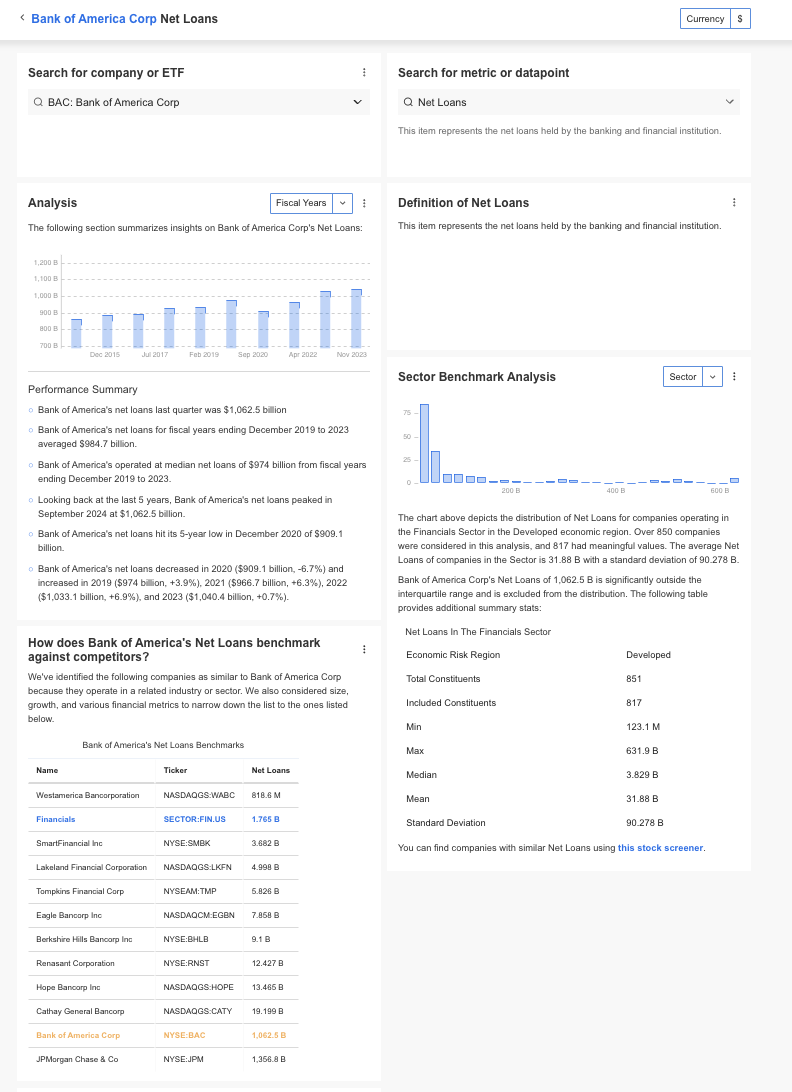

What are Net Loans?

Net loans refer to the total value of loans a company or financial institution has issued, minus any provisions for loan losses, reserves, or allowances. These figures represent the actual amount of money that is expected to be repaid, reflecting the institution’s loan portfolio after accounting for potential defaults or non-performing loans.

In simpler terms, net loans represent the “net” amount of loans that a bank or lender expects to collect after factoring in the risk of defaults or unpaid debts. For financial institutions like banks, these loans are a key component of their balance sheet, often forming the bulk of their assets.

How to Calculate Net Loans?

The formula for calculating net loans is quite simple:

Net Loans = Gross Loans – Loan Loss Reserves

In this formula,

- Gross Loans: The total amount of loans issued by the bank or financial institution, without considering potential defaults or non-performing loans.

- Loan Loss Reserves: Funds set aside by the financial institution to cover potential loan defaults. These reserves are created based on historical loan performance, anticipated risks, and the economic environment.

Example Calculation of Net Loans

Let’s consider a practical example. A bank has issued $1 billion in loans. However, it anticipates that $30 million of these loans may default based on its historical experience and current economic conditions. To prepare for this, the bank sets aside a reserve of $30 million.

As per the information provided here:

- Gross Loans: $1,000,000,000

- Loan Loss Reserves: $30,000,000

The loan loss reserves are determined based on the bank’s analysis of the loan portfolio’s risk profile, including non-performing loans and potential defaults. These reserves help ensure that the bank is financially prepared for any defaults or unexpected losses in the loan portfolio.

Applying the formula for Net Loans

Net Loans = Gross Loans – Loan Loss Reserves

Net Loans = $1,000,000,000 – $30,000,000 = $970,000,000

So, the bank’s net loans would be $970 million. This represents the amount of loans the bank expects to collect after accounting for potential losses.

Why Are Net Loans Important?

Net loans are a critical metric for assessing the health of a financial institution and its ability to manage risk effectively. They provide a clearer picture of the loan portfolio’s value by accounting for potential losses. This metric helps investors, analysts, and the bank itself to assess the true financial condition of the lending business.

Understanding the metric is crucial for several reasons:

Risk Management

Net loans are essential for evaluating the level of risk associated with the bank’s lending operations. The amount of loan loss reserves set aside gives insight into how well the bank is preparing for potential defaults. A higher reserve indicates greater perceived risk, while a lower reserve may suggest more confidence in the loan portfolio’s performance.

