Volume Weighted Average Price, or VWAP, is an important indicator often used by day traders and institutional investors alike. Understanding the VWAP meaning and the VWAP calculation can help drive better buy and sell decisions.

What Is The Volume Weighted Average Price (VWAP)?

The volume-weighted average price, or VWAP, is the average price of a stock over a period of time, adjusted for the volume of those trades. Because of the volume component, VWAP assigns more weight to larger trades. And because it’s an average price across the period of time, VWAP offers a smoother view of the trading trend during the day.

VWAP is a trading benchmark that reflects the average price a stock has traded at throughout the day, based on both its volume and price. It is a crucial metric used by institutional investors and traders to measure and evaluate the quality of a stock’s trading performance, as well as to determine trends and market direction.

VWAP was first used in 1984 by a trader at Abel Noser, a Wall Street trading firm. It’s since become a core part of many trading strategies.

Volume-Weighted Average Price Formula

The formula for calculating VWAP is relatively straightforward and is based on three key factors: the price of the stock, its trading volume, and the time period being measured.

In theory, a perfect VWAP formula would include every single trade made during the trading session. With that data, the VWAP formula would look like this:

VWAP = ∑(Price × Volume) / ∑Volume

In this formula:

- Price: The price of the stock at any given moment during the trading day.

- Volume: The number of shares traded at that price level.

- Summation: This formula calculates the weighted average price of the stock over the trading day.

The VWAP calculation takes into account the volume of shares traded at various price levels, meaning that trades with higher volumes will have more influence on the VWAP. This is why VWAP is often considered a more accurate reflection of the true market value of a stock compared to the simple average price.

But that trade-by-trade data is not generally available. So, as a shortcut, traders can use what is known as the “typical price”

The typical price is equal to the average of the high, low, and close price for an intraday period. In other words, the typical price formula is:

Typical Price = (High + Low + Close) / 3

For each period (traders usually use 1-minute or 5-minute increments), the typical price is multiplied by the volume within that period. That figure is then divided by total volume for the day to that point, creating this VWAP formula:

