China pledges more stimulus, lifting oil prices and local stocks

Euro licks wounds after disappointing PMIs, antipodeans shine

Wall Street advances ahead of Microsoft (NASDAQ:MSFT) and Google earnings

Stimulus optimism

Chinese authorities vowed to roll out more stimulus measures on Monday, spreading cheer in global markets. The world’s second-largest economy has been plagued by a deepening downturn in the manufacturing and real estate sectors, which combined have put the brakes on economic growth, forcing the Politburo into action despite lingering concerns about elevated debt levels.

While the latest reports did not contain any details on specific measures, the blueprint is that the government will seek to boost domestic consumption by focusing on demand for cars, electronics, and household products. Most importantly, China pledged to “adjust” its property market policies, sending a strong signal that the rules to restrain speculation in real estate are about to be relaxed.

Traders responded by loading the truck with China-sensitive assets. Oil prices hit their highest levels in three months on hopes of increased demand from the world’s largest consumer, the Chinese yuan strengthened, and Asian markets rallied with stocks in Hong Kong spearheading the advance.

Now the question is whether all these stimulus measures will contain enough firepower to truly stabilise the Chinese economy and keep investors in high spirits. Beijing has been reluctant to roll out the heavy guns so far, worried of the repercussions on debt, so traders will need to see the details and scope of these policies before getting too excited.

Euro nurses losses, commodity FX shines, gold indecisive

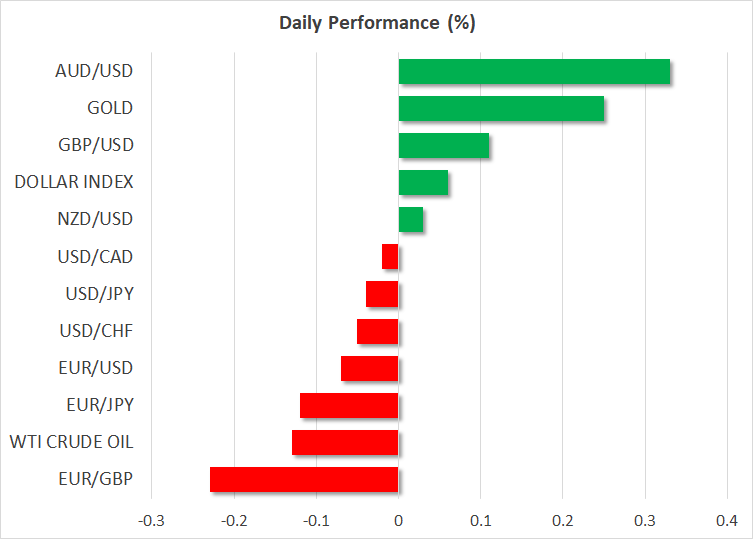

In the FX sphere, the currencies of nations with close trade links to China enjoyed a fresh burst of demand. Specifically, the Australian and New Zealand dollars are outperforming on Tuesday amid bets that any Chinese stimulus will spill over and bolster the commodity exports of these economies.

Meanwhile, the euro has struggled this week, tormented by business surveys warning the Eurozone economy is flirting with recession. The ECB is almost certain to raise rates on Thursday, so the burning question for the euro is whether policymakers will pre-commit to another move in September or whether the mounting signs of economic weakness will see them preach some caution.

Elsewhere, gold has been volatile but has gone nowhere this week, with the $1,960/ounce region acting as a magnet for prices. Behind this indecision lie conflicting forces, as the rising US dollar but falling real yields are pulling gold prices in opposite directions. This tug of war will probably be resolved tomorrow with the Fed decision.

Wall Street rallies ahead of tech earnings

The blistering rally in US equity markets resumed yesterday, with the S&P 500 closing less than 6% from its record highs. It’s been one-way traffic all the way up, without any serious corrections after the Fed’s liquidity injections back in March to shield the banking system.

On a macro level though, there isn’t much to celebrate. Corporate earnings are on track to decline by 7% - 9% from last year during this reporting season, which means the rally in equity markets has simply made stocks more expensive from a valuation perspective, as it hasn’t been backed by improving profitability.

As for today, Microsoft and Google-parent Alphabet (NASDAQ:GOOGL) will announce their results after Wall Street’s closing bell. With the AI hype reaching fever pitch, the earnings of these tech giants could affect the entire market, not just their own shares.