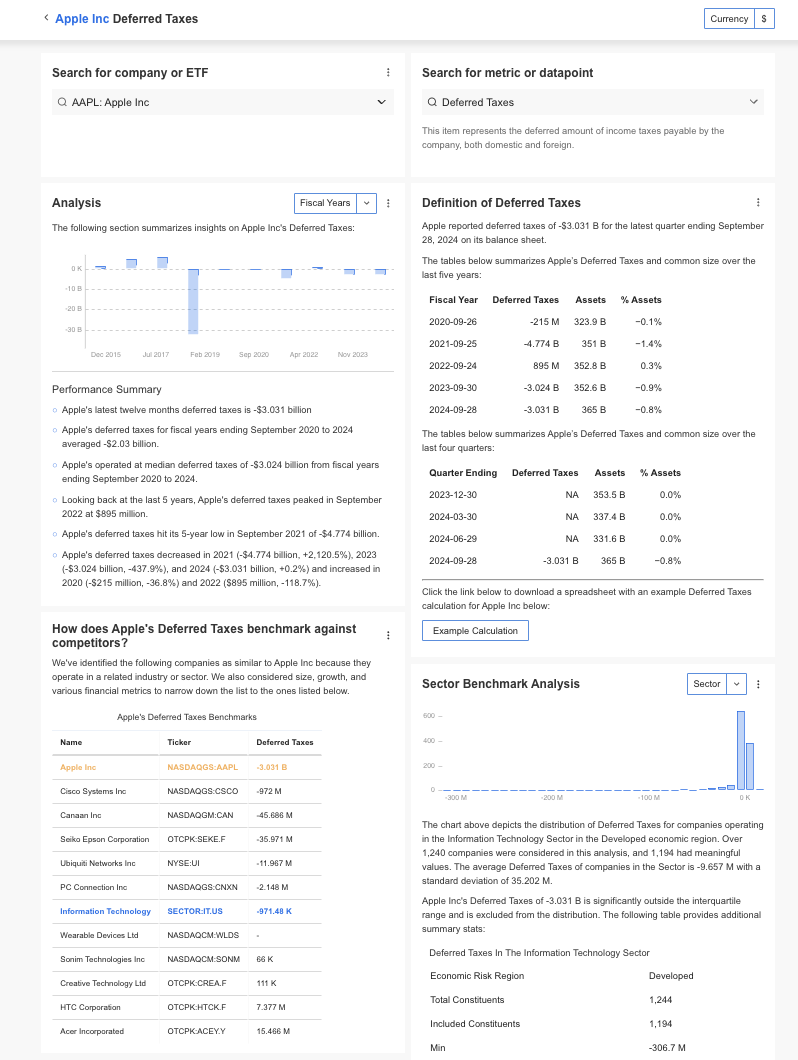

What are Deferred Taxes?

Deferred taxes refer to the taxes that a company will pay or receive in the future, due to temporary differences between its accounting profit and taxable income. These differences can arise because of varying accounting methods used for financial reporting purposes and tax calculations. Essentially, deferred taxes represent taxes owed or to be refunded in future periods, linked to the timing of income or expenses.

Types of Deferred Taxes?

There are two main types of deferred taxes:

- Deferred Tax Liabilities (DTL): These arise when a company’s taxable income is lower than its accounting income, meaning taxes will be owed in the future.

- Deferred Tax Assets (DTA): These arise when a company’s taxable income is higher than its accounting income, leading to future tax refunds.

For example, a business might report higher depreciation expenses in its financial statements due to accounting rules, but the tax authorities might allow depreciation on a different schedule. This creates a temporary difference, which results in deferred taxes.

Deferred taxes are important for understanding a company’s future tax obligations or refunds and can significantly impact financial analysis and investment decisions.

How to Calculate Deferred Taxes?

The formula for calculating deferred taxes is:

Deferred Tax = Temporary Difference × Tax Rate

Deferred Tax Liability is calculated when the taxable amount in the future will exceed the book value. Deferred Tax Asset is calculated when the taxable amount in the future will be less than the book value.

Calculating deferred taxes involves understanding the temporary differences between the book value (financial statements) and the tax base (tax filings) of a company’s assets and liabilities. To calculate deferred tax liabilities or assets, you need the following:

- Temporary Difference: This is the difference between the carrying amount of an asset or liability in the financial statements and its tax base.

- Tax Rate: The tax rate that will apply to the temporary difference when it reverses in the future.

Example Calculation of Deferred Taxes

Let’s consider a simplified example to understand how deferred taxes work.

Suppose a company purchases a piece of equipment for $10,000 and depreciates it using the straight-line method for accounting purposes over 5 years. This means the company reports $2,000 in depreciation annually for its financial statements.

