What is the Equity Method?

The equity method of investment is a method used by companies to account for investments in other companies where they hold significant influence, but not full control. Typically, this is applied when a company owns between 20% and 50% of another company’s voting stock, which gives it the ability to influence the decisions of the other company without having outright control.

Unlike full consolidation or cost-based methods, the equity method recognizes the investor’s share of the investee’s net income or losses directly in its financial statements.

How to Calculate Equity Method Investments?

To calculate the investment’s carrying amount under the equity method, the following steps are taken:

Carrying Value of Investment = Initial Cost of Investment + Share of Investee’s Profits or Losses − Dividends Received + Share of Other Comprehensive Income

This calculation ensures the investment account reflects the investor’s proportionate ownership stake and the changes in the investee’s net assets.

Example Calculation of Equity Method Investment

Let’s take a look at a simplified example of how the equity method is applied in practice:

To illustrate, consider the following scenario involving XYZ Corp and ABC Ltd.

Details:

- XYZ Corp acquires a 30% stake in ABC Ltd for $500,000.

- ABC Ltd reports net income of $200,000 for the year.

- ABC Ltd declares and pays $50,000 in dividends during the same period.

Step-by-Step Calculation:

- Initial Investment: The starting investment value is the acquisition cost:

Initial Investment = $500,000

- Share of Net Income: XYZ Corp’s share of ABC Ltd’s income is 30% of $200,000:

Share of Net Income = 0.30 × 200,000 = $60,000

- Adjusting for Dividends: XYZ Corp’s share of dividends is 30% of $50,000:

Dividends Received = 0.30 × 50,000 = $15,000

- Revised Investment Value: Incorporate the adjustments:

Investment Value=500,000+60,000−15,000=$545,000

Result: XYZ Corp’s investment in ABC Ltd now carries a value of $545,000.

Why is Equity Method Investment Important?

Under the equity method, the investor company recognizes its share of the investee’s profits or losses in its own financial statements. This means that the carrying amount of the investment is adjusted periodically to reflect the investor’s share of any earnings or losses made by the investee.

The equity method differs from other methods of accounting for investments, such as the cost method and the consolidation method, in that it recognizes the investor’s share of the investee’s financial performance and adjusts the carrying value of the investment accordingly.

When is the Equity Method Applied?

The equity method is typically applied in situations where an investor has significant influence over the investee, which is generally indicated by the investor owning between 20% and 50% of the voting shares of the investee. However, this percentage can vary depending on the specific circumstances, such as the presence of other factors like board representation, contractual agreements, or other methods of exercising influence.

Criteria for Significant Influence

Companies are considered to have significant influence when they:

- Own 20% to 50% of voting shares.

- Have representation on the investee’s board of directors.

- Participate in policy-making processes.

It is important to note that owning 20% of a company doesn’t automatically mean the equity method must be applied. Factors such as the investor’s ability to make significant decisions about the investee’s operations, its ability to participate in policy decisions, or influence financial and operating decisions also play a role in determining whether significant influence exists.

Conversely, it could be used with less than 20% ownership if significant influence exists.

How Does the Equity Method Work?

Recognizing Initial Investment

When an entity acquires a significant stake in another company, it records the initial investment on the balance sheet at cost. This figure reflects the purchase price of the shares.

Under the equity method, the investor adjusts the investment account based on its proportionate share of the investee’s net income or loss. For instance:

- If the investee earns a profit, the investor’s investment value increases.

- If the investee incurs a loss, the investment value decreases.

Receiving Dividends

Dividends received from the investee reduce the investment account. Unlike cost-based methods, dividends are not recognized as income but are considered a return on investment.

Advantages of the Equity Method

Accurate Reflection of Ownership

The equity method provides a more accurate picture of an investor’s share in the economic performance of the investee. This is because it reflects both the company’s share of profits and losses as well as any dividends or distributions received.

Transparent Financial Reporting

Since the equity method reflects changes in the value of the investment due to the investee’s performance, it gives investors and analysts a clearer understanding of the financial health of the business relationship.

Recognition of Influence

It acknowledges that the investor has significant influence over the investee’s decisions, and therefore, its share in the investee’s financial activities is essential to understand the financial status of the investor company.

Limitations of Equity Method

Complexity in Application

The equity method can be complex to apply, especially when determining how much influence the investor has over the investee. Sometimes, this may involve judgment calls, particularly in cases where the ownership percentage is close to the threshold.

Changes in Ownership

If the investor’s stake increases or decreases, this can impact the application of the equity method. If the investor’s share increases to over 50%, the consolidation method may be more appropriate, while if it drops below 20%, the cost method may be used instead.

