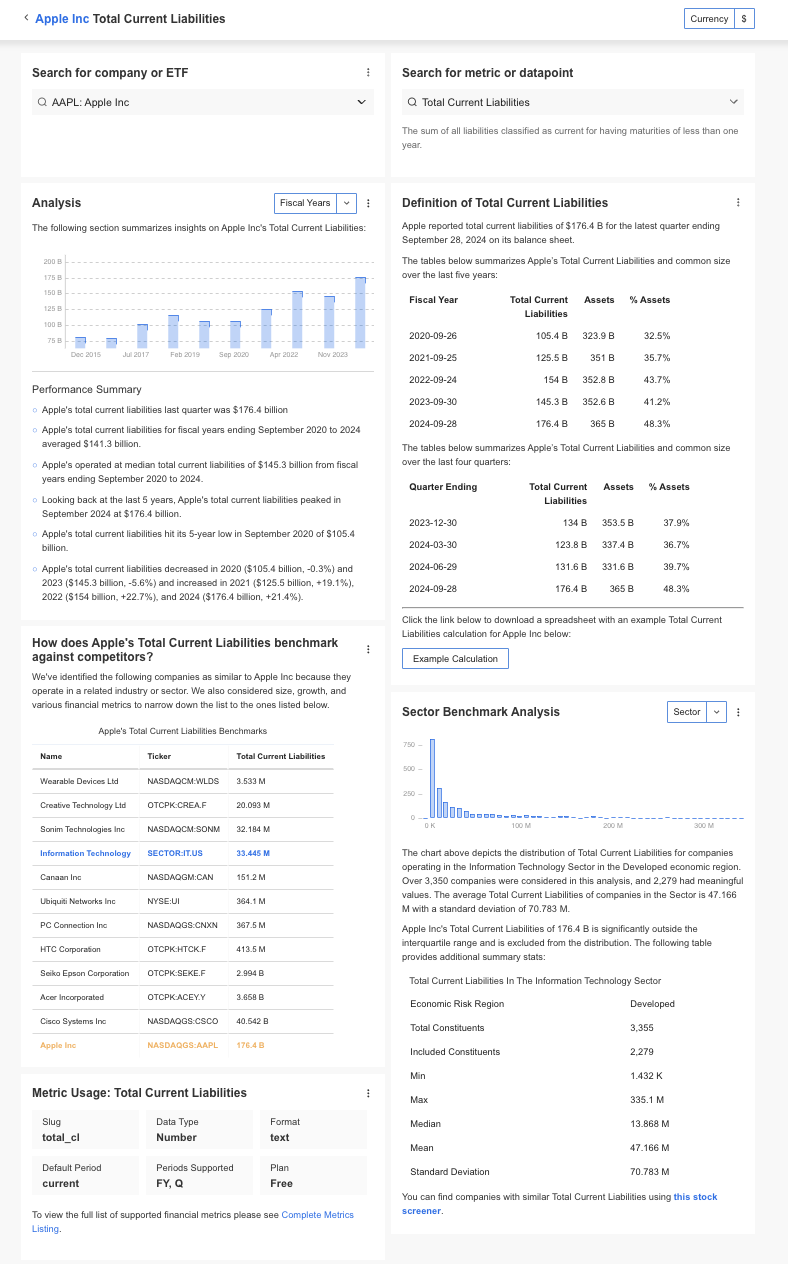

What is Total Current Liabilities?

Total Current Liabilities represent the sum of all short-term financial obligations a company must settle within a year. These include debts and other liabilities due in the near term, such as accounts payable, accrued expenses, short-term loans, and taxes payable.

This figure is a key component of a company’s balance sheet, offering insights into its ability to meet short-term obligations using available current assets. It’s a vital metric for assessing liquidity and operational efficiency.

How to Calculate Total Current Liabilities?

Calculating Total Current Liabilities involves summing up all liabilities expected to be settled within a year.

Total Current Liabilities = Accounts Payable + Short-Term Debt + Accrued Expenses + Taxes Payable + Unearned Revenue + Other Short-Term Liabilities

The liabilities in the aforementioned formula include:

- Accounts Payable: Payments owed to suppliers.

- Short-Term Debt: Includes loans, lines of credit, and portions of long-term debt maturing within a year.

- Accrued Expenses: Liabilities incurred but not yet paid, such as wages and utilities.

- Taxes Payable: Income taxes and other government obligations due in the short term.

- Unearned Revenue: Payments received for services yet to be provided.

- Other Short-Term Obligations: Includes dividends payable or short-term lease liabilities.

Example Calculation of Total Current Liabilities

Consider a company ABC has the following short-term obligations:

- Accounts Payable: $100,000

- Short-Term Debt: $50,000

- Accrued Expenses: $25,000

- Taxes Payable: $10,000

- Unearned Revenue: $15,000

Using the formula:

Total Current Liabilities = 100,000 + 50,000 + 25,000 + 10,000 + 15,000

Total Current Liabilities = $200,000

Company ABC has $200,000 in obligations it must settle within a year. Stakeholders can use this figure to analyze the company’s liquidity and short-term financial health.

Why is Total Current Liabilities Important?

Total Current Liabilities play a crucial role in understanding a company’s financial health, particularly its ability to manage short-term obligations. For stakeholders such as investors, creditors, and management, this metric provides valuable insights into liquidity, operational efficiency, and financial risk.

