- Fed lifts dot plot, adds fuel to dollar’s engines

- Focus turns to core PCE index, the Fed’s preferred inflation gauge

- Slowdown could hurt the dollar, but broader outlook remains bright

- The data is released on Friday, at 12:30 GMT Fed signals another hike, fewer cuts in 2024

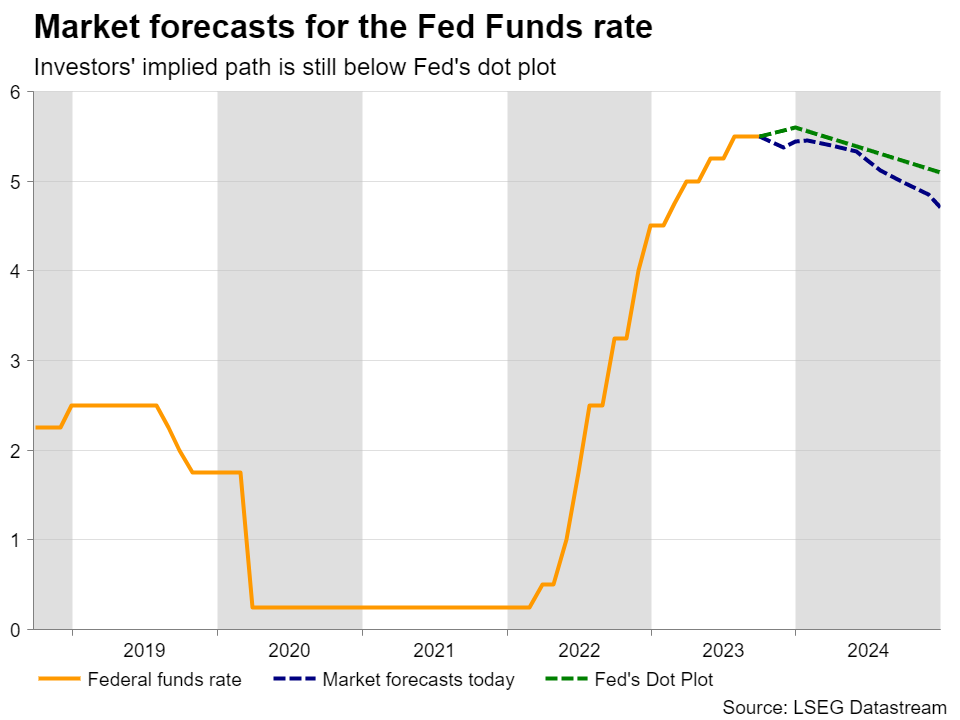

The Fed decided to keep rates steady last week, but policymakers appeared in hawkish armor, projecting a higher rate path than back in June. The new dot plot continued pointing to another quarter point hike by the end of this year, but only to two rate cuts during 2024. More specifically, officials now see rates coming down to 5.1%, 50bps higher than June’s 4.6% projection.

Still, investors were not fully convinced, as their own implied path points to only a nearly 50% probability for a final hike, while it indicates that interest rates will end 2024 at 4.7%. This suggests that there is still room for market participants to adjust higher their path should data continue to point to a resilient US economy, which in turn could add more fuel to the dollar’s engine tanks.

Focus turns back to the data

With that into consideration, although there is no data equivalent to Wednesday’s decision on this week’s agenda, investors may pay some attention to Friday’s core PCE index as it appears to be a more preferred inflation metric by the Fed than the CPIs, even if it is much less of a market mover. At the same time with the core PCE index, we get the personal income and spending data, while the day before, the final GDP for Q2 and initial jobless claims for last week are scheduled to be released.

