Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

After registering positive earnings surprises in the past three quarters, Target Corporation (NYSE:TGT) missed on earnings in the final quarter of fiscal 2017. The company posted fourth-quarter adjusted earnings of $1.37 per share that missed the Zacks Consensus Estimate by a couple of cents and declined 5.8% from the prior-year period. The quarterly earnings came above the mid-point of the recent provided guidance range of $1.30-$1.40 per share.

We observe that rise in cost of sales and higher SG&A expenses hurt the bottom line. Even higher sales failed to act as a savior. Shares of this Minneapolis-based company are down roughly 4% during pre-market trading hours. This is because of the continued year-over-year decline in the bottom line.

Nevertheless, the company generated total sales of $22,766 million that surpassed the Zacks Consensus Estimate of $22,463 million for the fourth straight quarter, and surged 10% from the year-ago quarter.

Target’s initiatives such as the development of omni-channel capacities, diversification and localization of assortments along with emphasis on flexible format stores are encouraging. Additionally, the company intends to deploy resources to significantly develop online platform as well as store facilities to make shopping more convenient for customers. Moreover, “Target Restock” program is also gaining traction.

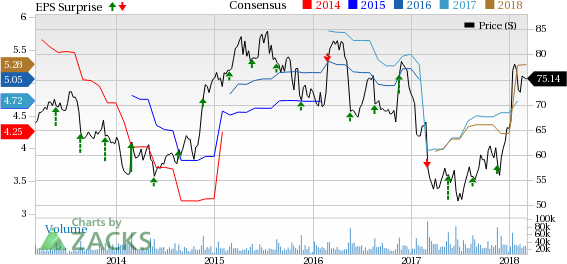

Target Corporation Price, Consensus and EPS Surprise

Target Corporation Price, Consensus and EPS Surprise | Target Corporation Quote

Notably, comparable sales for the quarter increased 3.6% against 1.5% decline witnessed in the year-ago period. The number of transactions jumped 3.2%, while the average transaction amount increased 0.4%. Comparable digital channel sales surged 29% and added 1.8 percentage points to comparable sales.

These helped this Zacks Rank #2 (Buy) stock to gain 23% in the past three months compared with the industry’s growth of 6.2%.

Gross profit grew 8.5% to $5,971 million, while gross margin contracted 40 basis points to 26.2%. Operating income plummeted 14.6% to $1,152 million, while operating margin shriveled 140 basis points to 5.1%.

Target’s debit card penetration remained flat at 12.7%, while credit card penetration fell 20 basis points to 11.4%. Total REDcard penetration declined to 24% from 24.3% in the year-ago quarter.

Other Financial Details

During the quarter, Target repurchased shares worth $254 million and paid dividends of $337 million. The company still had about $3.7 billion remaining under its $5 billion share buyback program. The company ended the quarter with cash and cash equivalents of $2,643 million, long-term debt and other borrowings of $11,317 million and shareholders’ investment of $11,709 million.

A Glance at the Outlook

Management now anticipates first quarter and fiscal 2018 comparable sales to be up low-single digit. Target now envisions first quarter earnings in the band of $1.25-$1.45 and fiscal 2018 earnings between $5.15 and $5.45 per share. The current Zacks Consensus Estimate for the first quarter and fiscal 2018 stands at $1.40 and $5.28, respectively.

Interested in Retail Space? Check These 3 Trending Stocks

American Eagle Outfitters (NYSE:AEO) delivered an average positive earnings surprise of 2.6% in the trailing four quarters. The company has a long-term earnings growth rate of 5.5% and a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

G-III Apparel (NASDAQ:GIII) delivered an average positive earnings surprise of 6.1% in the trailing four quarters. It has a long-term earnings growth rate of 15% and a Zacks Rank #2.

The Children's Place, Inc. (NASDAQ:PLCE) delivered an average positive earnings surprise of 14% in the trailing four quarters. It has a long-term earnings growth rate of 9% and a Zacks Rank #2.

Wall Street’s Next Amazon (NASDAQ:AMZN)

Zacks EVP Kevin Matras believes this familiar stock has only just begun its climb to become one of the greatest investments of all time. It’s a once-in-a-generation opportunity to invest in pure genius.

Click for details >>

Warren Buffett and Berkshire Hathaway (NYSE:BRKa) always make headlines in February when the firm holds its annual meeting. Among the many takeaways is what the company has been...

While Tuesday I wrote about the strength of junk bonds in the face of risk-off ratios (TLT v. SPY, HYG), today, I am still quite concerned about Granny Retail or the consumer...

Shares of Caesars Entertainment (NASDAQ:CZR), a leading gambling stock, traded around 3% higher on Wednesday morning, though the stock was trading around 1.5% lower shortly before...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.