4 Money Supply and Net Lending to Individuals. The U.S. will announce Core PCE Price Index, Personal Spending, ISM Manufacturing Employment, and ISM Manufacturing PMI. Australia will provide information on the Current Account, Building Approvals, the Interest Rate Decision and the RBA’s Rate Statement.