What is EPV?

Earnings Power Value (EPV) is a financial metric used to estimate the intrinsic value of a company based on its sustainable earnings. Developed by Bruce Greenwald, EPV focuses on the firm’s current earning potential, disregarding growth projections or speculative factors.

This method appeals to investors seeking to understand a company’s value under steady-state operations. By analyzing EPV, you can gain insights into whether a stock is overvalued or undervalued in the current market.

How to Calculate EPV?

The formula for Earnings Power Value is straightforward and relies on adjusted net operating profit after taxes (NOPAT) and the company’s weighted average cost of capital (WACC):

EPV = Adjusted NOPAT / WACC

In the formula,

- Adjusted NOPAT: Net operating profit after taxes, modified to exclude any non-recurring or extraordinary items that do not reflect the company’s ongoing operations.

- WACC (Weighted Average Cost of Capital): The company’s cost of capital, representing the required return for equity and debt holders.

This formula is instrumental in providing an objective measure of the company’s earnings capacity and its value from a purely operational perspective.

The formula for Earnings Power Value (EPV) is often simplified as:

EPV = Adjusted Earnings / WACC

Here,

- Adjusted Earnings typically refers to normalized net operating profit after taxes (NOPAT) or EBIT after tax, adjusted for non-recurring items.

- WACC (Weighted Average Cost of Capital) represents the discount rate that reflects the company’s cost of debt and equity.

However, the exact definition of ‘Adjusted Earnings’ can vary slightly depending on the source or methodology being used. For example:

- Some methodologies might use EBITDA, EBIT, or NOPAT.

- Others might further adjust these earnings to normalize for one-time events, cyclical fluctuations, or extraordinary items.

Example Calculation of EPV

Consider ABC Corp. is a manufacturing company. Here’s the relevant financial information:

- Earnings Before Interest and Taxes (EBIT): $15,000,000

- Tax Rate (t): 25%

- Non-Recurring Expenses (One-Time Legal Costs): $2,000,000

- Weighted Average Cost of Capital (WACC): 10%

Adjust EBIT

We start by adjusting EBIT for any non-recurring or extraordinary expenses. In this case, ABC Corp. incurred $2,000,000 in one-time legal costs, which are not part of its regular operations.

Adjusted EBIT = Reported EBIT + Non-Recurring Expenses

Adjusted EBIT = 15,000,000 + 2,000,000 = 17,000,000

Calculate After-Tax Adjusted EBIT

Since taxes impact earnings, we must calculate EBIT after tax (also referred to as NOPAT). This gives us the company’s normalized operational performance after accounting for taxes.

EBIT After Tax = Adjusted EBIT × (1−t)

EBIT After Tax = 17,000,000 × (1 − 0.25) = 17,000,000 × 0.75 = 12,750,000

Apply the EPV Formula

Using the EPV formula, we divide the after-tax adjusted earnings by the company’s WACC to determine its Earnings Power Value.

EPV = EBIT After Tax / WACC

EPV = 12,750,000 / 0.10 = 127,500,000

Interpretation of Results

- The Earnings Power Value (EPV) of ABC Corp. is $127,500,000.

- This value represents the intrinsic worth of the company if it maintains its current level of profitability indefinitely, with no assumptions for growth.

- If ABC Corp.’s market capitalization is less than $127,500,000, it may indicate that the company is undervalued, presenting a potential investment opportunity.

Why is EPV Important?

The Earnings Power Value (EPV) is an essential concept in financial analysis and valuation, offering investors and analysts a clear, growth-neutral measure of a company’s intrinsic value. Here’s why EPV is important:

Focus on Present Operational Efficiency

EPV exclusively evaluates a company’s current ability to generate sustainable earnings without relying on speculative growth assumptions. This approach allows investors to analyze the company’s core operations and profitability, excluding the influence of future projections or market hype.