VWAP = Sum of (Typical Price * Volume) / Sum of Volume

Example Calculation of Volume-Weighted Average Price

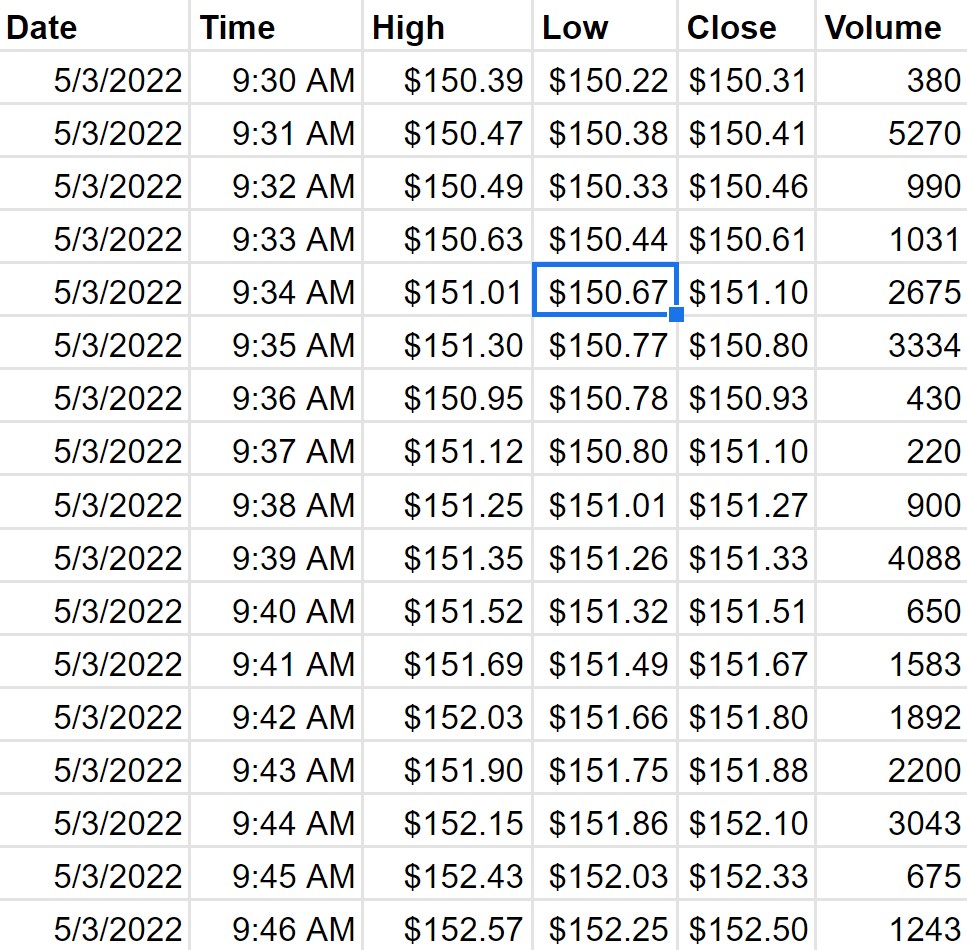

An example here may be instructive. Let’s look at hypothetical trading for ABC stock during the first 17 one-minute increments of a trading session:

For each increment, we first need to calculate the typical price. Again, that formula is (high + low + close) / 3.

So for the 9:30 am increment, our typical price equals ($150.39 + $150.22 + $150.31) / 3, or $150.3067. For 9:31 am, our calculation is ($150.47 + $150.38 + $150.41) / 3, or $150.42.

We repeat that calculation for each increment; we now have 17 typical prices. We then multiply each individual typical price by the volume for that time period.

For 9:30 AM, for instance, we multiply our typical price of $150.3067 by the volume of 380. At 9:31 AM, the typical price of $150.42 is multiplied by 5,270. These 17 sums are then totaled and divided by total volume for the entire period to get our VWAP from 9:30 am to 9:46 am.

In this case, the 17 sums (sometimes known as Typical Price Volumes, as they are derived by multiplying typical price and volume) total $4,628,406.32. Total volume over the entire 17-minute period is 30,604, providing a 17-minute VWAP of $151.24.

Example Calculation of VWAP in Excel

It’s obviously untenable to do these calculations on a line-by-line basis. The time taken would offset any potential trading benefits from calculating VWAP in the first place.

