What is Tangible Common Equity?

Tangible Common Equity (TCE) is a financial metric used to measure a company’s ability to absorb losses and maintain financial stability. It represents the portion of a company’s equity that remains after subtracting intangible assets like goodwill, patents, and trademarks. The term “tangible” refers to assets that have a physical presence, such as property, equipment, and cash, while “common equity” denotes the ownership equity held by common shareholders, excluding any preferred shares.

By focusing on tangible assets and excluding intangible ones, TCE provides a more conservative measure of a company’s real, readily available capital. This can give investors, creditors, and analysts a clearer picture of the company’s financial stability, especially in times of economic volatility.

How to Calculate Tangible Common Equity?

To calculate Tangible Common Equity (TCE), you can use the following formula:

TCE = Total Common Equity − Intangible Assets

Where:

- Total Common Equity is the total equity attributable to common shareholders, found on the company’s balance sheet.

- Intangible Assets include items like goodwill, patents, trademarks, and other non-physical assets.

Example Calculation of Tangible Common Equity

Let’s consider a hypothetical company, XYZ Corporation, with the following balance sheet information:

- Total Common Equity: $500 million

- Intangible Assets (Goodwill, Patents, etc.): $100 million

Using the formula:

TCE = 500 million − 100 million = 400 million

In this case, XYZ Corporation’s Tangible Common Equity would be $400 million. This means the company has $400 million in tangible assets that can be used to cover its liabilities if needed.

Why is Tangible Common Equity Important?

TCE is essential for assessing the underlying financial strength of a company, especially in industries like banking and finance where it is crucial to have a solid equity base to mitigate risks. Tangible Common Equity is an important indicator for investors and financial analysts for several reasons:

- Financial Health: A high TCE indicates that a company has a strong base of tangible assets, which can help it weather economic downturns and absorb losses.

- Risk Assessment: In industries like banking, a strong TCE ratio is crucial because it demonstrates the ability of a financial institution to withstand significant financial stress. A low TCE ratio, on the other hand, may signal higher financial risk.

- Creditworthiness: Lenders and creditors look at TCE as a measure of how much financial cushion a company has. The higher the TCE, the more secure the company is in its ability to repay debts.

- Investor Confidence: For investors, a strong TCE ratio can signal that the company is fundamentally sound and has solid assets that can be used to generate returns.

In some industries, particularly finance and banking, regulatory bodies require firms to maintain a minimum level of tangible common equity to ensure that they can absorb shocks from unexpected financial losses.

How to Interpret Tangible Common Equity?

The significance of TCE can vary depending on the industry. For example:

Banking and Finance: TCE is particularly important in these sectors as regulators often require banks to maintain a minimum TCE to ensure stability. A high TCE ratio can indicate that a bank has enough tangible equity to cover potential losses from bad loans or other financial risks.

Technology: In the technology sector, companies may have significant intangible assets such as patents, software, and intellectual property. For such companies, TCE may not be as critical because the value of their intangible assets plays a crucial role in their market value and growth potential.

Manufacturing and Retail: In traditional industries like manufacturing, where physical assets such as machinery and real estate are essential, TCE is a more relevant indicator. A high TCE suggests that a company is in a strong financial position with a solid base of physical assets.

By maintaining a strong TCE, companies can assure investors and creditors that they have the necessary capital to weather financial difficulties, making it an essential component of long-term financial planning.

Tangible Common Equity vs. Total Equity

While total equity represents the entire value of a company’s assets minus its liabilities, Tangible Common Equity focuses on only tangible assets and common shareholders’ equity. The primary difference is the exclusion of intangible assets, which are often harder to liquidate or assess accurately during financial crises. This makes TCE a more conservative and reliable metric, particularly when evaluating a company’s resilience in times of financial stress.

Here’s how the two compare:

- Total Equity: Includes all assets (tangible and intangible) minus liabilities.

- Tangible Common Equity (TCE): Excludes intangible assets such as goodwill, patents, and trademarks.

The exclusion of intangibles helps ensure that the equity being measured can be converted to cash or liquidated in the event of a financial downturn. For example, if a company were to liquidate its assets, tangible assets like property and cash would be the first to be used to settle debts, not intangible assets like brand value or intellectual property.

Tangible Common Equity and Valuation

Tangible Common Equity plays a significant role in the valuation of companies, especially those in distress or at risk of bankruptcy. In situations where a company is being evaluated for acquisition or liquidation, tangible common equity provides a more realistic estimate of its actual worth.

This is particularly important for investors who focus on value investing or distressed asset acquisition, as TCE helps them determine whether the company’s stock is undervalued based on its real, tangible assets.

