What Is Amortization of Intangible Assets?

Amortization of intangible assets refers to the systematic allocation of the cost of intangible assets – non-physical assets such as patents, trademarks, copyrights, or licenses – over their useful economic lives. Unlike tangible assets, which depreciate, intangible assets are amortized unless they have an indefinite life, such as goodwill. This distinction is crucial for maintaining accurate financial records and complying with accounting standards.

How to Calculate Amortization of Intangible Assets?

The amortization of intangible assets typically uses the straight-line method unless another method more accurately reflects the pattern of economic benefits derived.

The formula for Straight-Line Amortization is:

Annual Amortization Expense = (Cost of Asset − Residual Value) / Useful Life

Breaking down the formula:

- Cost of Asset: The purchase price or development cost of the intangible asset.

- Residual Value: The estimated value of the asset at the end of its useful life, often set to zero for intangible assets.

- Useful Life: The duration for which the asset is expected to provide economic benefits.

Example Calculation of Amortization of Intangible Assets

Suppose a company acquires a patent for $500,000 with a useful life of 10 years and no residual value.

Calculation:

Annual Amortization Expense = (500,000 − 0) / 10 = 50,000

Each year, the company will recognize $50,000 as an amortization expense in its income statement, reducing the patent’s book value over time.

Why is Amortization of Intangible Assets Important?

The process of Intangible Asset Amortization allows businesses to account for the gradual reduction in the value of these assets in their financial statements while aligning costs with the revenue generated by their use.

Expense Matching

Aligns the cost of intangible assets with the revenue they generate, ensuring financial accuracy.

Tax Benefits

Amortization reduces taxable income, providing a tax shield for businesses.

Investor Insights

Provides stakeholders with a clear understanding of how the company utilizes and derives value from its intangible assets.

Key Characteristics of Intangible Asset Amortization

Intangible Nature: Intangible assets lack physical form but have significant value due to their role in generating economic benefits. Examples include intellectual property, software licenses, and franchise agreements.

Finite Useful Life: Only assets with a finite useful life are subject to amortization. Assets with indefinite useful lives, such as goodwill, are not amortized but are periodically tested for impairment.

Accounting Standards Compliance: The process of amortizing intangible assets is governed by accounting frameworks such as Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS).

Common Intangible Assets Subject to Amortization

Patents: Legal protections for inventions. Amortized over their legal life or the period of economic benefit, whichever is shorter.

Copyrights: Exclusive rights for creative works. Typically amortized over their legal protection period, up to 70 years post-author’s death.

Software Licenses: Rights to use proprietary software. Amortized over the license term or expected usage period.

Franchise Agreements: Contracts granting rights to operate under a franchisor’s brand. Amortized over the agreement’s duration.

Accounting for Intangible Asset Amortization

Amortization impacts two primary financial statements:

Income Statement

- The amortization expense is recorded as an operating expense, reducing net income.

- For example, a $50,000 amortization expense for a patent lowers taxable income by the same amount.

Balance Sheet

- The intangible asset’s book value is reduced annually by the amortization expense.

- Using the earlier example, the patent’s value would decrease from $500,000 to $450,000 after the first year.

Challenges and Considerations

- Estimating Useful Life: Determining the accurate economic life of intangible assets can be subjective and vary across industries.

- Impairment Risk: Assets not subject to amortization, such as goodwill, may require impairment write-offs if their carrying value exceeds recoverable amounts.

- Regulatory Changes: Changes in tax or accounting standards can influence how companies report and amortize intangible assets.

By systematically amortizing intangible assets, companies can maintain transparency and accuracy in their financial reporting, ensuring a true reflection of their economic performance.

