Investing.com’s stocks of the week

Overview of the Ban

President Biden’s recent decision to prohibit oil drilling covers approximately 2.54 million square kilometers of oceanic territory, including parts of the Atlantic and Pacific coasts, sections of Alaska’s northern Bering Sea, and the eastern Gulf of Mexico. This vast area is comparable to the size of Sudan or Algeria. Notably, the central and western Gulf of Mexico, key to 14.5% of U.S. oil production and 4% of natural gas output, remain unaffected.

The newly restricted zones hold limited proven reserves. While the eastern Gulf contains unexplored potential reserves, their economic feasibility is questionable given the dominance of onshore shale extraction.

Global and Domestic Energy Context

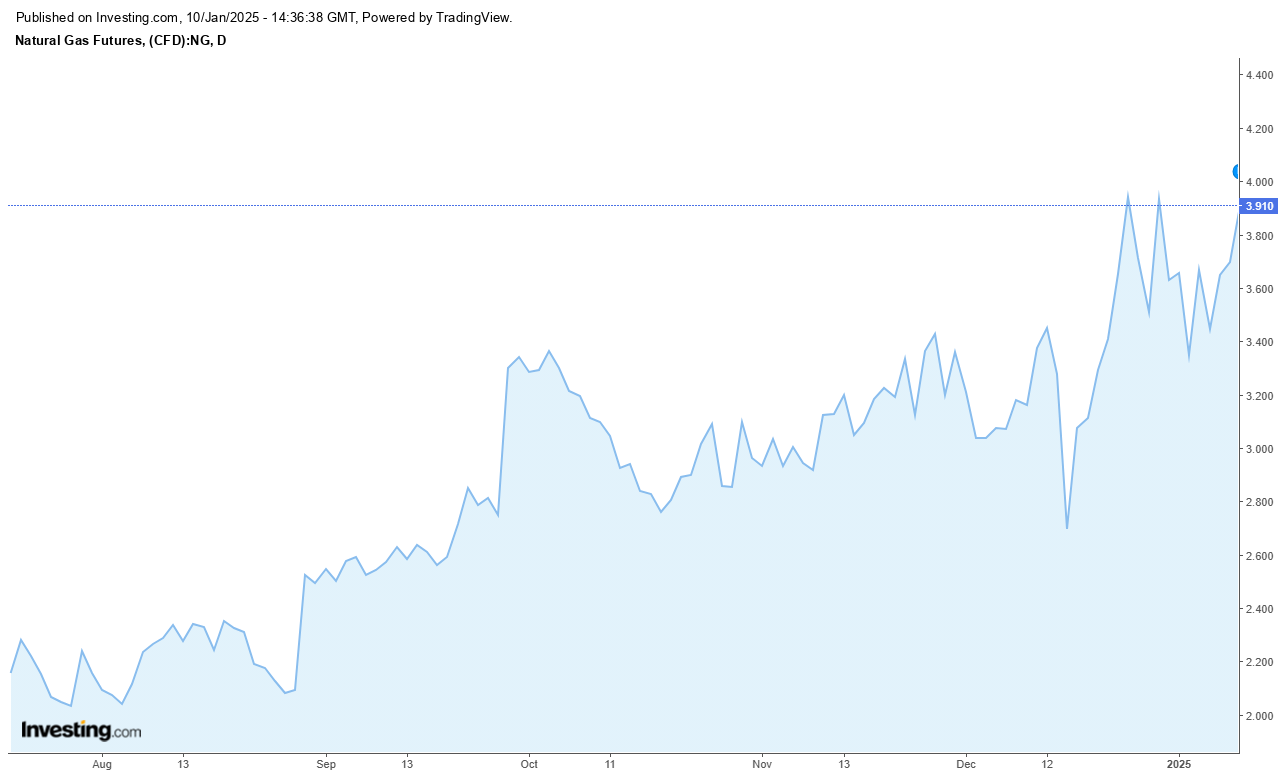

Globally, oil and gas markets are in a state of oversupply due to active development of existing fields. Natural gas markets, however, are driven by short-term factors such as weather and international LNG demand. Gas prices (NGG5) are expected to rise in the short term.

In the long term, U.S. oil production has a theoretical ceiling of 14.5 million barrels per day with current infrastructure. Exceeding this level would require significant investment in pipelines and drilling facilities. Increased oil production would also lead to higher associated gas output, supported by expansions in fields like Marcellus.

Shifts in Energy Production and Renewables

Gas-based power generation in the U.S. is projected to grow by 14% over the next two years, driven partly by the need for reliable backup to renewable energy sources. Coal-fired plants, however, are being phased out in favor of decarbonization policies. By 2025, U.S. renewable energy output from solar, wind, and hydro is expected to reach 1.1 trillion kilowatt-hours, leading the developed world.

