Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

Similar to wise buying decisions, exiting certain underperformers at the right time helps maximize portfolio returns. Selling off losers can be difficult, but if both the share price and estimates are falling, it could be time to get rid of the security before more losses hit your portfolio.

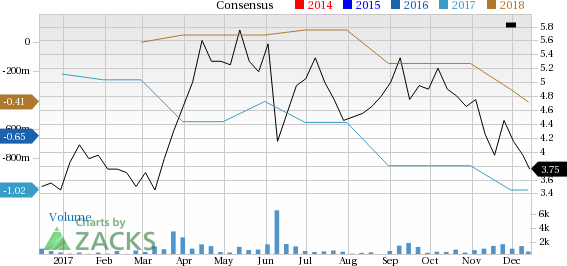

One such stock that you may want to consider dropping is Cogint, Inc. (NASDAQ:COGT) , which has witnessed a significant price decline in the past four weeks, and it has seen negative earnings estimate revisions for the current quarter and the current year. A Zacks Rank #4 (Sell) further confirms weakness in COGT.

A key reason for this move has been the negative trend in earnings estimate revisions. For the full year, we have seen one estimate moving down in the past 30 days, compared with just no upward revisions. This trend has caused the consensus estimate to trend lower, going from a loss of 96 cents a share a month ago to its current level of a loss of $1.02.

Also, for the current quarter, Cogint has seen one downward estimate revision versus no revisions in the opposite direction, dragging the consensus estimate down to a loss of 16 cents a share from a loss of 10 cents over the past 30 days.

The stock also has seen some pretty dismal trading lately, as the share price has dropped 9.3% in the past month.

Cogint Price and Consensus

So it may not be a good decision to keep this stock in your portfolio anymore, at least if you don’t have a long time horizon to wait.

If you are still interested in the Computers - IT Services industry, you may instead consider a better-ranked stock – Fair Isaac Corporation (NYSE:FICO) . The stock currently holds a Zacks Rank #1 (Strong Buy) and may be a better selection at this time. You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks Editor-in-Chief Goes "All In" on This Stock

Full disclosure, Kevin Matras now has more of his own money in one particular stock than in any other. He believes in its short-term profit potential and also in its prospects to more than double by 2019. Today he reveals and explains his surprising move in a new Special Report.

Download it free >>

Nvidia’s earnings beat didn’t erase investor concerns over slowing growth. Soft Q1 guidance and valuation worries may limit the stock’s upside. Weak network and gaming sales...

Warren Buffett and Berkshire Hathaway (NYSE:BRKa) always make headlines in February when the firm holds its annual meeting. Among the many takeaways is what the company has been...

While Tuesday I wrote about the strength of junk bonds in the face of risk-off ratios (TLT v. SPY, HYG), today, I am still quite concerned about Granny Retail or the consumer...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.