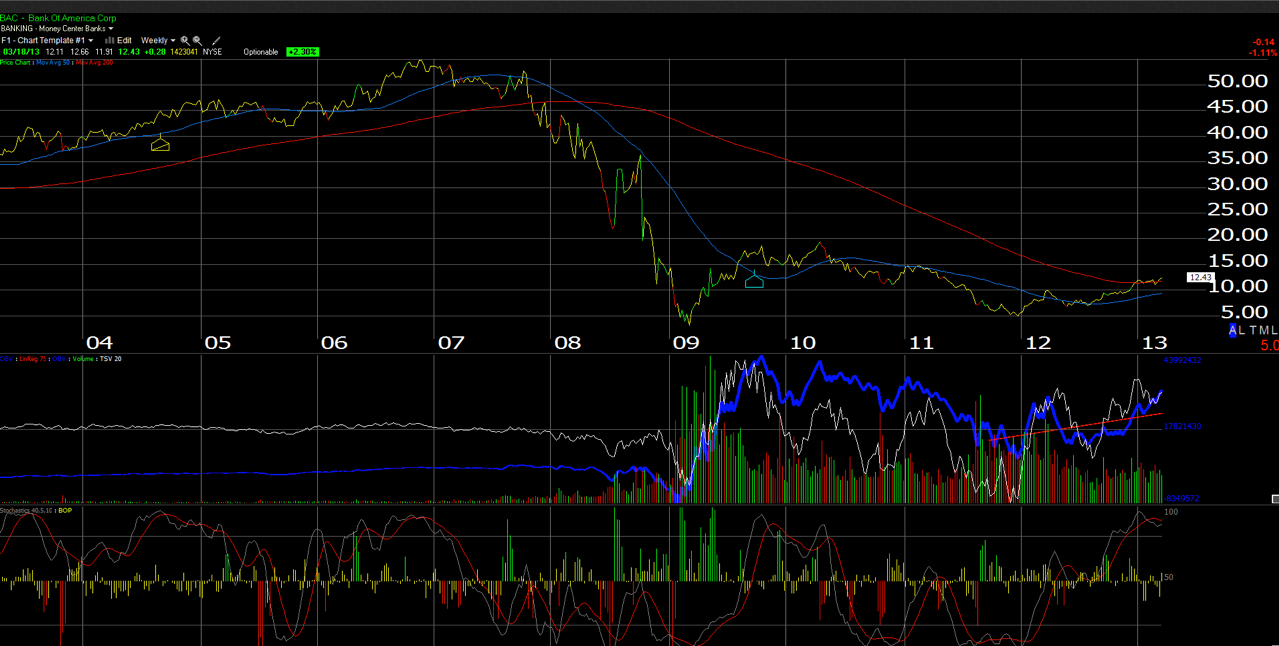

Bank of America (BAC) has edged above its 200-week moving average on the chart below and greatly improved its technical underpinnings. One of the reasons for the technical improvement (we think) is that BAC is a de facto play on the housing recovery, and as they settle these mortgage and insurance issues (from a litigation perspective), and the national housing market gradually improves, the “dash-to-trash” should help BAC’s balance sheet and capital as we move through the decade.

Current analyst consensus is looking for $1 and $1.31 in 2013 and 2014 and probably more importantly, the downward revisions have stopped and have started to turn slightly positive.

Book Value

BAC’s estimated tangible book value (TBV) is roughly $13.50 per share, so you can still buy the stock at a discount to TBV.

If you go back and look at the 2006 10K, BAC had about 4.5 billion, fully-diluted shares outstanding, but today that figure is over 10 billion. The Financial Crisis and the capital infusions severely diluted all bank shareholders, not just BAC.

Given the dilution, it will be a long, long time before BAC sees its old highs near $50 per share.

Buy The Pullback

BAC is now repo’ing shares and paying a dividend and as we said, we think the bank is a levered play on the housing recovery. We think BAC easily trades to $15, then $20 and we’d buy any pullback under $12.

Brian Gilmartin, CFA portfolio manager

Trinity Asset Management, Inc.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Chart Of The Day: Bank Of America

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2025 - Fusion Media Limited. All Rights Reserved.