What Is Interest Capitalized?

Interest Capitalized is interest incurred on funds borrowed for the development or construction of a long-term asset. Instead of recording this interest as an expense immediately, it is added to the asset’s total value on the balance sheet, where it becomes part of the asset’s cost basis. This interest capitalization continues during the construction or development phase and ends once the asset is ready for its intended use.

Capitalizing interest is common in sectors like real estate, where companies often borrow substantial sums for projects that will not yield immediate income. By capitalizing these interest payments, companies can present more favorable short-term profit figures, which can enhance financial metrics such as net income and EBITDA.

How to Calculate Interest Capitalized?

The calculation of capitalized interest depends on the amount borrowed, the interest rate on the loan, and the duration of the construction period. The formula for calculating capitalized interest is:

Capitalized Interest = Average Expenditures × Interest Rate × Construction Period

Capitalizing interest is an accounting practice that recognizes interest payments as part of the asset’s acquisition cost, allowing companies to delay expensing these costs until the asset generates income.

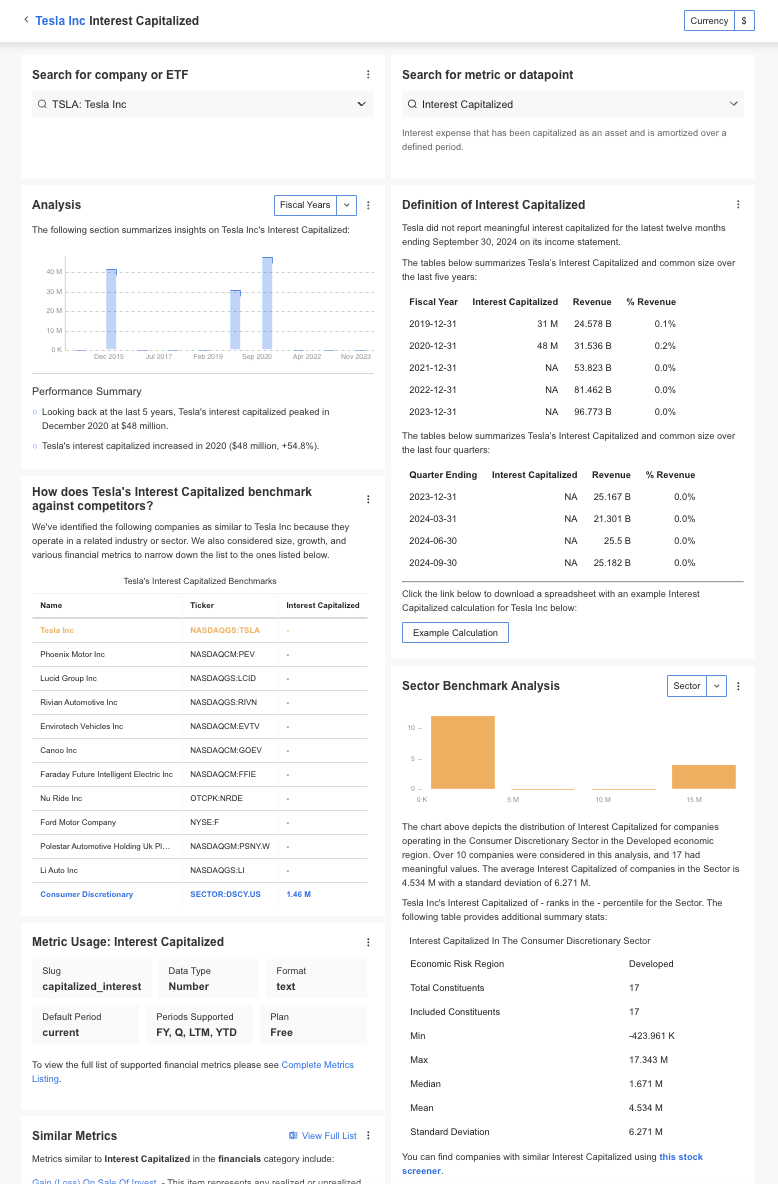

Example Calculation of Capitalized Interest

Let’s assume a company takes out a loan of $10 million at an annual interest rate of 5% to fund a new factory’s construction, which will take two years to complete.

- Determine Average Expenditures: For simplicity, if expenditures are evenly distributed over the construction period, the average expenditure might be $5 million.