Understanding the metric is crucial for several reasons:

Assessing Liquidity

By comparing Total Current Liabilities to Current Assets (via the current ratio), stakeholders can gauge whether a company has enough resources to meet short-term obligations.

- Liquidity Ratios: The comparison between Total Current Liabilities and Current Assets forms the basis of important liquidity ratios like:

- Current Ratio (Current Assets / Total Current Liabilities)

- Quick Ratio ((Current Assets – Inventory) / Total Current Liabilities)

A well-balanced ratio indicates that the company can comfortably meet its obligations, reassuring stakeholders about its short-term financial stability.

Evaluating Operational Efficiency

The composition and size of Total Current Liabilities provide insights into how efficiently a company manages its day-to-day operations.

- Accounts Payable: Large accounts payable balances could indicate strong supplier relationships with favorable credit terms.

- Accrued Expenses: Managing accrued expenses effectively reflects the company’s control over operational costs.

A stable or declining level of current liabilities often suggests better financial discipline and operational efficiency.

Supporting Creditworthiness Analysis

Creditors use Total Current Liabilities to assess a company’s short-term solvency before approving loans or extending credit.

- Low Liabilities: Suggest low risk, improving the likelihood of securing favorable loan terms.

- High Liabilities: May signal financial stress, leading creditors to demand higher interest rates or stricter repayment terms.

Identifying Potential Risks

Total Current Liabilities serve as an early warning signal for potential liquidity challenges.

- High Liabilities vs. Low Current Assets:

A mismatch between liabilities and available assets may indicate financial strain, requiring immediate corrective actions. - Debt Concentration:

A significant portion of liabilities tied to short-term debt can increase vulnerability to interest rate fluctuations or cash flow disruptions.

Providing Insights for Investors

For investors, Total Current Liabilities offer a window into the company’s financial health and operational priorities:

- Cash Flow Management: High liabilities may suggest potential cash flow constraints, affecting dividend payments and reinvestment capabilities.

- Sustainability: Companies with excessive liabilities relative to assets may struggle to sustain operations during economic downturns.

Investors often use this metric alongside other financial data to assess the risk-reward profile of their investments.

How to Interpret Total Current Liabilities?

The interpretation of Total Current Liabilities depends on its relationship with other financial metrics:

In Relation to Current Assets

A company’s ability to cover Total Current Liabilities with its Current Assets is measured by the current ratio:

Current Ratio = Current Assets / Total Current Liabilities

- Current Ratio > 1: Indicates sufficient assets to cover liabilities, signaling liquidity.

- Current Ratio < 1: Suggests potential liquidity challenges.

In Relation to Revenue

Comparing Total Current Liabilities to revenue offers insights into whether the company’s income can sustain short-term obligations.

In the Context of Industry Norms

Different industries have varying benchmarks for Total Current Liabilities. For instance:

- Retailers may have higher liabilities due to inventory financing.

- Service-based businesses often carry fewer liabilities due to lower operating costs.

What is a Good Total Current Liabilities?

A “good” Total Current Liabilities figure varies based on the company’s size, industry, and financial strategy. However, some general guidelines include:

- Low to Moderate Liabilities: Indicates manageable obligations relative to assets and revenue.

- Aligned with Industry Standards: Helps ensure that liabilities are neither excessive nor too conservative compared to peers.

- Backed by Sufficient Current Assets: A current ratio above 1 typically suggests a healthy balance between assets and liabilities.

What are the Limitations of Total Current Liabilities?

While useful, Total Current Liabilities has its limitations:

- Lack of Context: By itself, this figure doesn’t indicate whether liabilities are manageable. It must be compared to assets or revenue.

- Does Not Reflect Cash Flow: High liabilities might not be an issue for companies with strong cash flow, but the metric doesn’t capture this dynamic.

- Industry Differences: Comparing Total Current Liabilities across industries can be misleading, as financial structures vary widely.

- Snapshot in Time: Total Current Liabilities reflect a specific moment and may not account for seasonal or cyclical variations in a company’s financial position.

- No Insight into Profitability: The metric focuses on obligations, not on whether the company generates sufficient profits to manage these liabilities.

How to Find Total Current Liabilities?

InvestingPro offers detailed insights into companies’ Total Current Liabilities including sector benchmarks and competitor analysis.

InvestingPro+: Access Total Current Liabilities Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to Total Current Liabilities data within the InvestingPro platform

🛠 Access to 1200+ additional fundamental metrics

🔍 Competitor comparison tools

📊 Evaluate stocks with 14+ proven financial models

Total Current Liabilities FAQ

What are Total Current Liabilities?

Total Current Liabilities are the sum of all short-term obligations a company must settle within a year, such as accounts payable and short-term loans.

How do Total Current Liabilities differ from Total Liabilities?

Total Current Liabilities include only short-term obligations, while Total Liabilities encompass both short-term and long-term obligations.

Why are Total Current Liabilities important?

They help assess a company’s liquidity, short-term financial health, and ability to meet immediate obligations.

What is a good level of Total Current Liabilities?

It depends on the industry and company context but should be manageable relative to current assets and revenue.

How can a company reduce Total Current Liabilities?

By paying down short-term debt, renegotiating payment terms with creditors, or increasing operational efficiency to manage expenses.

Are high Total Current Liabilities always bad?

Not necessarily. High liabilities can support growth if backed by strong revenue or cash flow, but excessive liabilities relative to assets can indicate risk.