What Is Income Tax Expense?

Income tax expense is a critical component of a company’s financial statements, reflecting the taxes a business owes based on its taxable income for a specific period. It represents the total amount of taxes a company incurs due to its income-generating activities during a financial period.

Unlike other expenses, it is tied directly to the company’s profitability and tax regulations, making it an essential metric for assessing financial health and operational efficiency.

How to Calculate Income Tax Expense?

It is calculated based on the applicable corporate tax rate and taxable income, which may differ from accounting profit due to temporary and permanent tax differences.

The calculation of income tax expense can be summarized using the following formula:

Income Tax Expense = (Taxable Income × Tax Rate) + Deferred Tax Expense / Benefit

Here,

- Taxable Income: The portion of a company’s income subject to taxation, which is derived after applying tax laws and deductions.

- Tax Rate: The applicable corporate tax rate, which varies based on jurisdiction and company size.

- Deferred Tax Expense/Benefit: The impact of temporary differences between accounting income and taxable income that result in taxes being paid or saved in future periods.

Example Calculation of Income Tax Expense

Let’s assume a company, ABC Corp, has the following financial details:

- Pre-Tax Accounting Income: $2,500,000

- Tax Deductions:

- Depreciation expense: $100,000

- Interest expense on loans: $50,000

- Other tax-deductible expenses: $30,000

- Taxable Income = Pre-Tax Accounting Income – Deductions

- Deferred Tax Expense: $50,000

Step 1: Determine the Company’s Taxable Income

Taxable Income = 2,500,000 – (100,000+50,000+30,000)

Taxable Income = 2,500,000−180,000=2,320,000

Thus, the Taxable Income for ABC Corp is $2,320,000.

Step 2: Apply the Applicable Tax Rate

The next step is to apply the relevant corporate tax rate to the taxable income. Corporate tax rates may vary by jurisdiction and company size, but for this example, let’s assume the following:

- Tax Rate: 25%

Calculation:

Income Tax Expense = Taxable Income × Tax Rate = 2,320,000 × 25% = 580,000

So, based on the taxable income of $2,320,000, ABC Corp’s Income Tax Expense is $580,000.

Step 3: Account for Deferred Tax Expense or Benefit

Adjusting for Deferred Tax:

Total Income Tax Expense = Current Income Tax Expense + Deferred Tax Expense

Total Income Tax Expense = 580,000 + 50,000 = 630,000

Thus, ABC Corp’s total income tax expense for the period is $630,000, which includes the current tax expense and the deferred tax expense.

Why is Income Tax Expense Important?

Income Tax Expense is a critical metric for understanding a company’s tax obligations, profitability, and financial health. By analyzing income tax expense in relation to pre-tax income, effective tax rates, deferred taxes, and trends over time, investors can gain valuable insights into a company’s tax strategies and long-term financial performance.

It provides critical insights for various stakeholders:

For Investors:

- Highlights the impact of tax obligations on profitability.

- Helps in evaluating a company’s efficiency in tax planning.

For Companies:

- Reflects compliance with tax regulations.

- Influences strategic decisions, such as reinvestments or cost management.

For Analysts:

- Serves as a key input in metrics like net income and earnings per share (EPS).

- Helps identify discrepancies between accounting and taxable income, offering insights into deferred tax assets or liabilities.

Factors Affecting Income Tax Expense

Several factors influence a company’s income tax expense:

- Taxable Income: Higher taxable income typically results in higher tax expenses.

- Tax Rate: Changes in corporate tax rates, due to government policy, directly affect tax expenses.

- Deductions and Credits: Tax deductions, credits, and incentives reduce the overall taxable income, thereby lowering tax expenses.

- Deferred Tax Items: Temporary differences, such as accelerated depreciation or loss carryforwards, impact deferred tax calculations.

- International Operations: Companies operating in multiple jurisdictions may face varying tax rates and regulations, affecting consolidated tax expenses.

How Does Income Tax Expense Appear on Financial Statements?

Income tax expense is recorded on the income statement, typically after operating expenses and before net income. It directly impacts the company’s net income, showcasing the financial burden of taxes on the organization’s profitability.

It is a key component in the calculation of net profit:

Net Income = Pre-Tax Income − Income Tax Expense

For companies with multiple jurisdictions or complex operations, income tax disclosures in the financial statements often include:

- A breakdown of current and deferred taxes.

