What Are Capital Leases?

Capital leases, also known as finance leases, are agreements where a lessee obtains rights to use an asset over a set period. These leases are structured such that the lessee assumes many of the benefits and risks of ownership. Recognized as long-term liabilities, capital leases reflect the lessee’s obligation to pay for the asset over time.

Criteria for Capital Leases

To determine if a lease qualifies as a capital lease, it must meet at least one of the following conditions:

- Ownership Transfer: Ownership of the asset is transferred to the lessee at the lease’s end.

- Bargain Purchase Option: The lessee can purchase the asset at a price substantially below its expected market value.

- Lease Duration: The lease term spans at least 75% of the asset’s estimated economic life.

- Present Value Threshold: The present value of lease payments amounts to 90% or more of the asset’s fair market value.

Understanding Capital Leases

Unlike operating leases, which are treated as regular rental agreements under Generally Accepted Accounting Principles (GAAP), capital leases are recorded as asset purchases if certain criteria are met. This classification can significantly impact a company’s financial statements by influencing reported expenses, depreciation, and liabilities.

The terminology shift from “capital lease” to “finance lease” reflects changes in accounting standards, specifically with the adoption of IFRS 16 and ASC 842. Despite the change in nomenclature, the economic substance and legal structure of these leases remain consistent.

These leases are crucial for businesses aiming to optimize asset usage without immediate capital expenditure, offering tax benefits as lease payments may be deductible as business expenses. Capital and finance leases play a vital role in corporate finance, providing a pathway for companies to grow and operate efficiently without the heavy burden of initial asset purchase costs.

Difference Between Capital Lease & Operating Lease

Operating leases and capital leases present distinct structures and accounting treatments. Traditionally, an operating lease allowed a company to utilize an asset without ownership rights, keeping these leases off the balance sheet. This approach provided a strategic advantage by not reflecting the asset or future rent liabilities on the balance sheet, thus keeping the debt-to-equity ratio more favorable.

However, with the enactment of Accounting Standards Update 2016-02 (ASU 842), starting on December 15, 2018, for public entities and December 15, 2019, for private entities, this changed significantly. Now, both right-of-use assets and corresponding liabilities must be reported on the balance sheet.

Under generally accepted accounting principles (GAAP), a lease must pass specific criteria to be classified as an operating lease, known as the “bright line” tests. If the lease fails to meet these requirements, it is considered a capital lease. The Internal Revenue Service (IRS) has the authority to reclassify an operating lease as a capital lease, which can lead to increased taxable income and tax obligations due to the disallowance of certain lease payment deductions.

Capital vs. Operating Leases: Accounting Implications and Tax Considerations

The core distinction between capital and operating leases hinges on the ownership characteristics and their impact on financial statements.

In a capital lease, the lessee is essentially the asset owner, which necessitates recording the leased asset and liability on the balance sheet. On the contrary, operating leases lack ownership characteristics, with the leased assets not appearing on the balance sheet. Instead, rental expenses are recognized in the income statement as incurred, and payments are documented in the cash flow statement.

The notable distinction is that in operating leases, the asset must be returned to the lessor at the lease term’s end. Initially, operating leases are listed as liabilities on the balance sheet, akin to debt. The accounting treatment diverges on the income statement, where the lease expense is recorded throughout the lease term. The cash flow statement reflects these payments within the cash flow from operations section.

Operating leases, being shorter-term, retain asset ownership with the lessor. They are fully tax-deductible as operating expenses, offering immediate financial benefits. In contrast, capital leases, treated similarly to ownership, span longer durations, with only the interest component of payments being tax-deductible.

Accounting Treatment for Capital Leases

Under accounting standards, capital leases are treated similarly to asset purchases. On the balance sheet, they are recorded as both an asset and a liability. Over time, the asset is depreciated, and the liability is reduced as lease payments are made. This treatment ensures a more accurate reflection of a company’s financial health by acknowledging both the asset and the debt associated with it.

In accounting terms, capital leases require the lessee to record both the asset and the lease obligation on their balance sheet. This recognition impacts financial ratios and indicators, offering a more comprehensive view of a company’s financial health. The asset is depreciated over time, while the lease obligation is amortized, influencing both income statements and balance sheets.

Advantages of Capital Leases

Capital leases are particularly beneficial for businesses looking to conserve cash while acquiring essential assets such as offices, equipment, and vehicles. These leases allow companies to use assets without a substantial upfront purchase, making them an economically viable alternative to outright buying.

Leasing offers strategic financial benefits, enabling companies to use essential assets without a substantial initial cash outlay. This approach is especially useful for businesses that need specific equipment or property to operate but lack the liquidity for outright purchases. Regular lease payments help maintain a predictable expense structure, while the option to buy the asset at a nominal price at the end of the lease term provides additional flexibility.

The financial commitments under a capital lease are spread out over the lease term, providing a more predictable and stable cost structure. Additionally, at the end of the lease, the lessee often has the option to purchase the asset for a predetermined price, enabling businesses to eventually own the assets at a nominal cost.

- Reduced Initial Investment: Capital leases provide the advantage of a lower initial outlay compared to buying the asset outright.