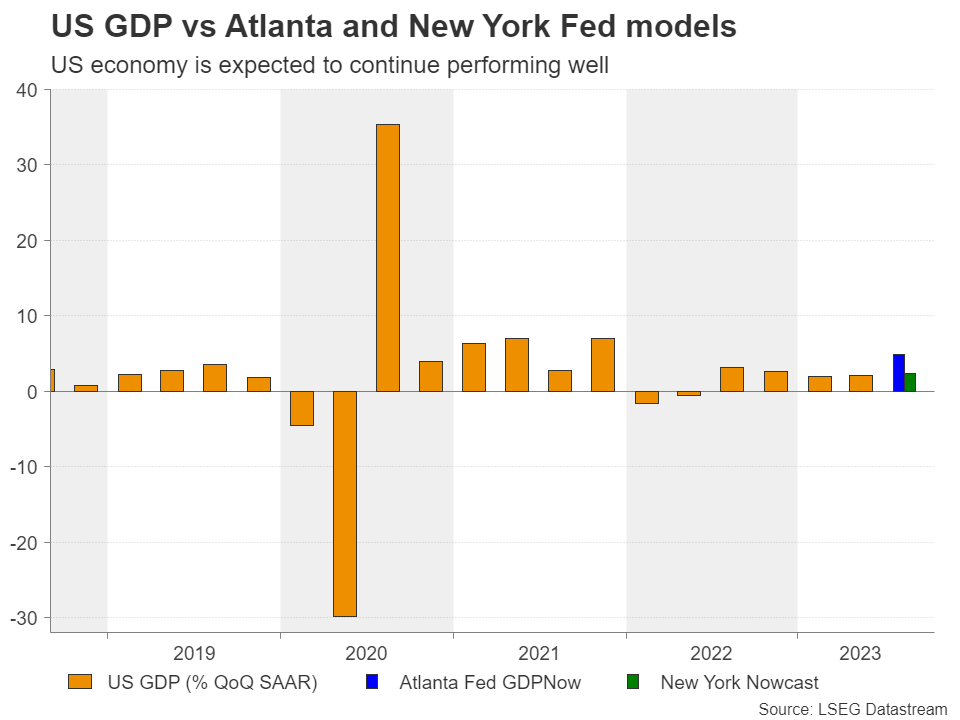

The GDP is likely to pass unnoticed as there are models already pointing to how the economy has performed during Q3. The Atlanta Fed GDPNow points to an outstanding 4.9% growth rate, while the New York Nowcast suggests that the economy grew around 2.3%. Although there is a big divergence between the two, they both point to a solid economic performance, which is unlikely to break the Fed’s “higher for longer” mentality.

Core PCE, income and spending, may all slow

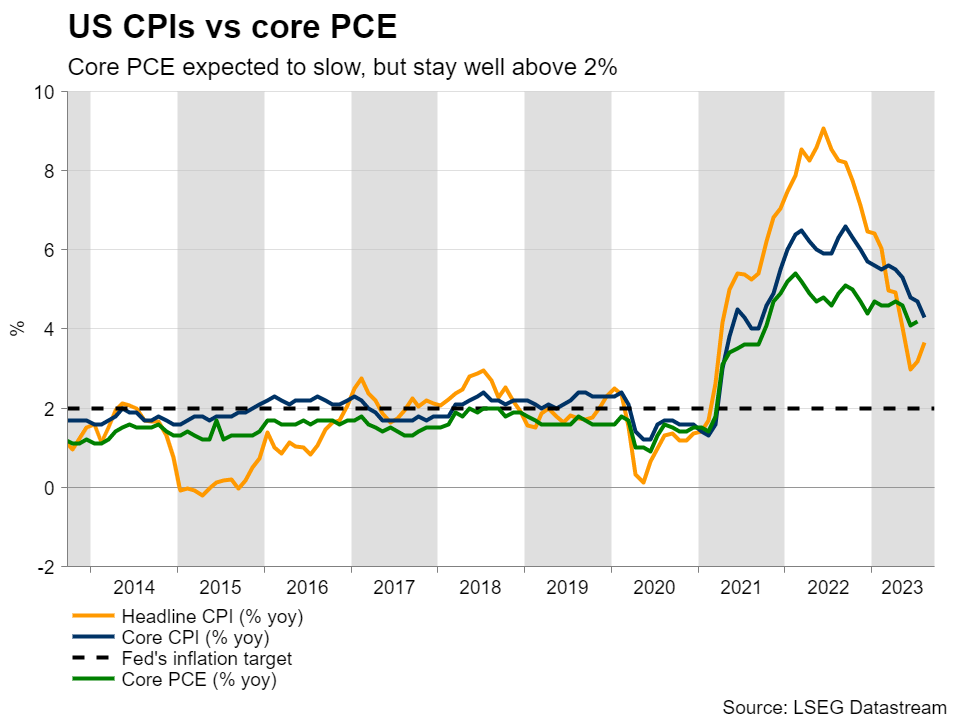

For Friday’s core PCE index, expectations are for a slowdown, which is supported by the cooling of the core CPI for the month. That said, even if this metric of underlying inflation slows, it would most likely remain decently above the Fed’s 2% goal. What’s more, considering the blend of a resilient economy and rising oil prices, the risk of a rebound in the months to come is not negligible.

Personal spending is also expected to have slowed, confirming the slight cooling in retail sales for the month, and thereby the reduced consumer demand. Although income is forecast to have accelerated, the deceleration in the monthly average hourly earnings for August tilts the risks to the downside.

Dollar could pull back, but stay in uptrend mode

The dollar could give back a small portion of its latest gains if the data adds to the idea that inflation in the US continues to cool down. However, a potential slide would be far from suggesting that the uptrend has run its course. Should growth-related data continue to suggest that the US economy is faring better than other major ones, the dollar is likely to continue shining.