Growth-Neutral Framework

Unlike valuation models such as discounted cash flow (DCF) that incorporate growth forecasts, EPV assumes no growth. This makes it particularly useful for:

- Mature or stable industries with predictable operations.

- Companies in volatile sectors where growth forecasts may be unreliable.

By removing growth expectations, EPV provides a conservative baseline for understanding value.

Provides a Baseline for Intrinsic Value

EPV establishes a company’s intrinsic worth by focusing on normalized, adjusted earnings. This baseline can serve as a reference point:

- To assess whether a stock is undervalued or overvalued relative to its market price.

- To complement other valuation methods, such as price-to-earnings (P/E) ratios or discounted cash flows.

Highlights Operational Resilience

Because EPV emphasizes normalized earnings, it reflects how well a company can sustain its performance under current conditions. This is particularly valuable during periods of economic uncertainty or when assessing companies with cyclical earnings.

Ideal for Risk-Averse Valuation

For conservative investors, EPV provides a reliable valuation tool that minimizes the risk of overestimating a company’s worth due to overly optimistic growth projections. This is particularly useful:

- When valuing companies in declining or slow-growth industries.

- For assessing businesses undergoing restructuring or turnaround efforts.

Application in Mergers and Acquisitions

EPV is a critical tool for determining the fair value of a target company in mergers and acquisitions (M&A). It helps buyers and sellers negotiate based on the company’s current earnings power rather than uncertain future potential.

How to Interpret EPV?

Interpreting Earnings Power Value (EPV) requires understanding how it reflects a company’s intrinsic value based on its current ability to generate sustainable earnings. Here’s how you can interpret EPV and what it indicates about a company’s financial health and market valuation:

EPV as a Baseline for Valuation

EPV provides an estimate of a company’s intrinsic value based solely on its present operating performance, excluding any assumptions about future growth. This gives you a clear picture of the company’s worth if it were to maintain its current earnings indefinitely, making it a useful baseline for comparing other valuation metrics.

- If EPV is higher than the company’s market capitalization: The stock may be undervalued, suggesting potential for price appreciation. It may be a buying opportunity if other factors support this conclusion.

- If EPV is lower than the company’s market capitalization: The stock may be overvalued, or it may indicate that the market is expecting significant growth or other positive developments that are not reflected in the current earnings.

Assessing Operational Efficiency

EPV is calculated based on a company’s adjusted earnings, which reflect its normalized operational performance after tax adjustments. Therefore, EPV highlights a company’s ability to generate consistent earnings from its core operations.

- A higher EPV indicates that the company is efficient at generating operating profits, relative to its cost of capital. A company with a high EPV has strong, stable operational performance and may be considered a well-managed business with an effective cost structure.

- A lower EPV suggests that the company’s profitability is weaker or that it is not efficiently using its capital to generate earnings. This could indicate potential operational inefficiencies or issues that need to be addressed.

Benchmarking Against Industry Peers

EPV can also be used to compare companies within the same industry or sector. By calculating the EPV for multiple companies, you can assess which ones are more efficiently generating earnings or which may be undervalued relative to their peers.

- A company with a higher EPV than its peers may indicate superior operational efficiency, better risk management, or a more favorable capital structure.

- A lower EPV compared to competitors could signal potential red flags, such as lower profitability, higher risk, or underperformance relative to industry standards.

What are the Limitations of EPV?

While EPV is a valuable tool, it is not without its constraints:

- Assumption of Stability: EPV assumes the company’s current earnings and capital structure are sustainable, which may not hold true in volatile industries.

- Exclusion of Growth Potential: By design, EPV does not account for future growth opportunities, which may lead to undervaluation of high-growth companies.

- Sensitivity to WACC and Adjustments: Small changes in WACC or errors in adjusting NOPAT can significantly affect the EPV outcome, underscoring the need for careful calculations.