- Reconciliation of effective tax rate vs. statutory tax rate.

Income Tax Expense vs. Income Tax Payable

Though related, income tax expense and income tax payable are distinct concepts:

Income Tax Expense:

- Represents the total tax cost for a period, including current and deferred taxes.

- Appears on the income statement.

Income Tax Payable:

- Refers to the actual tax liability owed to the government.

- Reported as a current liability on the balance sheet.

For example, if a company has a tax expense of $300,000 but has already paid $100,000 in advance, the income tax payable will be $200,000.

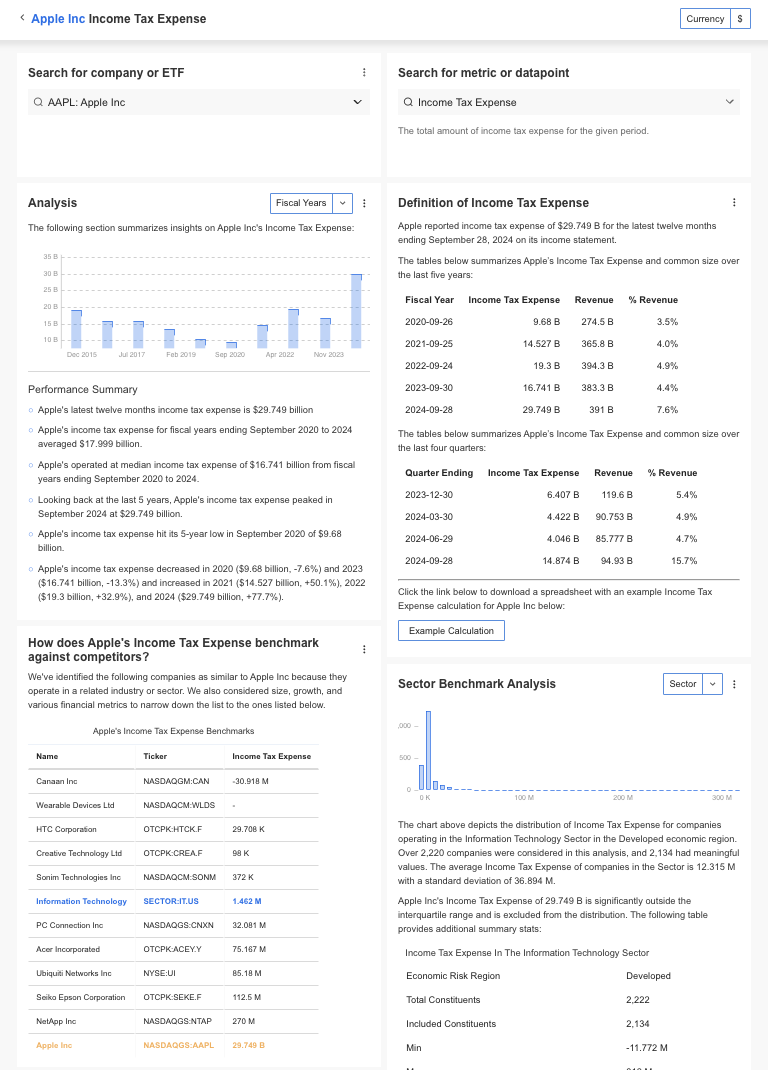

How to Find Income Tax Expense?

InvestingPro offers detailed insights into companies’ Income Tax Expense including sector benchmarks and competitor analysis.

InvestingPro: Access Income Tax Expense Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to Income Tax Expense data within the InvestingPro platform

🛠 Access to 1200+ additional fundamental metrics

🔍 Competitor comparison tools

📊 Evaluate stocks with 14+ proven financial models

Income Tax Expense FAQs

How does income tax expense differ from income tax payable?

Income tax expense reflects the total tax incurred for the period, including deferred taxes, while income tax payable represents the current tax owed to the government.

Can an income tax expense be negative?

Yes, a negative income tax expense indicates a tax benefit, often arising from operating losses or deferred tax assets.

Why does taxable income differ from accounting income?

Taxable income differs due to temporary or permanent differences, such as depreciation methods, tax credits, or non-deductible expenses.

What is deferred income tax?

Deferred income tax represents the tax impact of temporary differences that will reverse in future periods, leading to future tax liabilities or assets.

Does income tax expense affect cash flow?

While income tax expense impacts net income, it does not directly affect cash flow unless taxes are paid during the same period.