- China’s offshore yuan slides to new lows amid capital exodus

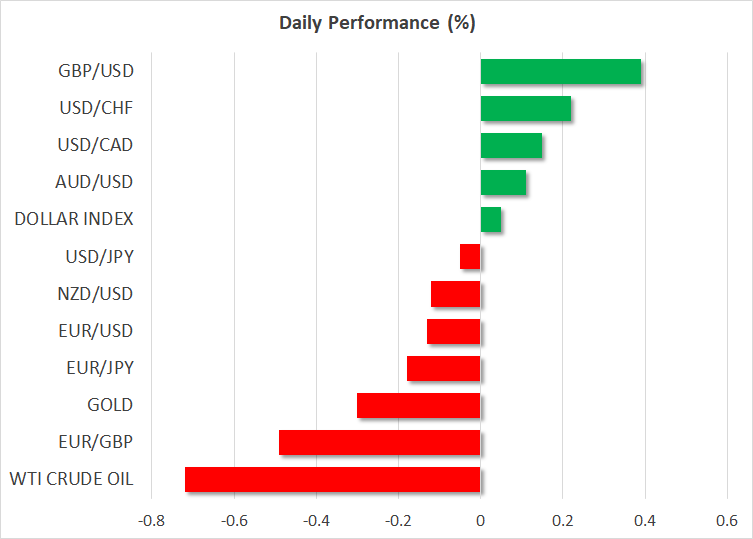

- Dollar retreats after soft business surveys, antipodeans struggle

- Stock markets run into resistance ahead of big tech earnings

Escaping China

Investor concerns around China’s economic trajectory reached a crescendo this week, hammering the offshore yuan down to new record lows as capital outflows escalated. With President Xi Jinping tightening his grip on power, the fear is that economic growth will become a second-tier priority, and policies such as draconian covid lockdowns will persist.

At the core of China’s problems lies a property sector bubble that has burst. Insufficient stimulus to counteract the fallout and the economy-suffocating lockdowns allowed this crisis to snowball, raising the risk it infects the nation’s leveraged banking system that is highly exposed to property loans, with rising interest rates globally amplifying the funding stress.

Without any signs the landscape is improving, it is no surprise that Chinese equity markets are under heavy pressure and the offshore yuan is brushing record lows. The twist is that unlike Japan and Europe, a weaker currency is beneficial for China since the nation still enjoys a massive trade surplus and muted price pressures, allowing FX depreciation to boost growth and inflation.

All told, China is perhaps the greatest risk for the global economy. While the United States and to a lesser extent Europe are likely to face ‘vanilla’ recessions caused by surging interest rates and energy shortages, China might encounter something much worse as the property meltdown can ignite systemic risks.

Antipodeans struggle, dollar cools off

Currencies of economies that depend on Chinese demand to absorb their commodity exports struggled yesterday, with the prime examples being the Australian and New Zealand dollars. In the UK, Sunak won the race to become prime minister, yet the pound could not sustain its gains, as market pricing around Bank of England rate hikes was unwound amid hopes of fiscal restraint.

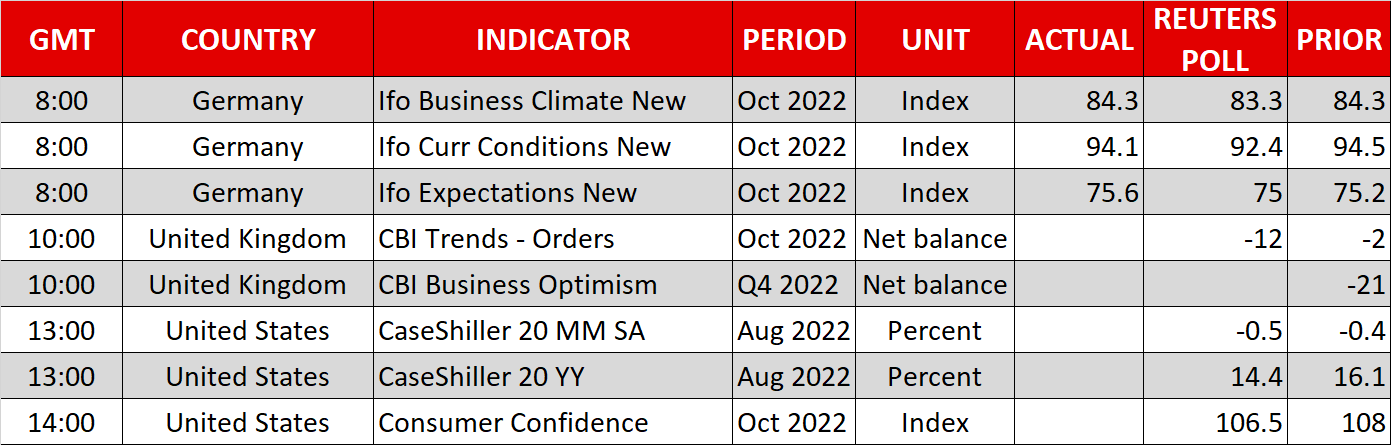

In the US, a batch of soft PMIs dealt a minor blow to the dollar. The surveys didn’t mince words, warning the economic downturn “gathered significant momentum” as the rising cost of living and tighter financial conditions crushed demand. With the Fed hellbent on rolling out more rate hikes while business surveys are already at contractionary levels and sinking, there’s a growing sense the speed of this tightening cycle will be a terrible policy error in hindsight.

As for the dollar, while the picture remains positive, we might be entering the ‘final act’ of this ferocious rally. The Fed has opened the door for a slowdown in December, the market is flush with long-dollar bets, and the outlook for the euro has turned incrementally brighter after the massive decline in energy prices. Hence, the fundamentals still favor a stronger dollar, but the runway for further gains seems narrow.

Earning season fires up

Bad news for the US economy was once again beneficial for Wall Street, with the S&P 500 rising more than 1% to encounter resistance near 3,800 after the disappointing batch of business surveys fueled hopes of a more cautious Fed.

The earnings season will kick into top gear today with heavyweights such Microsoft (NASDAQ:MSFT), Google (NASDAQ:GOOGL), Visa (NYSE:V), and Coca Cola releasing their quarterly results. The problem with this reporting season is that no matter how good of a quarter a company had, it cannot say confidently it will sustain that performance given the shifting macroeconomic outlook. Hence, any earnings-driven rallies are unlikely to be sustained for long.

Earnings estimates for next year have not kept pace with the weakening economic data pulse and are still far too rosy. Coupled with soaring bond yields that exert a gravitational force on equity markets by deflating valuation multiples, it’s still too early to be optimistic.