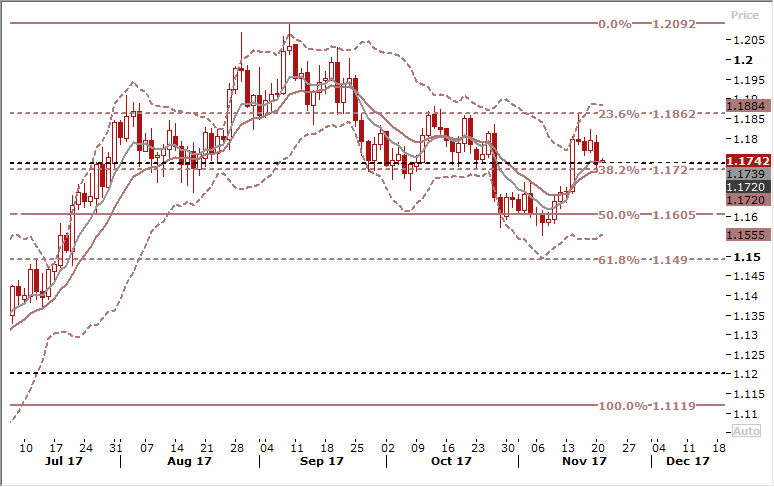

EUR/USD: Calm reaction to political uncertainty in Germany

Macroeconomic overview:

- German President Frank-Walter Steinmeier will meet the party heads of the Greens and the FDP today in an attempt to revive the Jamaica coalition negotiations and to avoid new elections. Tomorrow, Steinmeier will also meet SPD party chairman Martin Schulz. In our view, the chances of a successful resumption of the coalition negotiations or the formation of a new grand coalition are low. Yesterday, Angela Merkel announced that she would run again as the CDU/CSU’s candidate for chancellor in the event that there are new elections. Merkel basically ruled out the formation of a minority government. The latest available opinion polls, which were conducted yesterday, signal a political landscape largely unchanged since the general election in September(DeutschlandTrend): CDU/CSU (32%); SPD (22%); AfD (11%); FDP (10%); Left (10%); Greens (11%).

- Fixed income markets have been unimpressed by political developments in Germany, which probably reflects fact that good economic fundamentals will remain the most important driver as well as, to some extent, expectations that an agreement will be eventually found, avoiding the need for early elections at least in the near term.

- Political developments in Germany also remain center stage for FX markets; like on other asset classes, investor reaction has been surprisingly subdued so far: EUR/USD managed to recover above 1.750 after an early modest dip to 1.1723 and EUR/JPY rebounded back to around 132. With the German recovery already well underway (GDP rose 0.8% qoq in the third quarter 2017, bringing annual growth to 2.8% yoy), investors seem to consider the collapse of government talks in Berlin as unlikely to harm the economic outlook. Nevertheless, we think that markets are underestimating the risk of new general elections in Germany, which may be called for early next February. EUR/USD 3M implied volatility remains quite low, confirming that markets are shrugging off these negative developments. A minority government – for which the FDP offered support – would also be very troublesome for Angela Merkel, in our view, and may, in the end, just delay the electoral test.

- That said, we do not think that unexpected political uncertainty in Germany would derail the EUR/USD convergence to its fair value of 1.2400 that we expect in 2018, given strong Eurozone fundamentals. However, markets are long enough on the common currency at the moment, as IMM weekly data on non-commercial commitments indicate, and this may increase the risk of correction from time to time. On balance, we think that EUR/USD will probably remain more nervous and volatile than anticipated over the next few weeks.

Technical analysis and trading signals:

- The positive cross on the 7/14-ema last week was an important bullish sign. We stick to our bullish view and think that buying on dips could be a profitable strategy.

- We stay long at 1.1714 for 1.1960.

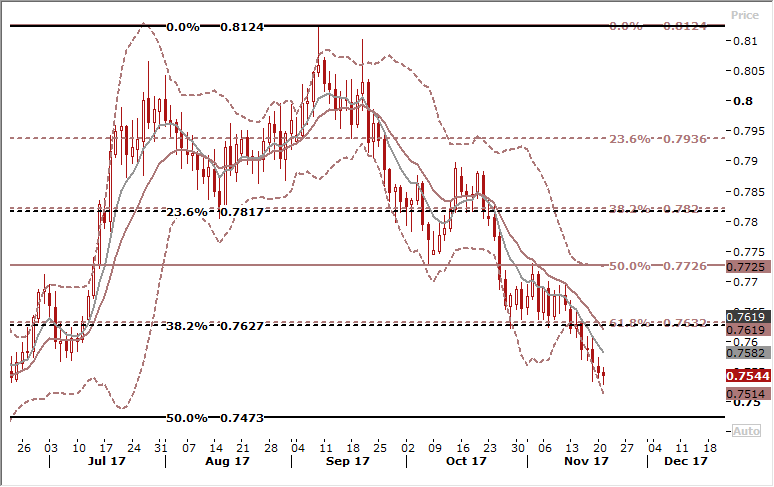

AUD/USD slips to 5-month low on RBA minutes

Macroeconomic overview:

- Minutes of the Reserve Bank of Australia's November 7 policy meeting showed it harboured "considerable uncertainty" about how quickly wages growth and inflation might pick up.

- Minutes showed policymakers pondered subdued consumer prices and pay rewards across the economy against the backdrop of sky-high household debt.

- The meeting came as the RBA cut its forecasts for core inflation, which is now seen lurking under its long-term 2-3% target band for another two years.

- Figures out since the meeting showed wages grew at an annual pace of just 2% in the third quarter, again disappointing hopes for an acceleration. "In particular...pressure on margins from strong competition and a faster-than-expected pick-up in productivity growth could delay the pass-through of tighter labour market conditions to inflationary pressure," the minutes showed.

- The RBA had been hopeful of inflation firing up as employment proved surprisingly strong, but data out last month showed another quarter of lukewarm consumer prices. Tepid inflation was a major reason the central bank cut interest rates to an all-time trough of 1.50% in August 2016.

- The low growth in salaries is eating into spending power and slugging the retail sector where sales suffered a rare contraction in the third quarter.

- In a speech last week, RBA Deputy Governor Guy Debelle said policymakers were well aware that the country's heavily indebted household would struggle if interest rates were to rise sharply, but there was no shock on the horizon to force such an increase.

- Indeed, the futures market has responded by pushing out the likely timing of a rate hike to early 2019. A couple of months ago, a move had been priced in for July 2018. The central bank's economic outlook was guardedly optimistic, noting that strong jobs growth across the country was supporting household incomes. In addition, government spending on public infrastructure had boosted private business investment and is likely to support economic growth for some time. Tuesday's minutes showed the RBA expects Australia's economy to grow around 3% over the next few years as the drag from a mining downturn diminishes and exports gather momentum. A further appreciation in the local dollar could jeopardise those forecasts, members noted.

- The Australian dollar slipped to a fresh 5-month low on Tuesday as minutes from a meeting of the country's central bank voiced concerns on sluggish wages and cemented views that interest rates will stay at record lows for months. The AUD/USD has been on a downtrend since early September when it climbed atop 0.8100. It has since lost 6.5% amid diminishing expectations of an interest rate hike and rising U.S. bond yields.

Technical analysis and trading signals:

- Bear sentiment persists as pair broke below Friday’s low. RSIs are biased down and not diverging. Further losses are likely. The test of 50% fibo of 2016-17 ascent at 0.7473 is a probable scenario.

- We stay sideways.