Under Armour, Inc. (NYSE:UAA) is scheduled to report third-quarter 2017 results on Oct 31, before the opening bell.

The question lingering in investors’ minds is whether this marketer and distributor of apparel, footwear and accessories will be able to deliver a positive earnings surprise in the to-be-reported quarter. In the trailing four quarters, the company’s earnings have outpaced the Zacks Consensus Estimate with an average of 33.3%. Let’s see how things are shaping up for this announcement.

What to Expect?

The Zacks Consensus Estimate for the quarter is pegged at 19 cents down from 29 cents reported in the year-ago period. Notably, the estimates have witnessed downward revisions in the last 30 days. Analysts polled by Zacks expect revenues of $1,490 million for the said quarter, up about 1.2% from the year-ago quarter.

Factors at Play

We believe the third-quarter results are likely to be impacted by moderation in North American business. Further, Under Armour has been grappling with higher interest expense as a result of increased debt level. In second-quarter 2017, the company’s interest expenses increased to nearly $8 million in comparison with $6 million in the prior-year quarter. Further, it anticipates interest expenses to rise to roughly $40 million in 2017 from $26.4 million in 2016.

Gross margin, which has been witnessing a sharp decline over the past few quarters, is anticipated to decline by a minimum of 120 basis points in comparison with 46.4% reported in 2016. This can be attributed to foreign currency headwinds, restructuring plan and its efforts toward managing inventory. The decline is likely to persist in the third quarter too.

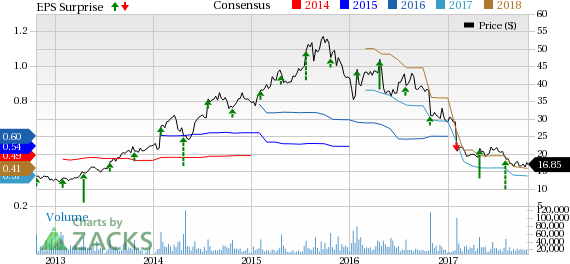

These factors have been well reflected in the company’s stock price performance. Evidently, Under Armour’s shares have plunged over 42% year to date against the industry’s gain of 2.4%.

However, Under Armour’s sustained focus on brand development, expansion of direct-to-consumer and technology-based fitness businesses look encouraging.

Under Armour, Inc. Price, Consensus and EPS Surprise

Under Armour, Inc. Price, Consensus and EPS Surprise | Under Armour, Inc. Quote

What Does the Zacks Model Unveil?

Our proven model does not conclusively show earnings beat for Under Armour this quarter. This is because a stock needs to have both a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) and a positive Earnings ESP for this to happen. You may uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Under Armour has an Earnings ESP of +2.13%. However, the company carries a Zacks Rank #4 (Sell). We caution against stocks with a Zacks Rank #4 or 5 (Sell-rated stocks) going into the earnings announcement, especially when the company is seeing negative estimate revisions.

Stocks with Favorable Combination

Here are some companies you may want to consider as our model shows that these have the right combination of elements to post an earnings beat:

Conn's, Inc. (NASDAQ:CONN) has an Earnings ESP of +50.00% and a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

Ralph Lauren Corporation (NYSE:RL) has an Earnings ESP of +2.63% and a Zacks Rank #2.

Big Lots, Inc. (NYSE:BIG) has an Earnings ESP of + 15.39% and a Zacks Rank #2.

Today's Stocks from Zacks' Hottest Strategies

It's hard to believe, even for us at Zacks. But while the market gained +18.8% from 2016 - Q1 2017, our top stock-picking screens have returned +157.0%, +128.0%, +97.8%, +94.7%, and +90.2% respectively.

And this outperformance has not just been a recent phenomenon. Over the years it has been remarkably consistent. From 2000 - Q1 2017, the composite yearly average gain for these strategies has beaten the market more than 11X over. Maybe even more remarkable is the fact that we're willing to share their latest stocks with you without cost or obligation.

Conn's, Inc. (CONN): Free Stock Analysis Report

Big Lots, Inc. (BIG): Free Stock Analysis Report

Ralph Lauren Corporation (RL): Free Stock Analysis Report

Under Armour, Inc. (UAA): Free Stock Analysis Report

Original post