What Is Depreciation & Amortization?

Depreciation and amortization are accounting methods used to allocate the cost of an asset over its useful life. They reflect how assets lose value over time due to usage, wear and tear, or obsolescence.

While depreciation applies to tangible assets, such as machinery, buildings, or vehicles, amortization applies to intangible assets, like patents, copyrights, or trademarks.

How to Calculate Depreciation & Amortization?

There are several methods to calculate depreciation and amortization. Below are the most common approaches:

Straight-Line Method

The simplest and most widely used method. It assumes the asset loses value evenly over its useful life.

Annual Depreciation / Amortization = (Cost of Asset − Salvage Value) / Useful Life

Declining Balance Method

This method accelerates depreciation, assuming the asset loses more value in the early years.

Depreciation Expense = Book Value at Beginning of Year × Depreciation Rate

Units of Production Method

This method calculates depreciation based on usage or output rather than time.

Depreciation Per Unit = (Cost of Asset − Salvage Value) / Total Estimated Units of Production

Example Calculation of Depreciation & Amortization

Depreciation Example

A company purchases a delivery van for $30,000. The van has an expected useful life of 5 years and a salvage value of $5,000 at the end of its life. Using the straight-line method:

Annual Depreciation = (Cost of Asset − Salvage Value) / Useful Life

Annual Depreciation = (30,000 – 5,000) / 10 = 5,000 per year

This means the company will record a depreciation expense of $5,000 annually for five years, reflecting the van’s diminishing value over time.

Amortization Example

A company acquires a patent for $15,000, which is expected to have a useful life of 10 years. Using the straight-line method:

Annual Amortization = Cost of Intangible Asset / Useful Life

Annual Amortization = 15,000/10 = 1,500 per year

The company will record an amortization expense of $1,500 annually for 10 years to account for the declining value of the patent.

Combined Depreciation and Amortization

If the company uses both the van and the patent in its operations, its annual expense for depreciation and amortization will be:

Total Annual Expense = Depreciation + Amortization

Total Annual Expense = 5,000 + 1,500 = 6,500

This total reflects how the company allocates the cost of both tangible and intangible assets over their respective useful lives.

Why is Depreciation & Amortization Important?

Depreciation & Amortization help businesses spread out large expenses over several years, aligning the cost with the revenue generated by the asset. Depreciation and amortization are crucial for financial analysis and decision-making. Here’s why:

- Accurate Profit Measurement: They allow businesses to match costs with revenues, giving a clearer picture of profitability.

- Tax Benefits: These expenses reduce taxable income, lowering tax liabilities.

- Cash Flow Management: They are non-cash expenses, meaning they don’t impact cash flow directly, which helps companies allocate resources efficiently.

- Asset Value Tracking: Helps investors and managers understand how much value an asset retains over time.

What is a Good Depreciation & Amortization?

There’s no one-size-fits-all answer to what constitutes “good” depreciation and amortization. However, a reasonable level depends on:

- Industry Standards: Different industries have varying benchmarks for asset lifespans.

- Asset Usage: A higher depreciation rate may be suitable for heavily used assets.

- Financial Health: Sustainable depreciation rates should not overly strain a company’s profit margins.

For investors, consistent and reasonable depreciation practices often signal sound financial management.

Limitations of Depreciation & Amortization

Depreciation and amortization are essential tools for businesses and investors alike. They help in understanding asset values, managing taxes, and ensuring long-term profitability. While these accounting methods have their limitations, when used correctly, they provide valuable insights into a company’s financial health.

- Subjective Estimates: Useful life and salvage value are based on estimates, which may not always be accurate.

- Non-Cash Nature: These expenses do not directly reflect the current cash outflows of a business.

- Market Fluctuations: They don’t account for actual market conditions or replacement costs.

- Intangibles Challenges: Assigning a useful life to intangible assets like goodwill can be complex and imprecise.