However, for tax purposes, the company uses an accelerated depreciation method that allows it to depreciate $4,000 in the first year.

At the end of the first year, there is a temporary difference of $2,000 ($4,000 tax depreciation – $2,000 book depreciation). If the tax rate is 25%, the deferred tax liability would be:

Deferred Tax Liability = 2,000 × 0.25 = 500

In this case, the company will owe $500 in deferred taxes in the future when the tax depreciation catches up with the book depreciation.

On the other hand, if the company had reported a greater depreciation for its books than for tax purposes, a deferred tax asset would be created.

Why are Deferred Taxes Important?

Deferred taxes are an essential aspect of financial accounting for several reasons:

- Understanding Future Tax Obligations: Deferred taxes help businesses and investors understand future tax liabilities or assets, which can significantly impact cash flow and financial planning.

- Accurate Financial Reporting: They ensure that a company’s financial statements accurately reflect its future tax obligations. Without accounting for deferred taxes, a company’s profit may be overstated, leading to misleading financial reports.

- Impact on Cash Flow: While deferred tax liabilities represent future cash outflows, deferred tax assets can provide future cash inflows. These amounts may influence decisions about capital allocation, investment, or debt management.

- Strategic Tax Planning: By understanding deferred tax positions, companies can engage in strategic tax planning, such as taking advantage of tax credits, incentives, or deferring tax payments to optimize their overall tax strategy.

- Investment Decisions: For investors, deferred taxes offer insights into a company’s tax position, helping them assess its future profitability and financial health.

What is a Good Deferred Tax Position?

A “good” deferred tax position depends on whether a company has more deferred tax assets or liabilities, and how these relate to the company’s overall tax strategy. Here are a few points to consider:

- Deferred Tax Liabilities: A company may have significant deferred tax liabilities, indicating that it expects to pay higher taxes in the future. While this is not inherently negative, it could signal potential cash outflows that need to be managed effectively.

- Deferred Tax Assets: A company with deferred tax assets might be in a position to benefit from tax refunds or reduced tax payments in the future. This can be a positive indicator for companies that are facing current tax burdens but expect to benefit later.

- Balance and Planning: A good deferred tax position reflects a balance between assets and liabilities, with a focus on managing these amounts over time. Companies should aim to manage deferred tax positions to optimize their cash flow and tax strategy.

- Realization of Assets: A good deferred tax position also involves the ability to realize deferred tax assets. This requires that the company be able to generate enough taxable income to offset the deferred tax assets in the future.

What are the Limitations of Deferred Taxes?

While deferred taxes are crucial for accurate financial reporting, there are limitations:

- Estimations: Calculating deferred taxes relies on estimates of future tax rates, timing of temporary differences, and potential changes in tax laws. This introduces a level of uncertainty in the forecasts.

- Complexity: The calculation and management of deferred taxes can be complex, especially for large businesses with many assets and liabilities. Companies must stay updated on tax law changes and adjust their calculations accordingly.

- Non-Cash Impact: Deferred taxes are non-cash transactions. This means that while they appear on the income statement and balance sheet, they do not directly affect the company’s cash flow in the period in which they are recorded.

- Not Always Realizable: Deferred tax assets are only realized when it is probable that the company will have sufficient taxable income in the future. If a company is not profitable in the future, it may not be able to realize these assets.

How to Find Deferred Taxes?

InvestingPro offers detailed insights into companies’ Deferred Taxes including sector benchmarks and competitor analysis.

InvestingPro: Access Deferred Taxes Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to Deferred Taxes data within the InvestingPro platform

🛠 Access to 1200+ additional fundamental metrics

🔍 Competitor comparison tools

📊 Evaluate stocks with 14+ proven financial models

Deferred Taxes FAQ

How are deferred taxes reported in financial statements?

Deferred taxes are reported on the balance sheet. Deferred tax liabilities appear under non-current liabilities, while deferred tax assets are typically listed under non-current assets.

Are deferred taxes the same as tax liabilities?

No, deferred taxes are different from tax liabilities. Tax liabilities represent taxes that are currently owed, while deferred taxes represent taxes that are owed or to be refunded in the future due to temporary differences in accounting methods.

Can deferred tax assets be used to offset future tax liabilities?

Yes, deferred tax assets can be used to offset future tax liabilities when the company has sufficient taxable income. However, the realization of these assets is not guaranteed.

Why do companies use accelerated depreciation for tax purposes?

Companies often use accelerated depreciation for tax purposes to reduce their taxable income in the short term, which lowers their current tax payments. However, this creates a temporary difference that results in deferred tax liabilities.

How do deferred taxes affect cash flow?

Deferred taxes do not directly affect cash flow in the period they are recorded. However, they represent future cash inflows (for tax assets) or outflows (for tax liabilities), impacting the company’s future financial position.