- The nub of the problem

- What China proposes to do about it

- What's missing?

- Relevant precedents

Risks involved

There's growing speculation that China will soon undertake substantial reforms to its financial system to address growing risks from escalating debt. First, the central government will take over some local government spending functions, such as social security and part of healthcare. Second, it'll allow local governments to issue bonds to replace the so-called local government financing vehicles (LGFVs). The changes are expected to be announced at a key meeting of Communist Party leaders in November.

If true, they'll represent the biggest reforms in China since 1998. They'll have enormous ramifications, including: i) the intention of reducing risks in the financial system but whether it does so remains to be seen ii) it'll slow bank loan growth, which was due to slow anyway iii) most importantly, it'll reduce infrastructure spending and put further pressure on commodity inputs which principally rely on Chinese demand (such as steel, copper, aluminium and iron ore).

The overall aim will be to cut corporate and local government debt, while also reducing investment. The problem is that other parts of the economy will need to pick up the slack if GDP is to stabilise at current levels. Namely, central government spending and household consumption. Also, China will need currency depreciation for exports to cushion the adjustment from corporate deleveraging. That's why you can probably expect cuts in interest rates and currency depreciation in the not-too-distant future. Without these two things, there'll be greater short-term economic pain than the new leadership would like.

Today's post will look at the likely policy changes in detail because they'll have a huge impact not only on China, but on Asia as well as developed world. We'll also investigate some of the risks involved with the proposed reforms.

The nub of the problem

To understand why China may announce these significant reforms over the next few months, it's important to recognise some of the serious issues that the country faces.

Put crudely, and as is widely reported, China has a debt problem. But those who compare this debt issue to the U.S. subprime crisis - a very common comparison - don't know what they're talking about. For whereas the U.S. problems originated form excessive household debt, China's debt problems are at the local government and particularly corporate sector levels. Household leverage remains low while central government leverage is also reasonable.

China's debt issues are more similar to those of Japan in 1990 and South Korea in 1997-1998. Both of these countries also had serious corporate indebtedness. One succeeded in addressing the problems quickly (South Korea) while the other didn't (Japan).

There are other differences between the Chinese issues of today and those of the U.S. pre-crisis. Chinese debt exploded from 2009 due to a 4 trillion yuan stimulus package designed to prevent the country from sliding into a recession/depression as much of the developed world did at that time.

The stimulus was principally debt-funded. State-owned banks lent money to state-owned companies (SOEs) which were deemed less risky than privately-owned businesses. Also, local governments financed public infrastructure works via off- balance sheet borrowing (LGFVs).

As you can imagine, the spending wasn't very productive and led to overcapacity in numerous sectors. The situation was made worse by:

1) The government keeping rates too low for far too long.

2) The explosion in lending to the so-called less risky SOEs turned out to be a serious mistake. It turned out many of them were risky, particularly when they earned negative returns on their investments. More significantly, it crowded out lending to small businesses, which led to significant strains in this sector.

3) A lack of proper funding channels for local governments. Local governments can't issue bonds. This means they relied on off-balance sheet vehicles, offering higher rates, to fund long-term infrastructure projects.

4) Financial innovation via wealth products became the go-to for loans to small business. These products had zero transparency and made financial guarantees which were subsequently shown to be highly dubious.

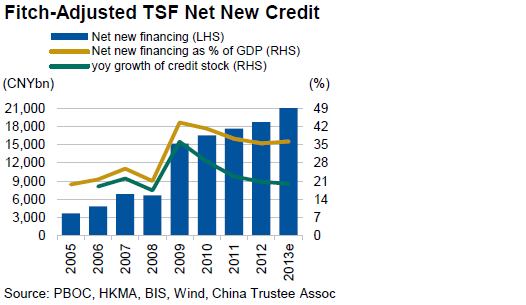

Because of all this, China now has a debt issue. Ratings agency Fitch puts total credit to GDP at almost 220%. More importantly, credit now accounts for more than a third of GDP. That means the economy is heavily reliant on increasing credit for GDP to remain at current levels.

