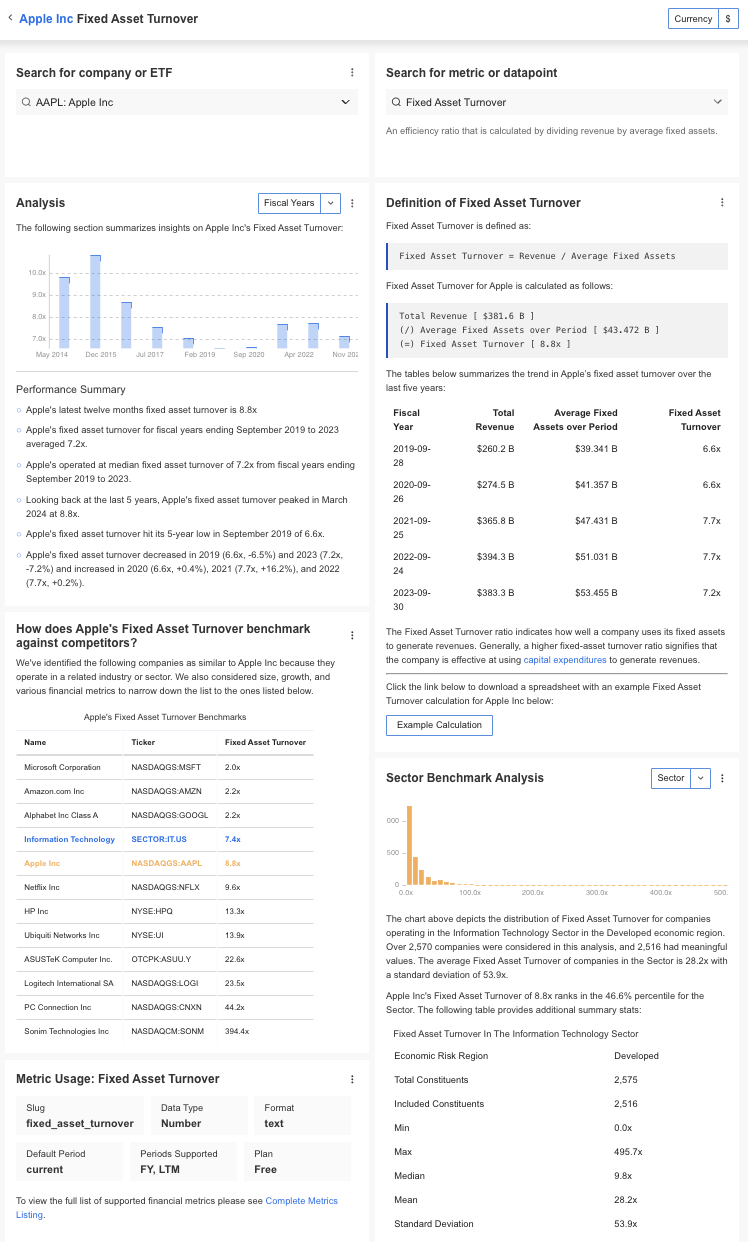

What Is Fixed Asset Turnover?

Fixed Asset Turnover (FAT) is a financial ratio that measures a company’s ability to generate net sales from its investment in fixed assets. Fixed assets typically include property, plant, and equipment (PP&E). This ratio provides insight into how efficiently a company is utilizing its fixed assets to produce revenue.

How to Calculate Fixed Asset Turnover?

The formula to calculate Fixed Asset Turnover is:

Fixed Asset Turnover = Net Sales / Average Net Fixed Assets

Where:

- Net Sales: The total revenue from goods and services sold, minus returns, allowances, and discounts.

- Average Net Fixed Assets: The average value of the fixed assets at the beginning and end of the period.

Why is Fixed Asset Turnover Important?

Fixed Asset Turnover is a crucial metric for understanding how well a company uses its fixed assets to drive revenue. It provides valuable insights for investors, analysts, and management, helping to gauge operational efficiency and inform strategic decisions.

Efficiency Indicator: This ratio is a key indicator of a company’s operational efficiency. A higher FAT suggests that the company is effectively using its fixed assets to generate sales, whereas a lower FAT indicates potential inefficiencies.