Besides the “higher for longer” narrative, another source of dollar strength may be risk aversion, as the latest challenges facing the Chinese economy, as well as the Eurozone and the UK, are directing extra flows into the US dollar, which due to the higher US interest rates seems to be investors’ safe haven of choice.

Cable among the pairs to continue suffering

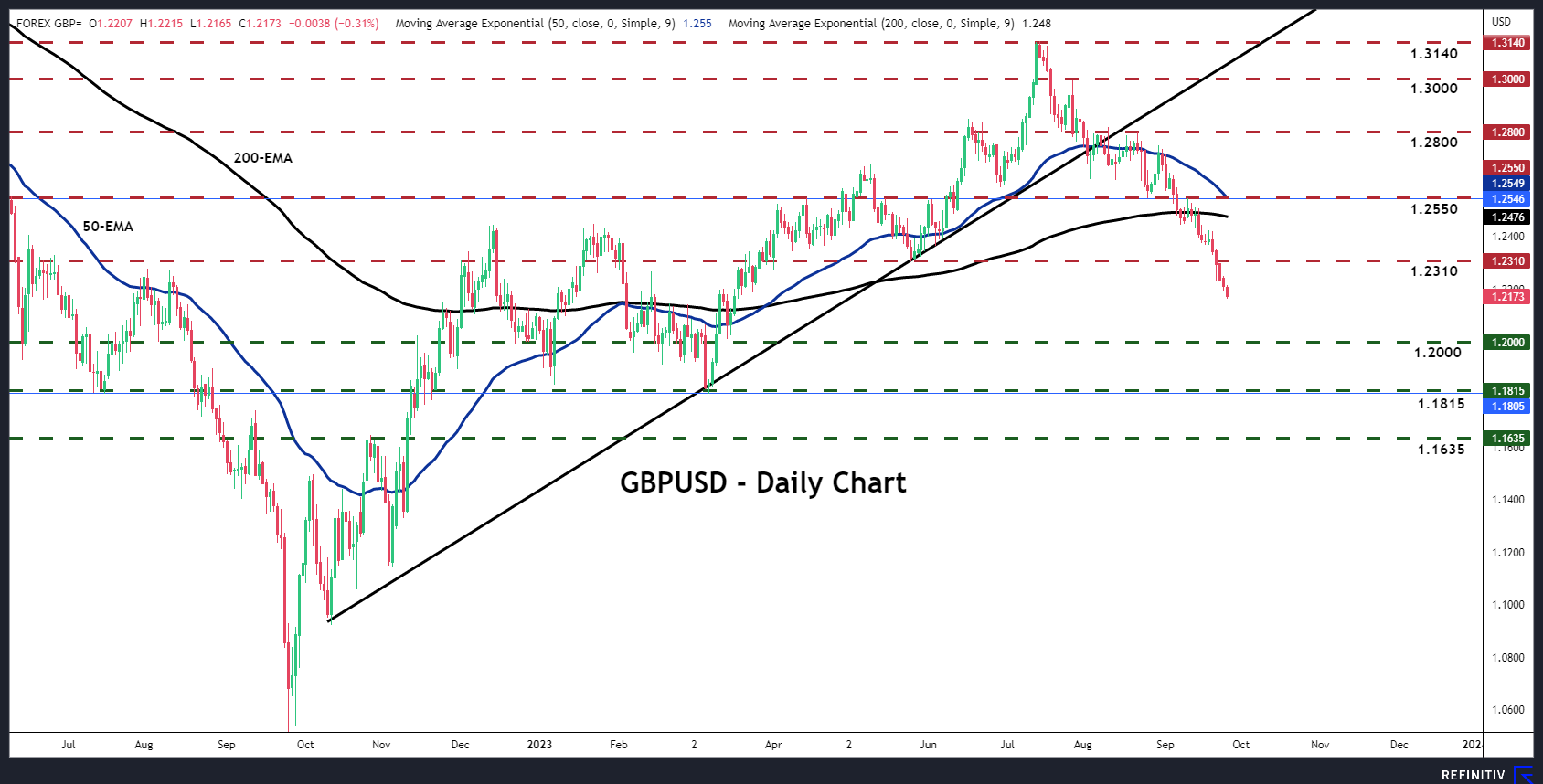

With the BoE unexpectedly taking the sidelines on Thursday and market participants assigning a 75% probability for no action at the November gathering, pound/dollar may be among the better choices for exploiting further dollar strength.

Cable has been in a sliding mode since mid-July and just after last week’s BoE decision, it pierced through the 1.2310 key zone, likely confirming a bearish trend reversal on the daily chart. The dip may have opened the way towards the psychological round number of 1.2000, marked by the low of March 15, the break of which could aim for the low of March 8, at around 1.1815.

On the upside, a return above 1.2310 is unlikely to make the picture brighter. It may just turn the outlook back to neutral. For this pair to enter uptrend mode again, a break above the key barrier of 1.2800 may be needed.