Tangible Common Equity Ratio

The Tangible Common Equity Ratio (TCE ratio) is a metric used to evaluate the relative strength of a company’s tangible equity. It is calculated by dividing Tangible Common Equity by the total assets of the company:

TCE Ratio = Tangible Common Equity / Total Assets

For example, if a company has $400 million in Tangible Common Equity and $2 billion in total assets, the TCE ratio would be:

TCE Ratio = 400 million / 2 billion = 0.2 or 20%

A higher TCE ratio typically suggests a lower risk of insolvency, as the company’s tangible equity covers a larger portion of its total assets. Conversely, a low TCE ratio may indicate a higher reliance on debt or intangible assets, which could expose the company to greater financial risk.

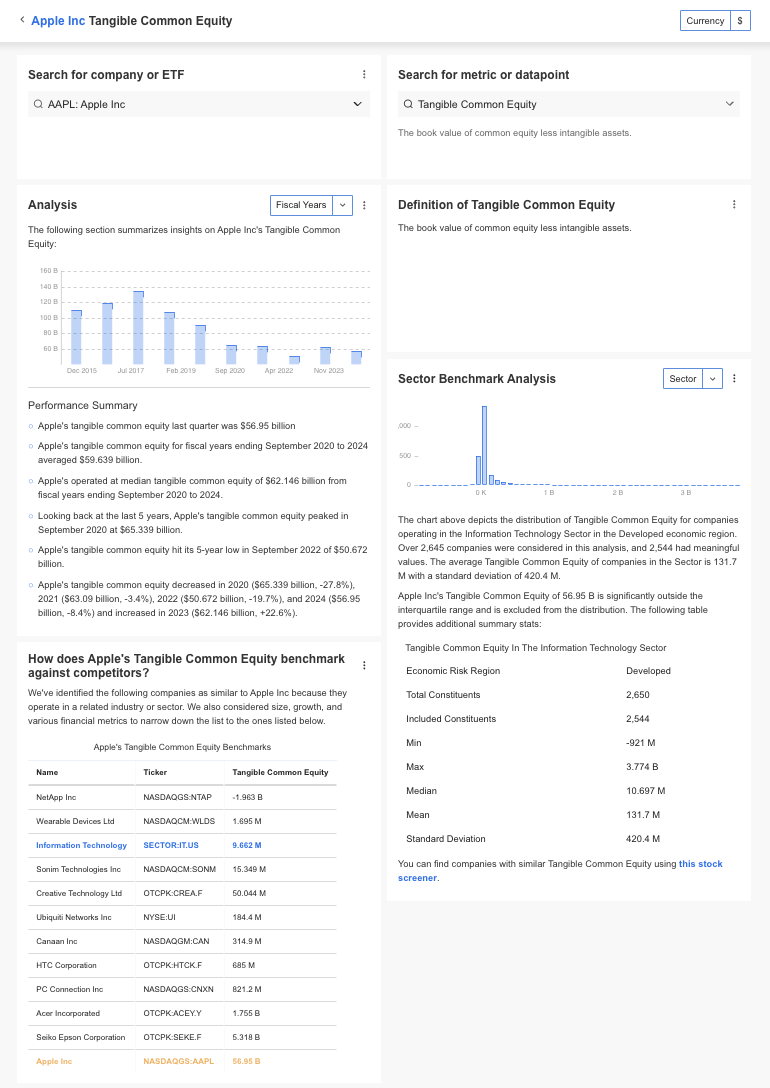

How to Find Tangible Common Equity?

InvestingPro offers detailed insights into companies’ Tangible Common Equity including sector benchmarks and competitor analysis.

InvestingPro: Access Tangible Common Equity Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to TCE data within the InvestingPro platform

🛠 Access to 1200+ additional fundamental metrics

🔍 Competitor comparison tools

📊 Evaluate stocks with 14+ proven financial models

Tangible Common Equity FAQs

What is the difference between Tangible Common Equity and Total Equity?

Total Equity includes both tangible and intangible assets, while Tangible Common Equity excludes intangible assets like goodwill and intellectual property, focusing solely on physical assets.

Why is Tangible Common Equity important?

It helps measure the financial stability of a company, offering a clearer view of its ability to withstand financial challenges, especially in sectors where tangible assets are crucial.

What is a good Tangible Common Equity ratio?

A higher TCE ratio indicates a more financially stable company. However, what is considered “good” varies by industry. A ratio of 10-20% is often seen as strong in many sectors.

How is TCE used in banking?

In banking, a strong TCE ratio is required to ensure that the bank can absorb losses and protect depositors. Regulators often require banks to maintain a minimum TCE ratio to ensure financial stability.