Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

John Wiley & Sons, Inc. JW.A posted better-than-expected results in the third quarter of fiscal 2018, wherein both the top and bottom line surpassed the Zacks Consensus Estimate. While earnings delivered a sixth consecutive quarter of positive surprise, sales marked its fourth straight beat.

Despite the earnings and sales beat, not much movement was witnessed in the stock yesterday. However, this Zacks Rank #3 (Hold) stock has rallied 25% in the past six months, outperforming the industry’s gain of 19.7%.

Q3 in Detail

John Wiley & Sons reported adjusted earnings of 87 cents per share, outpacing the Zacks Consensus Estimate of 84 cents. However, the bottom line decreased 2.2% from 89 cents in the year-ago quarter. Also, on a constant currency (cc) basis, adjusted earnings were down 14% year over year.

On a GAAP basis, the company recorded earnings of $1.19, which surged 45% from the prior-year quarter, mainly driven by US tax reforms.

Further, revenue of $455.7 million improved about 4% year over year (down 1% on a cc basis) and outpaced the Zacks Consensus Estimate of nearly $446 million. The year-over-year increase can be attributable to sales growth at the Research and Solutions segments, partly offset by decline at the Publishing division.

Adjusted operating income came in at $69.6 million compared with $60.3 million in the year-ago quarter. The upside was primarily driven by technology-savings as well as prior restructuring activities. The metric also grew 2% on a cc basis. The adjusted operating margin jumped 150 basis points to 15.3%. However, cost of sales increased 7.5%, and operating and administrative expenses inched up 0.6%.

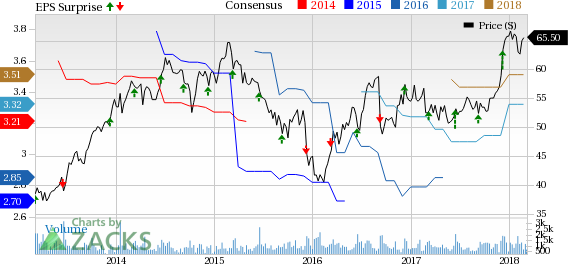

John Wiley & Sons, Inc. Price, Consensus and EPS Surprise

John Wiley & Sons, Inc. Price, Consensus and EPS Surprise | John Wiley & Sons, Inc. Quote

Segmental Details

Research: Sales at this division came in at $223.5 million and increased 9% year over year, fueled by solid contributions from Open Access. On a cc basis, top line at this segment was up 1%. Furthermore, rise in Licensing, Reprints, Backfile and Other revenues as well as Publishing Technology Services (Atypon) contributed to sales growth. The segment’s adjusted contribution to profit was $60 million compared with $53 million recorded in the prior-year quarter. On a cc basis, the same declined 2%.

Publishing: At this division, the top line dipped nearly 1% to $170.2 million (down 3% on cc basis) on account of soft performance of Course Workflow (WileyPLUS); Test Preparation and Certification; Licensing, Distribution, Advertising and Other as well as Educational Publishing. The decline was somewhat offset by sales growth at STM and Professional Publishing. While adjusted contribution to profit surged 21% to $48.1 million, the same rose 16% on a cc basis.

Solutions: Top line at this segment increased 5% year over year to $61.9 million (up 2% on a cc basis), backed by robust performance of Education Services/Online Program Management and Corporate Learning, partly offset by a decline in Professional Assessment revenues. The division’s adjusted contribution to overall profit was $7.7 million, up from $4.7 million in the year-ago period. Also, on a cc basis, the same surged 67%.

Other Financial Update

John Wiley & Sons ended the quarter with cash and cash equivalents of $128.2 million, long-term debt of $428.2 million and shareholders’ equity of $1,168.3 million.

Notably, the company provided $190.1 million of cash by operating activities in the first nine months of fiscal 2018. Further, the company reported free cash flow (net of Product Development Spending) of $80.7 million at the end of the quarter compared with $119.5 million in the year-ago period.

Management projects cash provided by operations to be up $35 million or more for the fourth quarter and roughly $350 million for fiscal 2018.

Furthermore, the company did not buy back shares in the reported quarter. However, on a year-to-date basis, it bought back 551,000 shares for $29.3 million and paid dividends of $55.1 million.

Guidance

Management reaffirmed its guidance for fiscal 2018. Both revenues and adjusted operating income (at cc) are anticipated to be nearly flat year over year. Adjusted earnings (at cc) are expected to be down by low-single digits. The Zacks Consensus Estimate for fiscal 2018 is pegged at $3.35.

Meanwhile, cash from operations is anticipated to be at least $350 million (at cc) compared with $314.5 million in fiscal 2017. Further, capital expenditures (on a cc basis) are expected to be slightly lower than $148.3 million incurred last year.

Don’t Miss These Three Trending Picks

AMC Networks Inc. (NASDAQ:AMCX) has a long-term earnings growth rate of 8.4% and a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Entercom Communications (NYSE:ETM) has a long-term earnings growth rate of 2% and a Zacks Rank #2 (Buy).

TEGNA Inc. (NYSE:TGNA) , also a Zacks #2 Ranked player, has delivered an average positive earnings surprise of 3.8% in the last four quarters.

Breaking News: Cryptocurrencies Now Bigger than Visa

The total market cap of all cryptos recently surpassed $700 billion – more than a 3,800% increase in the previous 12 months. They’re now bigger than Morgan Stanley (NYSE:MS), Goldman Sachs (NYSE:GS) and even Visa! The new asset class may expand even more rapidly in 2018 as new investors continue pouring in and Wall Street becomes increasingly involved.

Zacks’ has just named 4 companies that enable investors to take advantage of the explosive growth of cryptocurrencies via the stock market.

Click here to access these stocks. >>

Shares of Alibaba (NYSE:BABA) are on a tear to start off 2025. The consumer discretionary and tech stock is up by 52% this year as of the Feb. 25 close. The company’s cloud...

Every investor should know the term CEP, or customer engagement platform, because it is central to businesses' use of AI. CEPs provide software services to connect and communicate...

As markets try to look through the blizzard of policy changes flowing out of Washington, the crowd has shifted its preferences considerably in recent weeks based on a sector lens....

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.