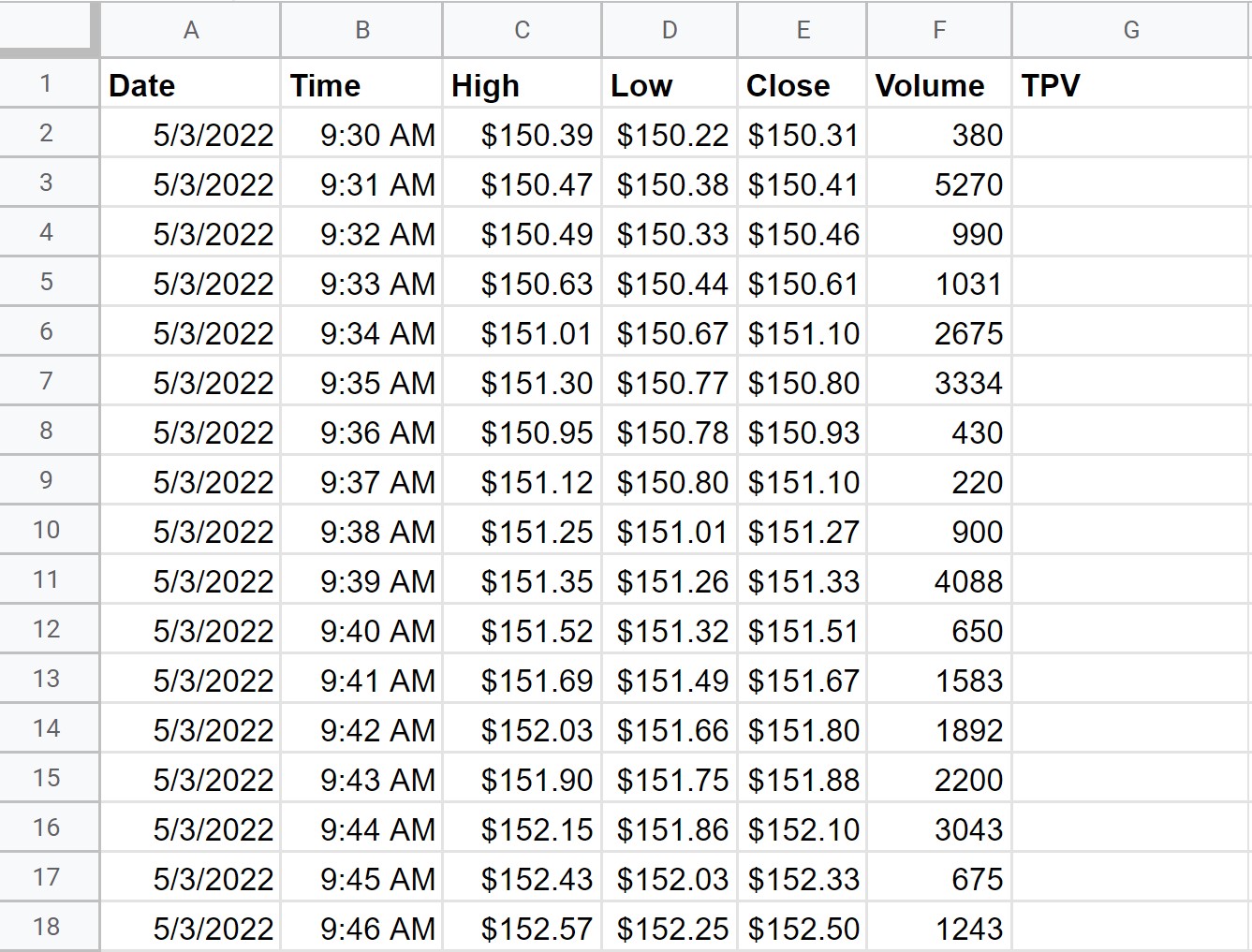

A well-designed Microsoft Excel spreadsheet can automate this process. Start by importing the necessary data — date, time, high, low, close, and volume. The next step is to create a column, which for simplicity’s sake can be abbreviated as ‘TPV’ for Typical Price Volume

:

We’ll then create a simple Excel formula for Typical Price Volume in cell G2, which mimics the TPV formula:

=((C2+D2+E2)/3)*F2

Again, we are looking to sum High, Low, and Close, which is (C2+D2+E2), and then divide by 3 to get the average. That typical price is then multiplied by volume for the increment (F2).

