The recent outperformance of the U.S. economy has the dollar appreciating against most currencies over the past week. Some of the current price levels have a percentage of the market beginning to price in expectations of a “secular USD bull market.” Are they getting ahead of themselves? The dollars job has been made simpler by the various central banks easing up on their monetary policy rules -- just look at the RBA. Governor Stevens recent move has currently put the AUD into a structural decline. Even with Abenomics architecturally underway, it’s the stronger US data story that would suggest that Yen is about to undertake a substantial further depreciation ahead. In the single currency’s case, underperforming Euro-data is not helping the EUR’s cause.

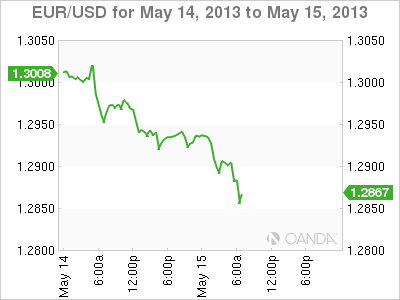

It’s not too much of a surprise to see that the euro zone has confirmed that their recession has extended into 2013 this morning, especially with the regions biggest supporters, France and Germany, releasing more wayward numbers. The euro-zone's economic output has contracted for a sixth straight quarter (-0.2%). The fear is that Germany (-0.1%, q/q), who provides one-third of total euro-zone output, is showing little signs of rebounding any time soon this year. EUR/USD" title="EUR_USD_1" width="400" height="300">

EUR/USD" title="EUR_USD_1" width="400" height="300">

In truth, the economic downturn that started in Greece three-years ago has now spread to the zone’s biggest contributors -- Germany, France, Italy and Spain. Record low interest rates and abundant ECB liquidity has stabilized the Euro’s debt markets, however, this accommodative policy has yet to filter down to ‘new’ spending, ‘new’ investing and ‘new’ hiring amongst the consumer level -- the meat and potatoes of anyone’s growth policy. Europe’s use of persistent austerity measures to dig themselves out of this deep manmade hole is however -- bleeding the end consumer is not working, hence the call for the euro zone and particularly Germany to consider embracing more of the free spending U.S. model approach to break GDP negative cycle.

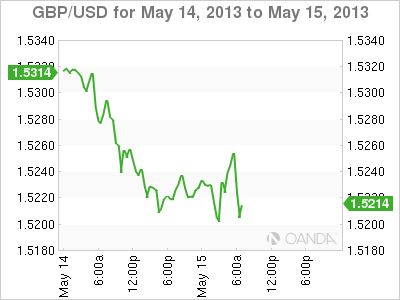

In the U.K. they have some jobs, but no money. Data released this morning confirmed that British jobless count is down and that the newly employed would not be boosting consumer spending much as the rise in average earning was reported at a record low (+0.8%). The number of unemployed rose for a third consecutive month (+15k), to a total of +2.52 million in March, a tad less than expected. The unemployment rate did beat the street, printing +7.8% vs. expectations of +8%. The UK labor market has shown some remarkable resilience in the face of persistently weak UK data. However, this negative consistency would suggest that whatever strength may have been left is soon to be lost. The UK’s Q1 expansion was certainly services supported and with the fall in real wages this trend is under threat going forward. Sterling happened to experience a short-lived positive knee-jerk reaction on the unemployment headline (+7.8%) where is has run into more offers north of 1.5250. GBP/USD" title="GBP_USD_2" width="400" height="300">

GBP/USD" title="GBP_USD_2" width="400" height="300">

US Treasury prices are pushing higher as signs continue to point to a lack of domestic inflationary pressures – a bondholder’s nemesis. With benign inflation being the order of the day in the U.S., it’s an excuse that could be levered to give the Fed more time to plan out its stimulus exit strategy. Falling energy prices are the culprit and have weighed heavily on last months U.S. import prices print (-0.5%, m/m). Investors should expect a similar effect to occur in this morning US PPI and tomorrows CPI headline release. Overtly, the Fed’s not that worried about disinflation just yet and that’s due to the nature of the “fluctuating” energy prices -- the state of the U.S. labor market remains their primary objective. Sustained price declines would keep QE in vogue, just look at Japan.

The deflationary concerns that currently weigh on global yields is not going away anytime soon. Just ask the Bank of Japan, they are the experts and know a thing or two about long-term deflation. The BoJ currently has its hands full trying to beat deflation. The cost of funding the country’s enormous budget deficit has been surging ever since last month’s “shock and awe” easing under Abenomics was introduced. Policy makers are hoping that GDP growth (tax revenues) will rise faster than debt funding costs. The BoJ is very much in the red on the JGB buys (they own +70% of new issues) and theses purchases are beginning to create liquidity problems -- Abenomics is working to a certain extent. The yen is trading deep, north of 102 and threatening to take on 103, but at what cost? If Japan cannot find any fiscal traction their currency will cause all sorts of problems.

The timing of a U.S. QE exit strategy is critically important. Currently, they are perhaps too many regional imbalances for the world’s largest economy to consider pulling back on its stimulus. The uneven pace of global economic growth could lead to two possible scenarios. The first, the globe experiences robust growth that helps the West to deleverage and the emerging economies to grow at a more rapid pace. The second, not as forgiving, inconsistent or uneven regional growth, which most likely would complicate debt-reducing efforts and perhaps cause further financial instability.

Despite the ECB’s well-anticipated rate cut and tentative dovish opening to negative interest rates this week, the EUR has continued to benefit somewhat from reduced credit risk premium and reserve diversification flows. However, in light of French and German GDP data this morning has helped to extend the 17-member single currency slide through 1.2900, opening up the ‘airways’ to test 1.2850 short-term. Fundamentally, the single-currency is bound to find much needed support in this region, as there is no reason to turn aggressively negative on the currency as long as there is no real widening in yield spreads that favor the “mighty” dollar.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Polski

- Português (Portugal)

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Being A Persistent Dollar Bull Is Hard Work

Published 05/15/2013, 08:17 AM

Updated 07/09/2023, 06:31 AM

Being A Persistent Dollar Bull Is Hard Work

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.