- Calculate Annual Interest: Multiply the average expenditures by the interest rate:

Annual Interest = 5% × 5,000,000 = 250,000

- Multiply by Construction Period: Since the project spans two years, multiply the annual interest by 2:

Capitalized Interest = 250,000 × 2 = 500,000

Thus, the capitalized interest over the two-year construction period would be $500,000, which is added to the asset’s cost basis on the balance sheet rather than recorded as an expense.

Why is Interest Capitalized Important?

Interest Capitalized is critical because it directly impacts a company’s profitability and cash flow. Since Interest Capitalized is recorded as part of the asset’s cost rather than as an immediate expense, it allows companies to avoid reporting interest costs on their income statement during the asset’s construction period.

Commonly used in corporate finance, real estate development, and large-scale construction projects, it represents interest expenses that are added to the cost basis of a long-term asset rather than expensed immediately. This practice improves a company’s short-term profitability, particularly in industries where long-term projects are financed over multiple years.

For investors, understanding Interest Capitalized provides insights into the company’s financial strategy, especially when evaluating profitability, debt management, and the real costs associated with large projects.

Advantages of Interest Capitalized

Understanding Interest Capitalized is essential for anyone involved in financial planning, investing, or managing capital-intensive projects. This approach allows companies to accurately reflect the cost of building long-term assets without immediately impacting profit, giving a clearer view of a company’s short-term profitability.

- Increases Short-Term Profitability: By not expending interest immediately, Interest Capitalized can improve reported net income during the construction phase.

- Boosts Asset Value: Capitalizing interest adds to the asset’s value on the balance sheet, which can potentially increase the company’s asset-to-liability ratio.

- Tax Advantages: Delaying interest expense recognition can defer tax liabilities, providing additional cash flow during the construction period.

Limitations of Interest Capitalized

While Interest Capitalized offers numerous benefits, it also requires careful consideration to ensure accurate financial analysis. As with any financial decision, understanding its potential drawbacks is essential for making informed investment and management choices.

- Deferred Expenses: Although Interest Capitalized boosts short-term profitability, the cost will be recognized over time as depreciation or amortization, impacting future income statements.

- Complexity in Financial Analysis: Interest Capitalized can make it challenging for investors to accurately assess a company’s debt servicing ability, especially in sectors with significant capital expenditure.

- Potential for Overstated Assets: Adding interest to an asset’s value may result in overstated asset values on the balance sheet, especially if the project is not as profitable as expected.

Accounting Standards for Interest Capitalized

Accounting standards provide strict guidelines on how and when interest can be capitalized. For instance, under the Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS), interest can only be capitalized on assets that are being developed for future productive use. Routine maintenance or repairs typically do not qualify for interest capitalization.

The capitalization period begins when three conditions are met:

- Expenditures for the asset are being incurred.

- Interest costs are being incurred.

- Construction activities are in progress.

The capitalization period ends once the asset is substantially ready for use, at which point the interest expense is no longer capitalized but instead recorded as an expense on the income statement.

How to Find Interest Capitalized?

InvestingPro offers detailed insights into companies’ Interest Capitalized including sector benchmarks and competitor analysis.

InvestingPro: Access Interest Capitalized Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to Interest Capitalized data within the InvestingPro platform

🛠 Access to 1200+ additional fundamental metrics

🔍 Competitor comparison tools

📊 Evaluate stocks with 14+ proven financial models

Interest Capitalized FAQs

What is Interest Capitalized?

Interest Capitalized refers to the interest incurred on funds borrowed for the construction or acquisition of long-term assets, which is added to the asset’s value rather than expensed immediately.

Why is interest capitalized?

Capitalizing interest defers the recognition of the cost until the asset begins generating revenue, thereby improving short-term profitability and providing a more accurate representation of the asset’s true cost.

When does the capitalization of interest end?

The capitalization period typically ends when the asset is substantially complete and ready for its intended use.

How does Interest Capitalized affect taxes?

Since Interest Capitalized is not expensed immediately, it can defer tax liabilities, which may improve cash flow during the asset’s construction phase.

Are there any restrictions on capitalizing interest?

Yes, only interest incurred during the active development of a long-term asset qualifies for capitalization. Maintenance costs or improvements on completed assets generally do not qualify.

Does capitalized interest increase the asset’s value?

Yes, capitalized interest adds to the cost basis of the asset on the balance sheet, which can impact depreciation and amortization in future financial periods.