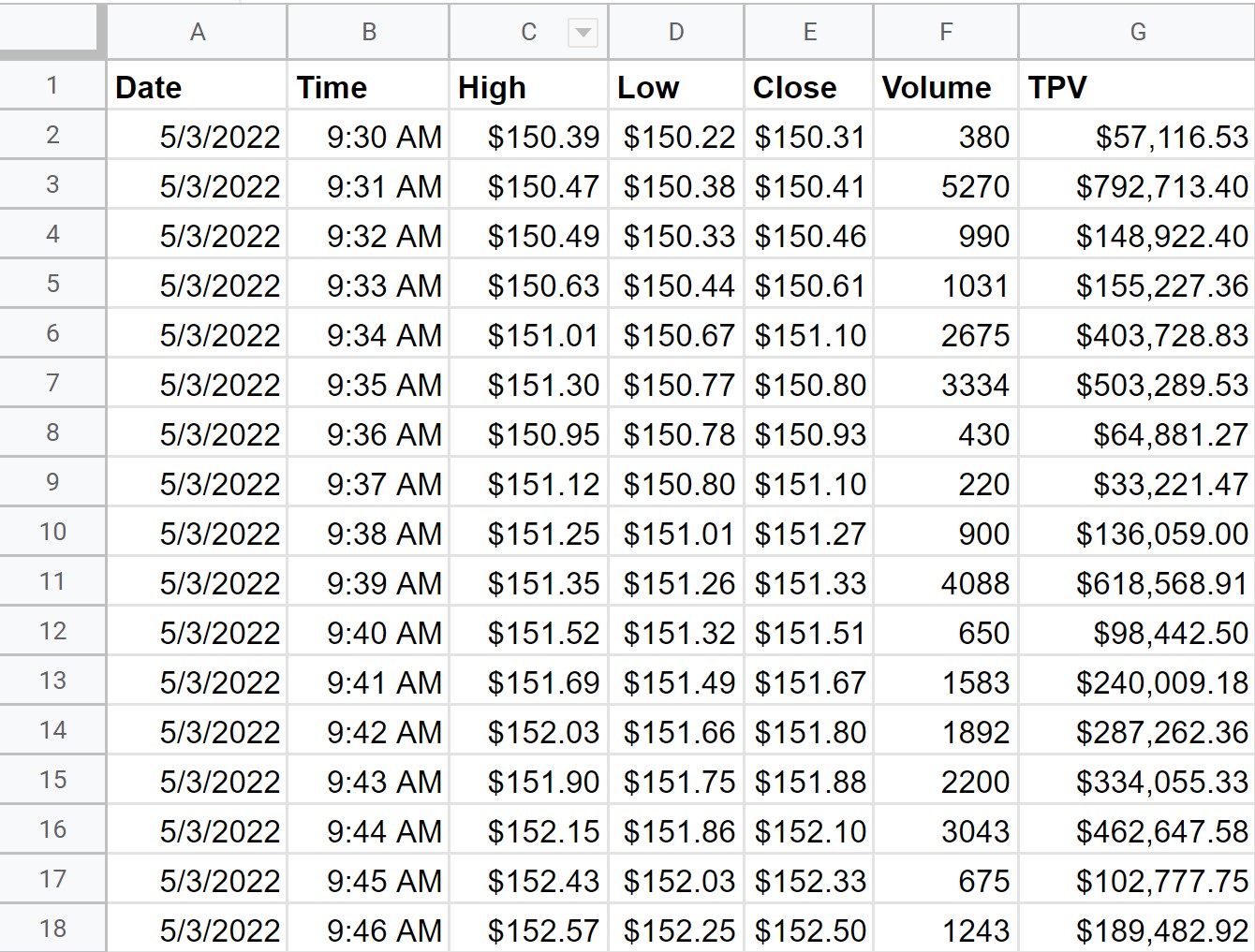

Fill or paste that formula down, and we have typical price for our time increments:

