Cleveland-Cliffs Inc. (NYSE:) is scheduled to release its fourth-quarter 2017 results before the opening bell on Jan 25.

Last quarter, Cleveland-Cliffs reported net income of $53 million or 18 cents per share against net loss of $28 million or 12 cents incurred in the prior-year quarter. Adjusted earnings of 36 cents per share for the quarter surpassed the Zacks Consensus Estimate of 30 cents.

Sales for the quarter were $698.4 million, up 26.2% year over year. It also outpaced the Zacks Consensus Estimate of $668 million.

Cleveland-Cliffs surpassed the Zacks Consensus Estimate in three of the trailing four quarters while missing in one, with an average negative surprise of 10.1%.

Shares of the company have moved up around 21.6% in the last three months, outperforming the

industry’s 16.6% growth.

Let’s see how things are shaping up for this announcement.

Factors at Play

For 2017, Cleveland-Cliffs reduced its sales volume expectation for its U.S. unit by 500,000 tons to 18.5 million long tons due to considerable reduction in pellet nomination by a large customer, which was partly offset by higher export sales. Further, the company expects iron-ore cash cost of goods sold and operating expenses in the range of $55-$60 per long ton, which remain unchanged from previous expectations.

The company also projects sales production volume of 10.5 million metric tons for the Asia Pacific Iron Ore operation, which represents a decrease from the previous forecast owing to operational decisions. Additionally, the company increased expectations for iron-ore cash cost of goods sold and operating expenses in the range of $36-$41 per metric ton owing to unfavorable exchange rate movements and reduced production volumes.

Moreover, the company's interest expense for 2017 has been reduced by $5 million to roughly $130 million as a result of the refinancing transaction in July, of which $20 million is expected to be non-cash.

The company also maintained its full-year selling, general and administrative (SG&A) cost expectation of $110 million factoring in higher incentive compensation accruals and spending associated with the development of the hot briquetted iron (HBI) production plant.

The Zacks Consensus Estimate for consolidated revenues for the fourth quarter is $644.5 million, reflecting a year over year decrease of around 14.5%.

For the fourth quarter, revenues from product sales and services at Cleveland-Cliffs’ U.S. Iron Ore segment is projected to witness a 24.5% decrease from the preceding quarter as the Zacks Consensus Estimate for the fourth quarter is pegged at $451 million.

Moreover, the Zacks Consensus Estimate for revenues from product sales and services at the Asia Pacific Iron Ore segment is expected to be $142 million for the fourth quarter, reflecting an estimated 39.2% increase.

Meanwhile, Cleveland-Cliffs remains focused on de-leveraging its balance sheet. Its net debt was roughly $1.4 billion at the end of the third quarter, down from around $2 billion at the end of the year-ago quarter. The company, in October, said that it expects to cut net debt to below $1 billion by end-2017. This would lead to a reduction in its annualized interest expense.

However, Cleveland-Cliffs is exposed to pricing pressure. It faces headwind from lower expected iron ore pricing, which coupled with anticipated volume pressure, may weigh on its fourth-quarter results.

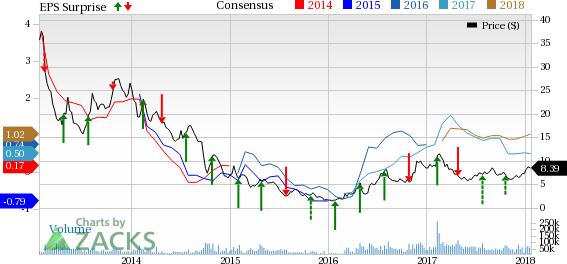

Cliffs Natural Resources Inc. Price, Consensus and EPS Surprise

Cliffs Natural Resources Inc. Price, Consensus and EPS Surprise | Cliffs Natural Resources Inc. Quote

Earnings Whisper

Zacks ESP: Cleveland-Cliffs has an Earnings ESP of +2.73%. This is because the Most Accurate estimate is 16 cents while the Zacks Consensus Estimate is pegged at 15 cents. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: Cleveland-Cliffs carries a Zacks Rank #3 (Hold), which when combined with a positive ESP, makes us reasonably confident of an earnings beat. Note that stocks with — a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 — have significantly higher chance of beating earnings estimates.

Conversely, Sell-rated stocks (Zacks Rank #4 or 5) should never be considered going into an earnings announcement.

Stocks With Favorable Combination

Here are some companies in the basic materials space, which according to our model also have the right combination of elements to post earnings beat this quarter:

LyondellBasell Industries NV (NYSE:) has an Earnings ESP of +2.00% and a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

Agnico Eagle Mines Limited (NYSE:) has an Earnings ESP of +5.00% and a Zacks Rank #2.

Kinross Gold Corporation (NYSE:) has an Earnings ESP of +2.27% and carries a Zacks Rank #3.

Wall Street’s Next Amazon (NASDAQ:)

Zacks EVP Kevin Matras believes this familiar stock has only just begun its climb to become one of the greatest investments of all time. It’s a once-in-a-generation opportunity to invest in pure genius.

Click for details >>