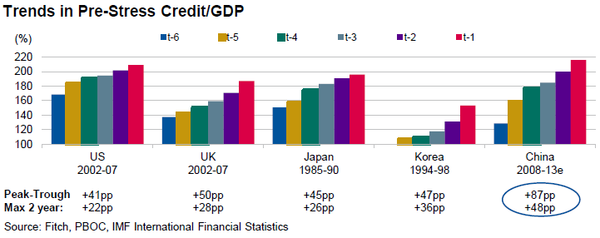

Where China does bear similarity to the U.S. and other countries who've experienced financial distress is with its rapid accumulation of debt. Credit to GDP will have risen by almost 90 percentage points for the five years ending 2013, nearly twice that of other countries prior to financial crises.

There are those who argue that China isn't as susceptible to a financial crisis because of its command economy. That is, it has more control over borrowers and lenders. It also has a closed capital account and a principally domestically-funded banking sector.

But it's also clear that credit can't keep rising significantly faster than GDP because the costs of servicing the debt will rise and unproductive investment will continue. Putting more money aside for debt servicing will leave less money for other government spending such as social security and so forth.

Put simply, the current situation isn't sustainable.

What China proposes to do about it

So there's the quick primer on China's credit problems. Now let's turn to the more important bit of what the government proposes to do about it.

For the past few months, stock brokers have been busy trying to get the inside dirt on the reform agenda for the high-powered meeting of Communist Party leaders in November (the 3rd plenary session of the Central Committee, as it's known). There's been speculation for several months that the central government will take over some local government spending functions. This week, Credit Suisse fleshed out some of the details on this and much more.

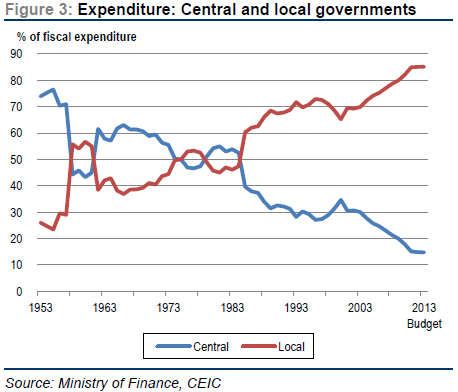

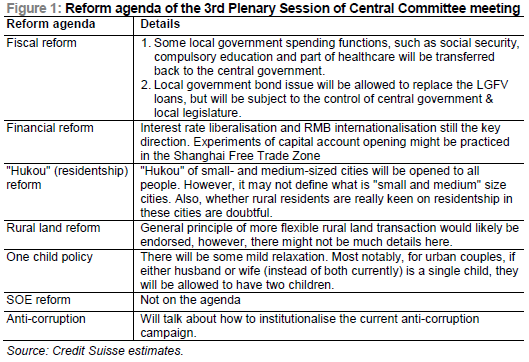

It said that it's likely the central government will take over key expenditure functions of local governments, including social security, compulsory education and parts of healthcare. The thinking is that there's a substantial skew in revenue and expenditures of central and regional governments. Currently, local governments account for 52% of total fiscal revenue but 85% of expenditure. Spending at the local government level has spiked from 46% of total to the current 85%. That's why these local governments have had to borrow money and why they've resorted to off-balance sheet vehicles to do it.

Secondly, Credit Suisse suggests that local governments at the provincial level will be allowed to issue bonds. And this financing will replace LGFV debt.

These two reform items will try to address obvious shortcomings in the current financial system such as: i) a significant fiscal transfer, of 9% of GDP, from central to local governments, which leaves room for significant corruption ii) a lack of proper financing channels for local governments, resulting in them resorting to off-balance sheet vehicles where transparency is limited iii) local governments being heavily dependent on land sales for revenue and property companies for funding.

Other likely reforms have been well-flagged and include f inancial liberalisation - interest rate liberalisation and RMB internationalisation -, Hukou (resident-ship reform) being opened to small and medium-sized cities as well as a relaxation of the one-child policy.

The reforms to local government are the most important ones and represent quite radical change. They will be nothing less than an overhaul of the financial system.