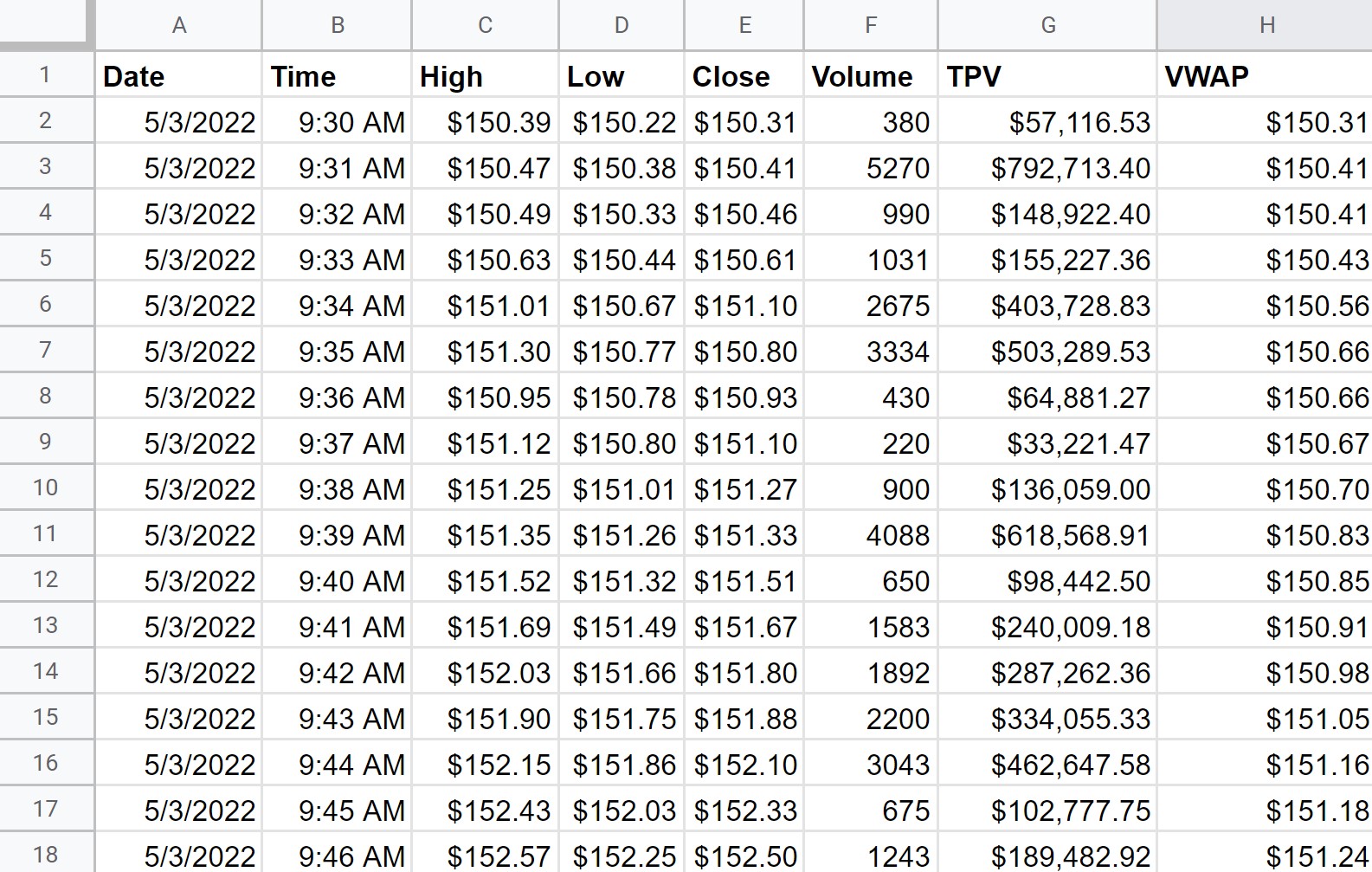

Now, we want to move to VWAP. To calculate VWAP, we can use an absolute reference in Excel. An absolute reference is signified by dollar signs preceding the letter and number of the cell, and anchors that cell when using a fill or paste function.

To calculate our VWAP, we want to sum our TPVs to that time point, and divide that total by volume to that time point. Our Excel formula thus looks like this for cell H2:

=(SUM($G$2:G2))/(SUM($F$2:F2))

And so we see that our sheet now calculates VWAP for each increment:

VWAP Strategy — How To Use VWAP

The core thought behind VWAP is that the incorporation of volume creates a truer sense of demand for and the trend of a stock. Imagine a simplistic hypothetical in which a stock ticks up on two trades, each for 10,000 shares — and then ticks down on two 100-share orders. The stock is back where it started — but demand in these four trades overall seems far more bullish than bearish.

Institutions that need to move those high-volume trades will thus often look to get as close to VWAP as possible. Staying near VWAP allows heavy volume to move in a series of trades without substantially moving the stock, since those trades in theory should be roughly in line with where demand sits.

Traders of all sizes, meanwhile, look at VWAP as better signifying where demand sits than a simple candlestick chart. A rising VWAP trend line shows that more money is moving into the stock. Yet if the stock price doesn’t reflect that strength, there may be a day-trading opportunity.

The converse is true as well: a falling VWAP trend line suggests that sellers are looking to move more volume, but that overall bearishness may not be reflected in the absolute trade-by-trade prices of the stock.

Traders who use VWAP strategies believe that the trend line toward the start of the day can often signal the direction of the stock for that session. If VWAP is rising, but the stock price isn’t, in many cases the market will eventually play catch-up — meaning day traders can buy the stock ahead of time.

More experienced traders will also use more complex VWAP strategies, viewing the metric as support or resistance much as longer-term traders do with moving averages.

Why Is The Volume-Weighted Average Price Important?

VWAP is used by experienced day traders as a metric that provides added context to simple price movements. But the metric has an important role in the corporate world as well. Many corporate transactions include “earnouts”, consideration that is based on a future stock price. Among the most common such transactions are SPAC (special purpose acquisition company) mergers.

SPACs bring private companies to the public market via mergers, most often at a price of $10 per share. Often, the owners and/or management teams of those private companies can receive additional shares if the stock price of the public firm reaches certain targets within a given time period. In this way, they are rewarded if the business outperforms expectations after the merger is complete.

In addition, nearly all SPAC deals include warrants. Like earnout shares, those warrants become redeemable for common stock once certain price targets are reached.

In theory, however, these price targets could be gamed. If an executive needed the stock to reach $15, for instance, they could make a single trade at that price.

To prevent any potential chicanery — or simply an odd trade that triggers earnouts or warrant redemptions — merger agreements require that the price target be based on VWAP across an entire session, rather than any single trade. In many cases, the target VWAP must be reached in 20 of 30 days.

This setup offers two advantages. First, it ensures that the stock holds the target level for a reasonable amount of time. Second, by using a volume-based measure like VWAP, it ensures that the market as a whole, and not just a few traders, is willing to pay that price.