Difficulties in Accounting for Losses

In cases where the investee reports a loss, the investor’s share of the loss reduces the carrying amount of the investment. If the carrying value drops to zero, the investor may need to cease recognizing losses and instead only account for any additional investments or distributions from the investee.

How to Find Equity Method Investments?

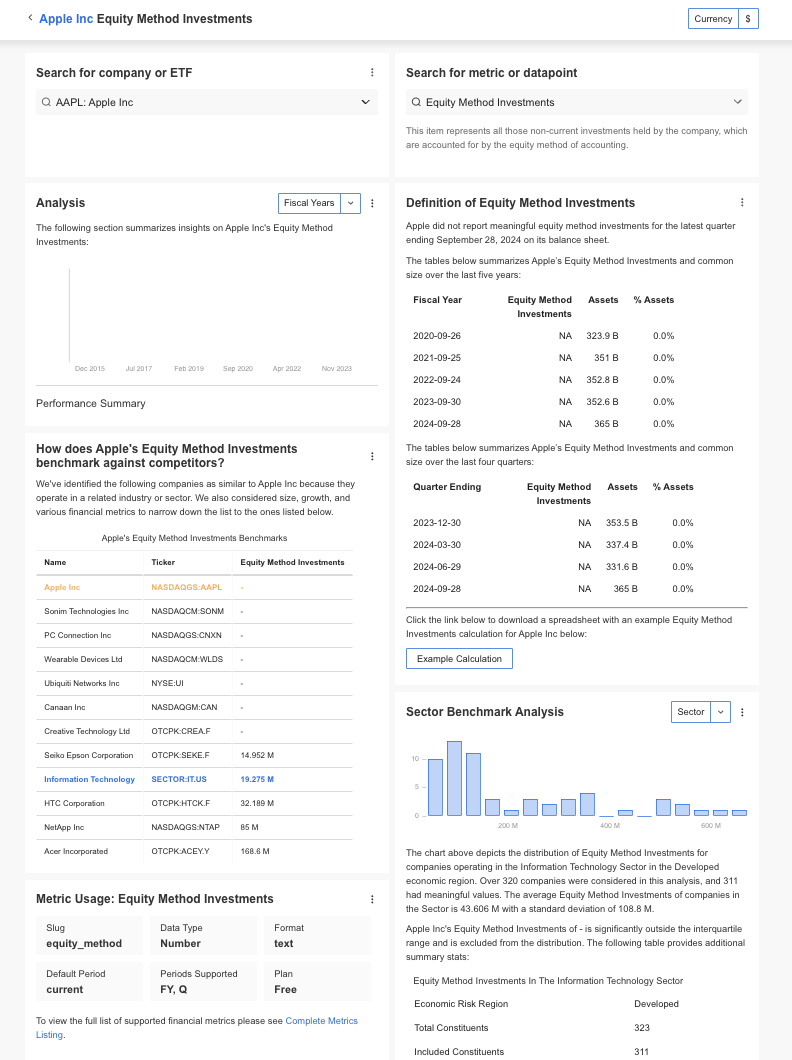

InvestingPro offers detailed insights into companies’ Equity Method Investments including sector benchmarks and competitor analysis.

InvestingPro: Access Equity Method Investments Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to Equity Method Investments data within the InvestingPro platform

🛠 Access to 1200+ additional fundamental metrics

🔍 Competitor comparison tools

📊 Evaluate stocks with 14+ proven financial models

Equity Method Investments FAQs

What is the difference between the equity method and consolidation?

The key difference lies in the level of control. Under the equity method, the investor has significant influence but not control. However, if the investor owns more than 50% of the investee, control exists, and the consolidation method is applied, combining both companies’ financial statements.

How is the equity method different from the cost method?

The cost method is applied when the investor does not have significant influence (i.e., owns less than 20% of the investee’s shares). Under the cost method, the investment is initially recorded at cost and only adjusted for dividends received or impairments, without recognizing the investee’s share of profits or losses.

Can the Investment Value Fall Below Zero?

If the investee’s cumulative losses exceed the investment value, the account can reach zero, and further losses are not recognized unless the investor has additional financial obligations.

Can the equity method be used for all investments?

No. It is only applicable when the investor has significant influence over the investee, typically when the ownership is between 20% and 50%. Investments outside this range are generally accounted for using other methods.

Are Dividends Always Deducted?

Yes, dividends reduce the investment account since they represent a return on the invested capital.