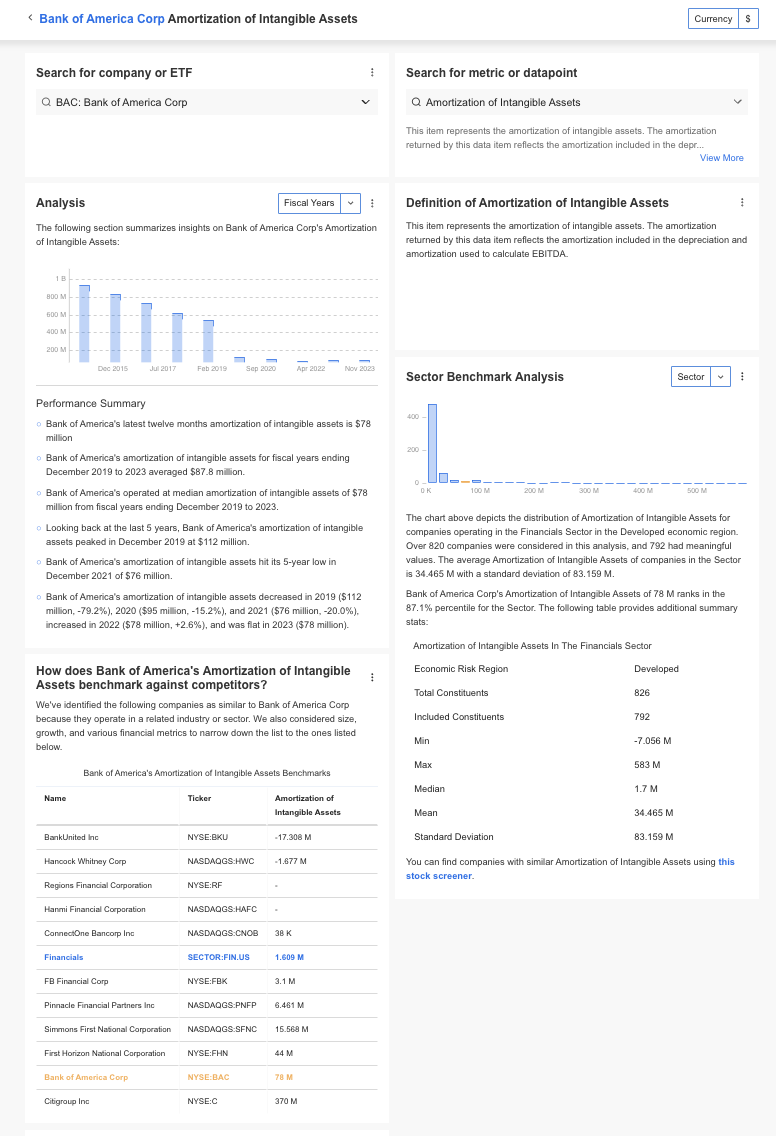

How to Find Amortization of Intangible Assets?

InvestingPro offers detailed insights into companies’ Amortization of Intangible Assets including sector benchmarks and competitor analysis.

InvestingPro+: Access Amortization of Intangible Assets Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to Amortization of Intangible Assets data within the InvestingPro platform

🛠 Access to 1200+ additional fundamental metrics

🔍 Competitor comparison tools

📊 Evaluate stocks with 14+ proven financial models

Amortization of Intangible Assets FAQs

What intangible assets are not amortized?

Assets with indefinite useful lives, such as goodwill and some trademarks, are not amortized but must undergo impairment testing annually.

How does amortization differ under GAAP and IFRS?

Both frameworks use the straight-line method but may differ in assessing useful life and impairment testing. GAAP allows some tax-related exceptions, while IFRS focuses on fair value adjustments.

Can intangible assets have a residual value?

Typically, intangible assets have no residual value at the end of their useful life, as they are often fully utilized or lose value due to obsolescence.

How does amortization affect cash flow?

Amortization is a non-cash expense, meaning it does not directly impact cash flow. However, it reduces taxable income, potentially lowering cash outflows for taxes.

What happens if an intangible asset becomes obsolete early?

If an intangible asset loses its value prematurely, it may require impairment recognition, which reduces its book value to reflect the current market condition.