- End-of-Term Ownership: The lessee gains ownership of the asset after fulfilling the lease term.

- Consistent Lease Payments: Fixed lease payments offer predictability, making it easier to manage and forecast budgets.

- Possible Tax Incentives: Lease payments may be eligible for deduction as a business expense, offering potential tax advantages.

Limitations of Capital Leases

Engaging in a capital lease can often entail greater expenses over time than outright buying the asset. This kind of lease typically involves a long-term commitment, potentially locking in higher costs than those associated with shorter rentals or direct purchases.

Maintenance and repair responsibilities also fall on the lessee, which can lead to substantial additional costs. The inflexible nature of capital leases makes early termination or modifications difficult, which may not suit all business needs. Another notable downside is the risk of the asset becoming obsolete before the lease concludes.

On the financial statement side, capital leases can heighten a company’s liabilities, potentially limiting its future borrowing capacity.

How to Find Capital Leases?

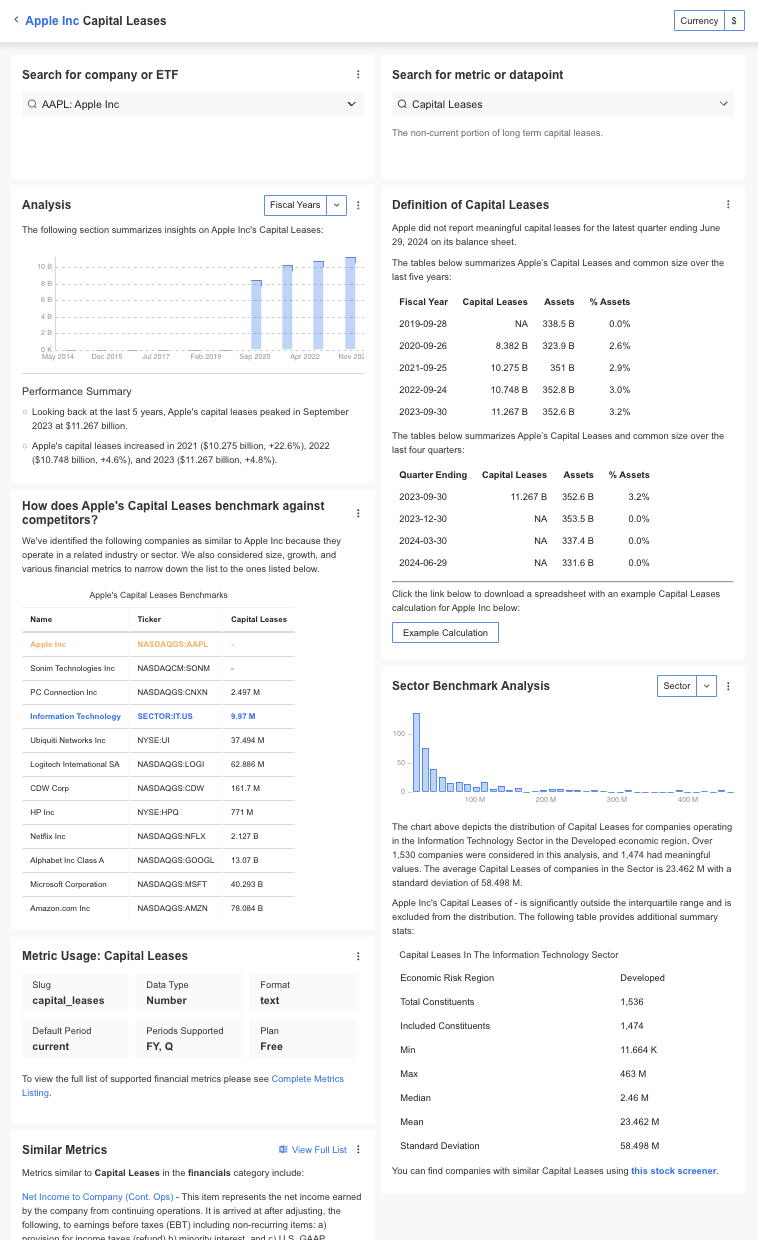

InvestingPro offers detailed insights into companies’ Capital Leases including sector benchmarks and competitor analysis.

InvestingPro: Access Capital Leases Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to Capital Leases data within the InvestingPro platform

✓ Access to 1200+ additional fundamental metrics

✓ Competitor comparison tools

✓ Evaluate stocks with 14+ proven financial models

Capital Leases FAQ

What is a capital lease?

A capital lease is a long-term agreement where the lessee acquires the use of an asset and assumes ownership-like responsibilities.

What assets can be included in a capital lease?

Assets such as machinery, vehicles, and real estate are often obtained through capital lease agreements.

How does a capital lease affect financial statements?

It increases both assets and liabilities on the balance sheet, providing a clearer picture of a company’s financial commitments.

Why opt for a capital lease over buying an asset outright?

Capital leases allow companies to leverage assets without the upfront cost, offering potential tax benefits and improved cash flow management without a large upfront investment.

Are lease payments under a capital lease deductible?

Yes, lease payments are generally deductible as business expenses, offering potential tax advantages.