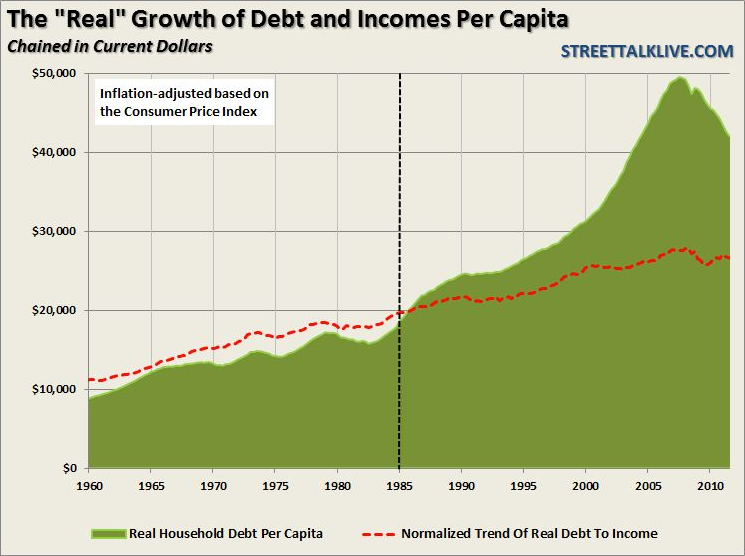

The release of the Federal Reserve's report on consumer credit was very telling. One of the continued themes that the economy was on its way to a real recovery was that the consumer was well into deleveraging the household balance sheet. This is important because one of the drags on economic growth has been a low savings rate due to high debt service levels. The chart below shows "real," inflation adjusted, consumer debt relative to incomes. The red dashed line is the normalized growth trend of debt to incomes as a point of reference for the current levels of debt to incomes.

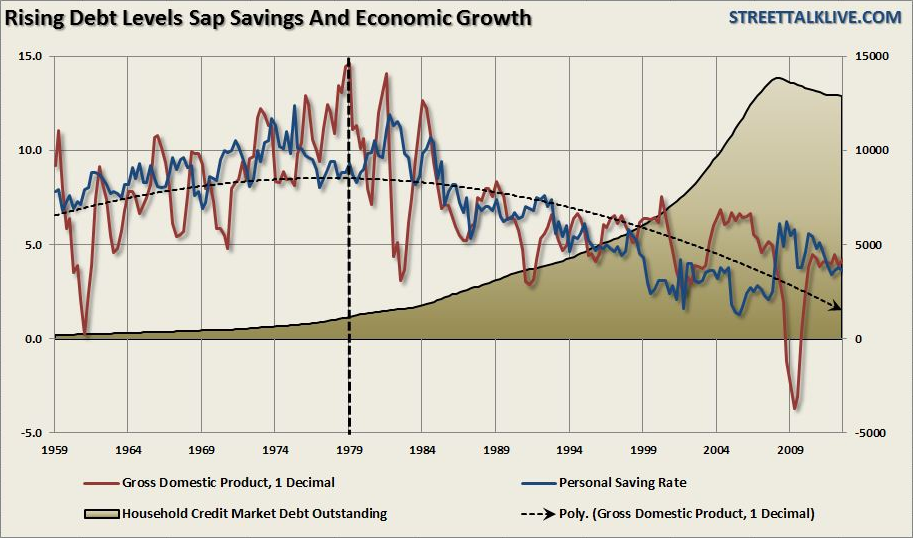

What is important to note, as shown more clearly in the next chart, is that economic growth expanded when debt was lower than the normalized trend. This led to higher savings rate which in turn fostered stronger economic growth. However, post 1980, as the trend of economic growth began to weaken, and interest rates fell, consumers began to leverage up with debt. The increase in debt service reduced savings rates from over 10% to less than 4% today.

More importantly the consumer has been turning to debt to offset falling incomes.The fight to maintain a standard of living that runs well above what can actually be afforded -- has come at an economic cost. The lower rates of productive investment, which is derived from savings, has led to a weaker trend of economic growth. Weaker economic growth has subsequently led to weaker growth rates of disposable income.