Financial Health of the Institution

A bank’s net loans help determine its financial health by showing how much of its lending activity is at risk. A significant difference between gross loans and net loans may indicate a higher likelihood of defaults, which could strain the bank’s finances. Conversely, a smaller gap suggests better loan quality and lower risk exposure.

Creditworthiness Evaluation

For investors and stakeholders, net loans are an important factor in assessing the institution’s creditworthiness. A high level of non-performing loans or a large loan loss reserve can signal financial instability, while strong net loans suggest sound lending practices and good credit risk management. These indicators influence investor confidence and the bank’s ability to secure financing.

Impact on Profitability

Net loans directly impact a bank’s profitability. Banks generate revenue from the interest charged on loans, and the more loans they expect to collect (i.e., the higher the net loans), the higher their potential earnings. Reductions in net loans due to loan losses or increased reserves can signal declining profitability, affecting stock prices and investor sentiment.

True Representation of Loan Portfolio

Net loans reflect the actual value of a financial institution’s loan portfolio after accounting for potential losses. By subtracting loan loss reserves from gross loans, net loans provide a more accurate picture of the amount that is likely to be collected. This helps in understanding the real value of the bank’s lending activities.

How to Interpret Net Loans?

Net loans are important because they give a clearer picture of a financial institution’s loan portfolio’s health and its potential future income. A higher number of net loans could indicate a larger loan book and the potential for greater earnings, while a lower number may suggest that a bank is tightening lending or that it is dealing with higher loan losses.

Interpreting net loans involves analyzing their context and implications:

- Loan Loss Reserves: A high amount of loan loss reserves relative to gross loans may suggest that the institution is facing increased risk, possibly due to economic downturns, or has a conservative approach toward loan defaults. Conversely, low reserves may indicate optimism or underestimation of risks.

- Growth Trends: A growing net loan balance typically indicates that a bank or financial institution is successfully expanding its lending activities, which could lead to higher interest income. However, rapid growth without adequate risk management could signal potential issues with loan quality.

- Loan Portfolio Composition: Understanding the types of loans included in the net loans figure is essential. For instance, loans to high-risk borrowers, such as subprime borrowers, could lead to higher defaults, even if the gross loan number is large. The quality of loans plays a key role in interpreting the net loans figure.

- Economic Environment: During periods of economic uncertainty or downturns, net loans may decrease as financial institutions become more cautious in their lending practices. In such cases, an increase in loan loss reserves may be a prudent response to potential defaults.

What is a Good Net Loan?

A good net loans figure is one that reflects a strong, growing loan portfolio, while also factoring in sufficient reserves for potential defaults. Here’s what to look for:

- Healthy Growth: A good net loans number should show steady growth in lending activities, indicating the bank’s successful strategy in issuing loans and expanding its business.

- Proportional Loan Loss Reserves: A good net loans figure will have an appropriate balance of loan loss reserves, ensuring that the institution is prepared for potential defaults while not overestimating risks.

- Low Default Rates: A low level of non-performing loans, relative to gross loans, is a sign of good loan quality. This means the bank is managing credit risk well and minimizing defaults.

- Risk Management: A well-managed financial institution will have the right amount of reserves based on its risk profile, industry conditions, and loan portfolio composition.

What are the Limitations of Net Loans?

While net loans can provide valuable insights into a company’s efforts to improve its operations, there are several limitations to consider:

- Overly Optimistic Reserves: If a bank or financial institution is overly optimistic about the recovery of bad debts, the loan loss reserves may be understated, leading to an inflated net loans figure. This can mislead investors about the true value of the loan portfolio.

- Changing Economic Conditions: Economic downturns or changes in market conditions can significantly affect loan defaults, leading to unexpected increases in loan loss reserves. This could result in a sharp reduction in net loans, even if the institution’s overall loan portfolio appears healthy.

- Different Accounting Methods: Financial institutions may have different methods for calculating and reporting net loans. For instance, some may use different criteria for determining which loans are considered non-performing, affecting the loan loss reserves and, subsequently, the net loans figure.

- Excludes Non-Performing Loans: While net loans account for loan loss reserves, they may not fully reflect the true risk of a loan portfolio. Financial institutions might still have a large volume of non-performing loans that are not fully accounted for in the net loans figure.

How to Find Net Loans?

InvestingPro offers detailed insights into companies’ Net Loans including sector benchmarks and competitor analysis.

InvestingPro+: Access Net Loans Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to Net Loans data within the InvestingPro platform

🛠 Access to 1200+ additional fundamental metrics

🔍 Competitor comparison tools

📊 Evaluate stocks with 14+ proven financial models

Net Loans FAQ

What is the difference between net loans and gross loans?

Gross loans represent the total amount of loans issued by a financial institution, while net loans account for the amount expected to be repaid, minus reserves for potential loan losses.

Are net loans the same as loan portfolios?

No, net loans refer specifically to loans after adjusting for loan loss reserves, whereas a loan portfolio includes all loans issued, including those that may not be fully collectible.

How does an increase in loan loss reserves affect net loans?

An increase in loan loss reserves reduces the net loans figure, reflecting the institution’s cautious approach to potential defaults and ensuring it is financially prepared for losses.

Why do net loans matter for investors?

Net loans are a key indicator of a bank’s financial health, asset quality, and future earning potential. Investors use this metric to assess risk and profitability.

Can net loans decrease even if gross loans are increasing?

Yes, if a financial institution increases its loan loss reserves due to anticipated defaults, net loans can decrease even if gross loans are growing.