Investment Decisions: Investors and analysts use this ratio to assess the productivity of a company’s fixed assets, which can influence investment decisions.

Benchmarking: Comparing FAT across companies in the same industry helps identify which firms are managing their assets more effectively.

How to Interpret Fixed Asset Turnover?

A higher FAT ratio indicates that a company is effectively utilizing its fixed assets to generate sales, showcasing management’s efficiency in asset utilization.

When interpreting the FAT ratio, consider the following:

Comparative Analysis: Always compare the ratio against the company’s historical performance and industry standards to gauge efficiency accurately.

Sector Suitability: Ensure that the company operates in a sector where the FAT ratio is a relevant measure before relying heavily on it.

Holistic View: Remember that while a high FAT ratio indicates efficient asset use, it does not provide a complete picture of profitability or cash flow generation. Other financial metrics should also be considered for a comprehensive analysis.

Factors Influencing Fixed Asset Turnover

The major factors that can influence a company’s Fixed Asset Turnover include:

Industry Type: Capital-intensive industries, such as manufacturing, typically have lower FAT ratios compared to service-oriented industries.

Asset Age and Condition: Older, fully depreciated assets may result in a higher FAT ratio, while newer assets might lower the ratio temporarily due to higher book values.

Revenue Trends: Significant changes in revenue without a corresponding change in fixed assets will affect the FAT ratio.

Limitations of Fixed Asset Turnover

Fixed Asset Turnover is a widely used financial ratio; however, like all financial metrics, it comes with its set of limitations, which investors and analysts must consider for a comprehensive analysis.

Cyclical Sales and Periodic Fluctuations

One significant limitation is its sensitivity to cyclical sales. Companies with seasonal or cyclical sales patterns may show worse ratios during slow periods. Therefore, it’s crucial to examine the ratio over multiple time periods to get an accurate picture of performance across different market conditions.

Impact of Outsourcing and Operational Strategies

Management strategies such as outsourcing production can skew the FAT ratio. By outsourcing, a company might reduce its reliance on fixed assets, thereby improving its FAT ratio. However, this does not necessarily mean the company is performing well overall. Outsourcing could mask underlying issues such as unstable cash flows or weak business fundamentals.

Disconnect Between Sales and Profitability

A high FAT ratio does not guarantee profitability. While it indicates efficient use of fixed assets to generate sales, it says nothing about the company’s ability to generate solid profits or maintain healthy cash flows.

Comparative Tool Limitations

The FAT ratio is most useful as a comparative tool. Its true value emerges when compared over time within the same company or against competitors in the same industry. However, differences in the age and quality of fixed assets can make cross-company comparisons challenging. Older, fully depreciated assets may result in a higher ratio, potentially giving a misleading impression of efficiency.

Exclusion of Working Capital

The FAT ratio excludes investments in working capital, such as inventory and cash, which are necessary to support sales. This exclusion is intentional to focus on fixed assets, but it means that the ratio does not provide a complete picture of all the resources a company uses to generate revenue.

How to Find Fixed Asset Turnover?

InvestingPro offers detailed insights into companies’ Fixed Asset Turnover including sector benchmarks and competitor analysis.

InvestingPro: Access Fixed Asset Turnover Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to FAT data within the InvestingPro platform

✓ Access to 1200+ additional fundamental metrics

✓ Competitor comparison tools

✓ Evaluate stocks with 14+ proven financial models

FAQ

What does a high Fixed Asset Turnover ratio indicate?

A high ratio indicates that a company is effectively using its fixed assets to generate sales, reflecting operational efficiency.

Can a very high Fixed Asset Turnover ratio be a bad sign?

Yes, it could indicate underinvestment in fixed assets, which might lead to future capacity issues or inability to meet demand.

How does Fixed Asset Turnover vary between industries?

It varies significantly; capital-intensive industries usually have lower ratios, while service-oriented industries typically have higher ratios due to lower fixed asset investments.

How can a company improve its Fixed Asset Turnover ratio?

Companies can improve this ratio by increasing sales without a proportionate increase in fixed assets or by efficiently managing and utilizing their existing assets.