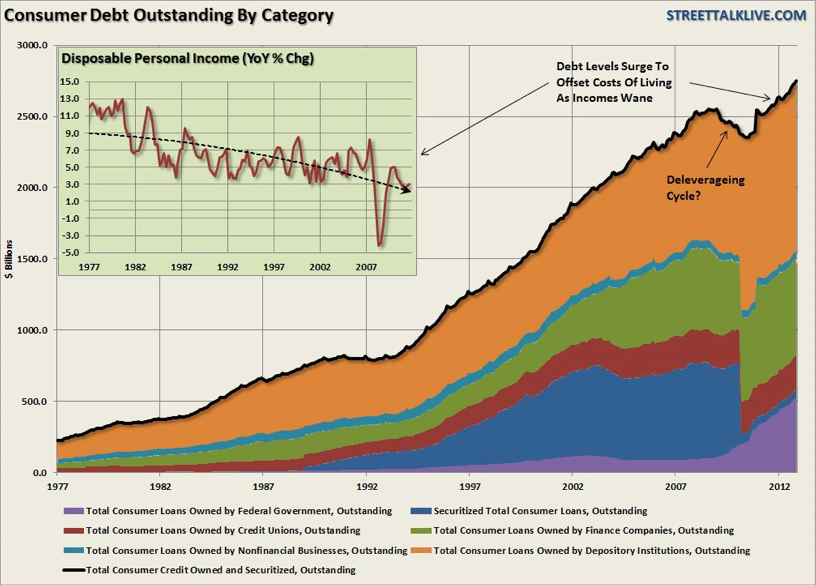

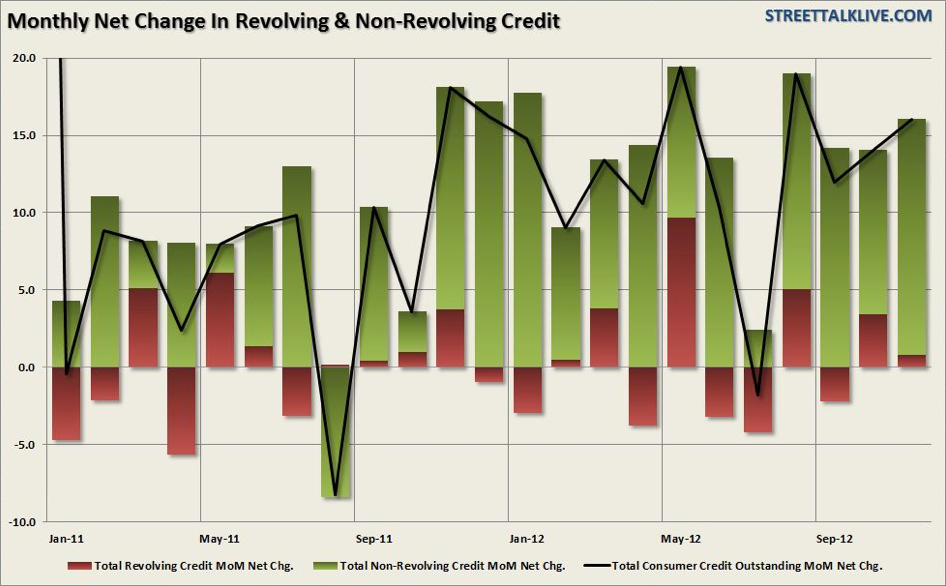

However, as the cost of living has continued to rise, due to both inflation and a an artificial wealth effect created by a continued fall in interest rates and stock market and real estate related asset bubbles, the affordability gap was filled with credit. This is a problem that continues to exist. The next chart shows consumer credit (another word for debt).

What is clearly evident is that the only deleveraging that has occurred, so far, has been primarily due to default, bankruptcy and the foreclosure process on mortgage debt. That is a trend, thanks to repeated bailouts of the banking sector to cover up the real issues, which is slowly fading.

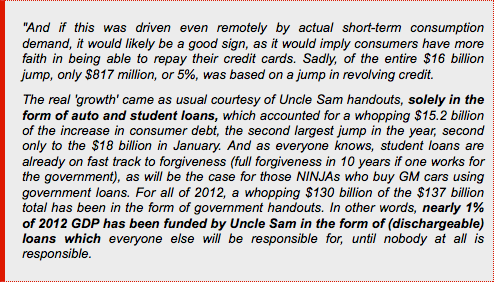

Another very disturbing trend in the data was discussed by Tyler Durden at Zero Hedge:

It has been quite apparent for some time that student loan debt, along with applications for food stamps and disability payments, was being used to bridge the gap between incomes and the standard of living for millions of Americans.

With the average American still living well beyond their means the reality is that economic growth will remain mired at lower levels as savings continue to diverted from productive investment into debt service. Furthermore, with the Federal Reserve and the Administration actively engaged in creating an artificial housing recovery, and wealth effect from increasing asset prices, it is likely that another bubble is being created. This has never ended well before. The concern is that without a reversion of debt to more sustainable levels the attainment of stronger, and more importantly, self-sustaining economic growth could be far more elusive than currently imagined.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Consumer Credit: What Deleveraging?

Published 01/09/2013, 05:16 PM

Updated 02/15/2024, 03:10 AM

Consumer Credit: What Deleveraging?

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2025 - Fusion Media Limited. All Rights Reserved.