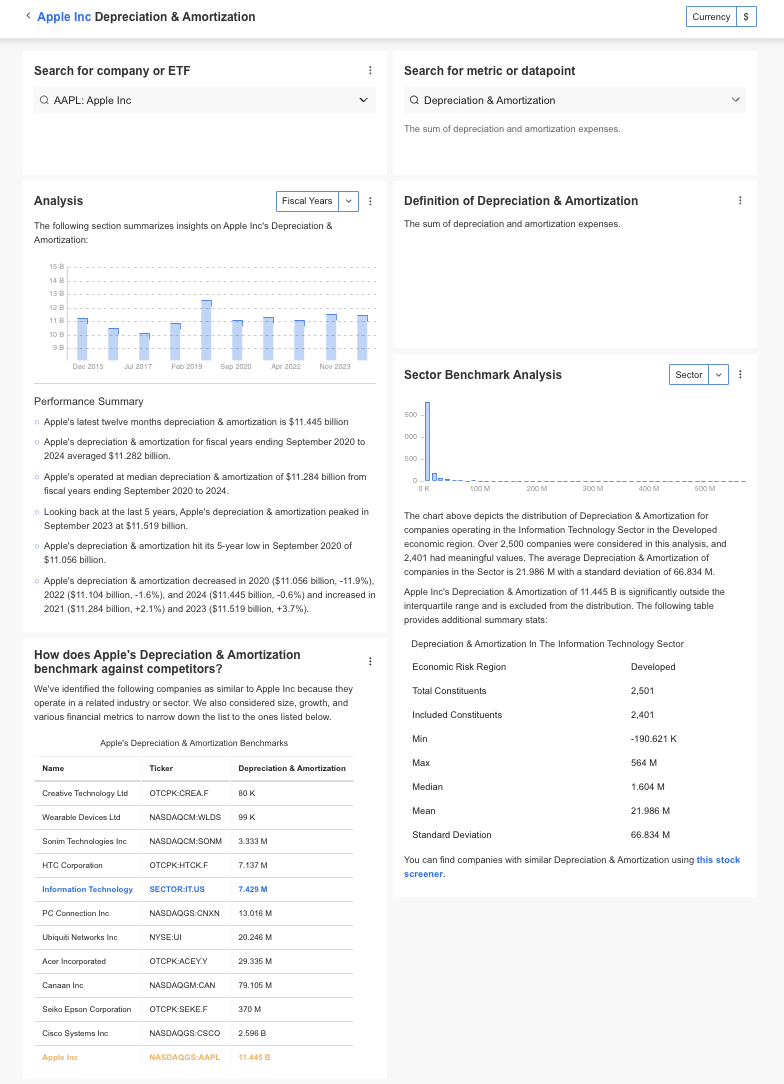

How to Find Depreciation & Amortization?

InvestingPro offers detailed insights into companies’ Depreciation & Amortization including sector benchmarks and competitor analysis.

InvestingPro: Access Depreciation & Amortization Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to Depreciation & Amortization data within the InvestingPro platform

🛠 Access to 1200+ additional fundamental metrics

🔍 Competitor comparison tools

📊 Evaluate stocks with 14+ proven financial models

Depreciation & Amortization FAQs

Can a business change its depreciation method?

Yes, businesses can change the depreciation method, but they must disclose this in their financial statements and justify the change.

Are land and goodwill depreciated?

Land is not depreciated as it doesn’t lose value over time. Goodwill, however, is subject to impairment testing instead of amortization.

How does depreciation impact cash flow?

Depreciation is a non-cash expense, so while it reduces taxable income, it doesn’t impact actual cash flow.

What is the difference between amortization and impairment?

Amortization spreads the cost of an intangible asset over its useful life, while impairment occurs when an asset’s market value falls below its book value.

Are depreciation and amortization tax-deductible?

Yes, they reduce taxable income, offering significant tax savings for businesses.