Silver (“Ag“) junior stocks have been destroyed over the past 3 months through July 17th. Not even companies (near to) or in production have been spared. Of course, the Ag price is the main reason for the carnage, it’s down 13.4% over the period. While 13% might not seem like a disaster, it is compared to gold (“Au“) [down 4.5% and copper (“Cu“) up ~5% since April 17th]. In the past several days, the Ag price has settled in, now ~US$16.20/oz., and some pundits are saying that select juniors are significantly oversold.

A name I believe to be oversold is Azarga Metals Corp (V:AZR). Not only is it off ~30% in 3 months, it was (and still is) under-appreciated to begin with. More tangibly, Azarga’s flagship project is roughly 50/50 Cu & Ag and, as mentioned, the Cu price is up ~5% since mid April. There’s no good reason for AZR to be trading off more than the average Ag focused junior! {I estimate the average Ag junior was down ~20% from April 17-July 17}

Azarga is a [C$7.5 M / US$5.9 M] market cap company listed on the TSX-V (ticker: AZR). It owns 60% [+ a call option on the remaining 40%] of the Unkur copper-silver project in eastern Russia, a project interest it acquired 16 months ago.

In April the company delivered a maiden NI 43-101 Mineral Resource estimate (“MRE“) of 42 Million metric tonnes (“Mt“) of 0.52% Cu and 38 g/t Ag — containing approximately 840 M Inferred pounds Cu Eq., or 124 M Inferred troy ounces Ag Eq. The MRE was established quickly and cost effectively.

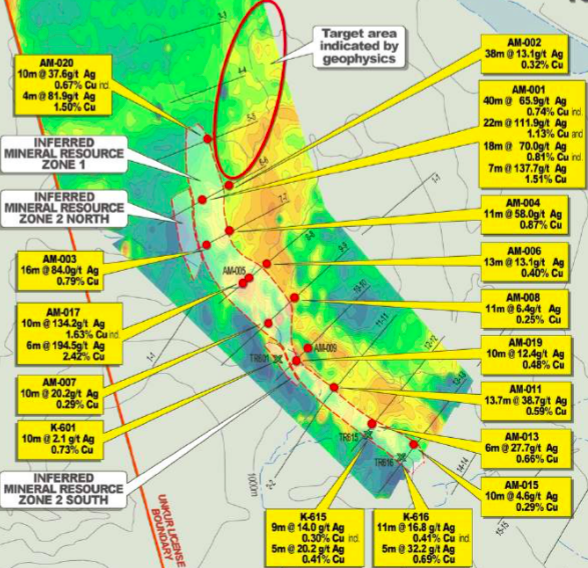

The first modern exploration program, conducted from Aug. 2016 – Feb. 2017, consisted of 16 diamond core drill holes (4,580 m), plus 4 trenches and sampling of various outcrops, tested a strike length of 3,400 m. In the map below, the red oval is an area of key interest, a zone of thicker and higher grade mineralization (confirmed by a ground magnetics survey) in the northern part of the Resource area.

Unkur is a high-grade deposit that was actively explored in the 1960s / 1970s, including drilling & trenching during the Soviet era. It has had several mineral resource estimates done on it, but none were (are) NI 43-101 compliant.

Four important features of the Resource are; (1) most of it (79%) is near surface, including two higher grade pods of mineralization. These pods could be amenable to low-cost open pit mining and could be mined earlier in a prospective mine plan, (2) mineralization is open in both directions along strike and down dip, (3) there’s now thought to be more than one layer of ore, not just a single mineralized zone, and (4) the MRE only covers about half the known strike length.

In an excellent Proactive Investors interview of CEO, President & Director Dusty Nicol in June, he stated that a potential doubling in size of the MRE was possible from the next drill campaign slated to start in August. A doubling in size and a likely increase in grade. He noted that the historic Soviet resource (not NI 43-101 compliant) of ~165 Mt is about 4 times the size of the MRE. New work done by the Company so far seems to indicate that the Soviet era data erred on the side of conservatism on both size and grade. Management continues to methodically validate the historical resource and is excited by results to date.

Regarding the opportunity to double the size of the MRE, Dusty thinks it could grow by a third or more from routine step-out drilling, connecting two known pods of mineralization in zone 2. And, if step-out drilling is successful in extending strike length by several hundred meters, there’s tonnage underneath the pit bottom that could be included in an updated resource later this year. The technical team, armed with a better understanding of what controls the distribution of high-grade Cu & Ag mineralization, is optimistic they can increase the overall grade by targeting geophysical anomalies to the North and Northeast. After raising exploration capital, drilling is expected to start in August.

The second phase of exploration will be carried out during the 2017-2018 field season and will focus on the potential for discovery of additional Cu /Ag mineralization from 3 target concepts: (i) drilling along strike or down dip; (ii) drilling to confirm additional mineralized zone(s) postulated to occur stratigraphically below currently defined Zones 1 & 2; and (iii) drilling new targets expected to be generated by geophysical surveys. The plan comprises geophysical exploration; {continuation of ground magnetics and initiation of electrical prospecting to the north and northeast of the currently defined resource} near-resource drilling; {8 diamond drill holes totaling 2,370 m} new target drilling; {~1,500 m of additional diamond drilling} and metallurgical characterization.CEO Nicol commented in June,

“Our objective this year will be to at least double the size of the current Resource while increasing overall Cu & Ag grades. Some of this increase is expected to come from step out drilling near the current Resource footprint. The remainder of the anticipated new Resource is expected to come from drilling of new targets from geophysics. Several such new targets have already been identified and drilling will focus on near-surface, high-grade targets as they’re identified.”

If the Company could double the size of the Resource to [840 M x 2 = 1.68 B lbs. Cu Eq.], it would be trading at just US$0.007 per lb. (net to Azarga) of Cu Eq. in the ground. {adjusted for Azarga’s 60% ownership of the Unkur project}

Dusty is fluent in 5 languages and has worked in 70 countries, he stated that access to infrastructure is better at Unkur than in 90% of the places he’s worked. He’s worked in really hard places in terms of terrain, weather and permitting, but Unkur’s location in eastern Russia is not expected to be challenging. Dusty has no trouble getting to site or getting rigs in. With the initial tonnage and grade and good infrastructure — less than 8 km from rail, direct rail to Vladivostok (a Pacific Ocean port) and Chinese smelters, power & groundwater onsite, — this next phase of exploration will support the work needed for a third-party NI 43-101 PEA or internal scoping study to be delivered in the Spring of 2018.

The project location has one advantage that few are talking about, namely a package of incentives provided to promote investment in Russia’s far east. There are tax incentives and royalty reductions, but the most important thing is the Far East Development Fund (“FEDF”), a development bank specifically set up for the region. It offers debt & equity funding and loan guarantees on preferential terms for projects such as Unkur. Azarga has a strong presence in Russia, it has boots on the ground. The entire technical team at site and administrative team in the city of Chita is Russian, and a significant percentage of the Company’s shareholder base is Russian.

Catalysts over the remainder of the year include; drill results, results from geophysics and metallurgical testing, and a new Resource estimate. A PEA or internal scoping study is expected in the Spring of 2018. Readers are encouraged to check out this 12-minute video interview of CEO Nicol to learn more about the Company and its plans for the remainder of the year.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Azarga Metals Corp, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Azarga Metals Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares and stock options in Azarga Metals and the Company was an advertiser on [ER]. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.