Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

Abercrombie & Fitch Co. (NYSE:ANF) is slated to release fourth-quarter fiscal 2017 results on Mar 7. The question lingering in investors’ minds is, whether this specialty retailer of premium, high-quality casual apparel will be able to deliver a positive earnings surprise in the to-be-reported quarter.

The company’s bottom line has surpassed the Zacks Consensus Estimate in the last two quarters, with an average beat of 17.8% in the trailing four. Let’s see how things are shaping up prior to this announcement.

What to Expect

The Zacks Consensus Estimate for the quarter under review is pegged at $1.13 per share, reflecting year-over-year growth of 59.2%. Further, the estimate has been moving up in the past 30 days. Further, analysts polled by Zacks expect revenues of $1.17 billion, up 12.8% from fourth-quarter fiscal 2016.

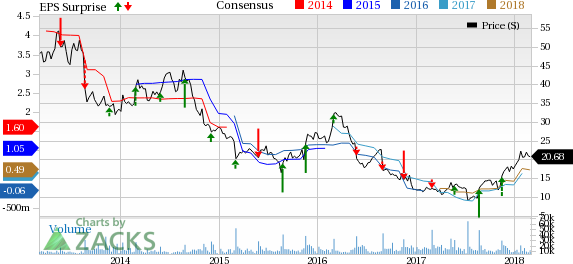

Abercrombie & Fitch Company Price, Consensus and EPS Surprise

Abercrombie & Fitch Company Price, Consensus and EPS Surprise | Abercrombie & Fitch Company Quote

Moreover, Abercrombie’s shares have rallied 17.2% in the past three months, outperforming the industry’s gain of 2.5%. The recent surge in share price is attributed to the company’s robust holiday sales and the resulting favorable outlook for the fourth quarter.

Shares of Caesars Entertainment (NASDAQ:CZR), a leading gambling stock, traded around 3% higher on Wednesday morning, though the stock was trading around 1.5% lower shortly before...

Amazon (NASDAQ:AMZN) is making a significant push into the future with a robust investment in robotics and artificial intelligence. The company has earmarked $35 billion for...

Home Depot’s (NYSE:HD) Q4 2024 report and guidance for 2025 have plenty to be unhappy about, but the simple truth is that this company turned a corner in 2024. It is on track for...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.