Credit Suisse suggests they'll have the following market implications:

1) They'll reduce financial system risks. Markets have been worried about escalating local government debt. These reforms could stabilise local government debt and the phasing out of LGFVs and issuance of bonds may make financing at the regional level more transparent. Read: less risky. I'm not convinced on this point, however.

2) Slow bank loan growth. LGFVs have been a boom business for banks and this would go.

3) Local governments at the provincial level will find funding more difficult for the likes of infrastructure projects. This will slow infrastructure and overall investment spend. It'll also slow the consumption of commodities reliant on this infrastructure spend.

What's missing?

The likely reforms neglect a few crucial issues, in our view. The first is the cleaning up of bank balance sheets. Everyone knows that the banks are sitting on massive non-performing loans from the dud credit they gave out, but no one knows exactly how much. The recognition of non-performing loans and bad debt write-offs will be critical.

Also, it seems SOE reform is off the agenda in the short-term. Again this is critical if China's to improve productivity growth. SOEs, particularly in key industries such as banking and energy, are choking off private sector involvement. That has to change.

Finally, there's little in the way of growth initiatives in the reforms above. If you cut back on local government expenditure, other areas of the economy must pick up for GDP to remain robust. Corporates aren't going to increase investment as they'll be busy deleveraging. That leaves central government spending and household consumption.

Therefore, I expect some initiatives post the November meeting to address the growth issue. More specifically, you're likely to get encouragement of household spending via increased subsidies and cuts to interest rates. You're also likely to get currency depreciation as this is the primary way to cushion the impact on corporates from deleveraging ie. a reduced currency will help exports. If that's right, that'll be a big turnaround given the substantial recent appreciation of the yuan.

Relevant precedents

Of course, there are many precedents of countries attempting to cut debt while maintaining economic growth. People forget though that China itself has been through financial crises of a similar nature to the current one.

The country went through a substantial deleveraging process from 1993-1998. In the early 1990s, SOEs as well as central and local governments dominated economic activity. In 1992, President Deng Xiaoping aggressively eased monetary policy which resulted in an investment boom as local governments borrowed through commercial banks and trust companies to finance their investment projects. M2 growth exploded, up 40% year-on-year in the first half of 1993. And fixed asset investment increased 60% year-on-year during the same period. Sound familiar?

In 1993, Vice-Premier Zhu Rongji tightened policy by enforcing loan quotas, turning the screws on interbank lending and suspending bank lending to the non-banking financial institutions. Again, does any of this sound familiar?

But Zhu also introduced several structural reforms. They included the privatisation and consolidation of SOEs, launch of a market-based resident housing system, commercialisation of the big-four banks and closure of many trust companies.

But as the debt-reduction measures were kicking in, along came the Asian Crisis in 1997. To ward off a much sharper slowdown, the government substantially eased policy, cutting benchmark rates three times by a total of 279bps and adjusting the 1998 budget through the issuance of an additional 100 billion yuan bond.

These policies, a combination of aggressive debt cutting and policy easing to cushion the blow, helped China get through the Asian Crisis relatively unscathed and paved the way for the extraordinary growth of the following decade.

Risks involved

While the China of today is different to that of the 1990s, the likely solutions to over-indebtedness, revolving around a policy mix of debt reduction and growth initiatives, could well be quite similar.

There are several obvious risks if China opts to pursue these kinds of policies though:

1) How much banks will have to cut lending growth and over how many years isn't known due to the lack of transparency in the financial system. This could impede any recovery scenario.

2) Any easy money policies via negative real rates will risk further asset bubbles. Easy money got China into this hole in the first place and it'll risk further damage going down this path.

3) Susceptibility to global shocks. When businesses are deleveraging, they're more vulnerable to external slowdowns. This is particularly in the case of China where exporters still dominate.

There's little doubt that these are challenging times for China. The consensus seems to be that China should be ok in the short-term but its long-term growth trajectory is in jeopardy.

I lean the other way, thinking the short-term pain is likely to be greater than expected given the popping of a credit bubble. However, structural reforms this year and beyond could put the country on a more sustainable economic footing, albeit at a lower economic growth level than today.