The U.S. also plans to double its LNG export capacity. Currently, it exports 13–14 billion cubic feet of LNG daily, with peak capacities at 16 billion cubic feet. Despite this, domestic policies prioritize meeting internal demand, which will influence pricing dynamics.

Geopolitical and Economic Trends

Globally, oil consumption and prices are declining amidst rising competition among oil producers. The Middle East, in particular, is experiencing reduced U.S. military presence, signaling diminished geopolitical dependence on oil. While oil remains a financial tool for global markets, its prominence is waning, marking the shift toward the sixth industrial revolution.

Technologically advanced nations like the U.S. are transitioning to financial systems and energy frameworks less dependent on oil. This shift aligns with the Federal Reserve’s monetary policy, which aims to control global liquidity and redirect capital away from regions of lesser strategic value.

Oil Pricing Outlook

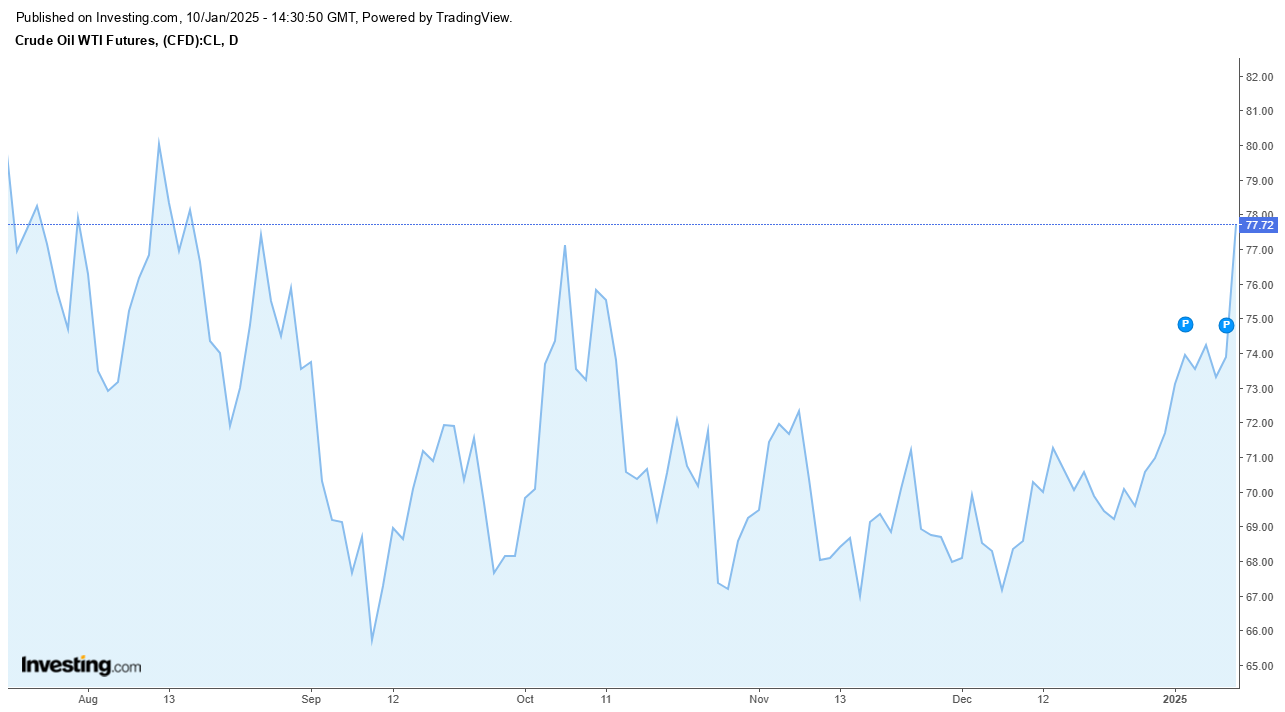

The U.S. aims to maintain stable energy prices, with oil prices (CG5) expected to hover between $70–$80 per barrel. This range is economically beneficial for the U.S. and reflects a broader policy of ensuring affordable and stable energy.

Political Landscape

While former President Trump has pledged to overturn Biden’s ban, historical precedent suggests significant legal and procedural hurdles. For instance, Trump’s 2019 attempt to lift an Arctic drilling ban was blocked, and he himself extended an offshore drilling moratorium in 2020.

Conclusion

The drilling ban is unlikely to have a significant impact on the oil market. Instead, it highlights broader shifts in global energy and economic strategies, emphasizing renewables, stable pricing, and long-term energy independence.