How to Interpret VWAP?

Interpreting VWAP involves understanding how the stock’s price behaves relative to the VWAP value throughout the day. Here are key insights:

Price Above VWAP: When the price is above the VWAP, it generally indicates that the market is bullish, and buying pressure is dominant. Traders might consider long positions when the price consistently stays above the VWAP.

Price Below VWAP: When the price is below the VWAP, it suggests a bearish market, and selling pressure might be in control. In this case, traders may prefer short positions or avoid buying.

VWAP Crossovers: A crossover occurs when the price crosses above or below the VWAP. A price moving above the VWAP might signal a buying opportunity, while crossing below could suggest a selling opportunity or a shorting signal.

VWAP as Support or Resistance: Throughout the day, VWAP often acts as a level of support or resistance. If the price is above VWAP, it may find support at VWAP, and vice versa. Traders often watch for price rejections or rebounds near VWAP.

Multiple Timeframes: Traders may use VWAP on different timeframes to gauge market sentiment. For example, a 15-minute VWAP might help intraday traders, while a daily VWAP could be useful for understanding longer-term trends.

What is a Good VWAP?

A “good” VWAP depends on the context of a trader’s strategy and the market conditions. In general:

- Above VWAP: If the stock price is trading above VWAP, it indicates a bullish market sentiment, and traders might look for buying opportunities or confirmations of uptrend continuation.

- Below VWAP: If the price is below the VWAP, it suggests bearish market conditions, which may prompt traders to consider short positions or avoid buying.

- VWAP Crossovers: A good VWAP signal might be when the price crosses above or below the VWAP, signaling potential trend reversals or continuations. Traders generally prefer clean breakouts from VWAP for confirming trading opportunities.

VMA vs VWAP

That said, VWAP is not the same as moving averages, including what is known as VMA (a Variable Moving Average).

The core distinction is simple. VWAP is an intraday measure; its usefulness lasts no longer than a session. It’s an average price used as a benchmark for trading that day.

Moving averages, whether VMA or otherwise, consist of prices across multiple sessions.

Limitations of VWAP

While VWAP is a valuable tool, it has several limitations that traders must keep in mind. Below are five limitations:

Lagging Indicator: VWAP is a lagging indicator, meaning it is based on past price and volume data. As a result, it may not always accurately reflect real-time market conditions and may miss immediate changes in price direction.

Not Suitable for Long-Term Analysis: VWAP is primarily useful for short-term and intraday trading. It does not offer reliable insights for long-term trends or investment decisions, making it less suitable for long-term investors.

Not Effective in Low Liquidity Markets: VWAP is most effective in high liquidity markets. In low-volume stocks or during periods of low trading activity, the VWAP may not provide a true reflection of the market price.

Vulnerability to Market Manipulation: VWAP can be influenced by large trades or manipulation of the volume during certain periods. Large players can skew VWAP calculations, leading to misleading price signals.

Dependence on Time of Calculation: VWAP is calculated over the course of the day and resets each trading session. This means that VWAP does not provide a continuous measure of stock performance, and it must be recalculated for each new day.

How to Find VWAP?

InvestingPro offers detailed insights into companies’ Volume-Weighted Average Price including sector benchmarks and competitor analysis.

InvestingPro: Access VWAP Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to VWAP data within the InvestingPro platform. Plus:

✓ Access to 1200+ additional fundamental metrics

✓ Competitor comparison tools

✓ Evaluate stocks with 14+ proven financial models

VWAP FAQs

What does VWAP stand for?

VWAP stands for Volume-Weighted Average Price, which is an average price of a stock during a trading day, weighted by the volume of shares traded at each price.

How is VWAP different from moving averages?

Unlike simple moving averages (SMA), which only consider the average price over a specified period, VWAP incorporates trading volume, providing a more accurate picture of market dynamics.

Can VWAP be used in long-term trading?

VWAP is mainly used for intraday trading, as it resets each day. For long-term trading, other indicators, such as the moving average, may be more useful.

What is the best way to use VWAP?

VWAP is best used to identify trends, find entry and exit points, and manage large trades. It is especially useful for day traders and those executing short-term strategies.

How does VWAP help traders?

VWAP helps traders by providing a benchmark for assessing the price at which a stock is trading. It also helps identify buying or selling opportunities based on price behavior relative to VWAP.