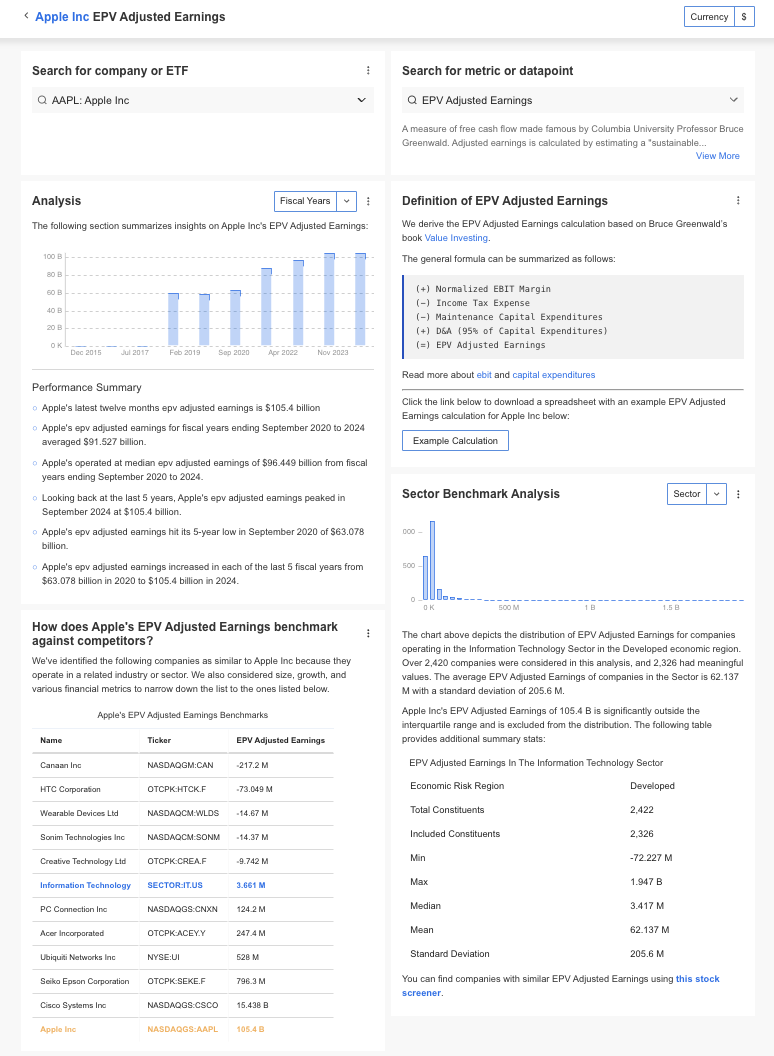

How to Find EPV Adjusted Earnings?

InvestingPro offers detailed insights into companies’ Earnings Power Value (EPV) Adjusted Earnings including sector benchmarks and competitor analysis.

InvestingPro: Access EPV Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to EPV data within the InvestingPro platform

🛠 Access to 1200+ additional fundamental metrics

🔍 Competitor comparison tools

📊 Evaluate stocks with 14+ proven financial models

EPV FAQs

How is EPV different from discounted cash flow (DCF) analysis?

EPV focuses solely on current earnings without considering future growth, while DCF incorporates projections of future cash flows and growth rates.

Can EPV be used for startups or high-growth companies?

EPV is less suitable for startups or high-growth companies due to its growth-neutral approach. These businesses often derive their value from anticipated future growth, which EPV does not account for.

Why is adjusted NOPAT important in EPV calculations?

Adjusted NOPAT ensures that the earnings used in the EPV formula accurately reflect the company’s recurring operational performance, free from anomalies or one-time events.

What role does WACC play in EPV?

WACC serves as the discount rate in the EPV formula, reflecting the company’s cost of capital and the expected returns of its investors.

Can EPV provide a definitive value for a company?

EPV provides an intrinsic value based on current earnings, but it should be used alongside other valuation methods for a comprehensive analysis.